In Ethiopia, women account for a disproportionate share of the unbanked, and the gap is widening. Photo: Binyam Teshome/World Bank

The World Bank Group (WBG), with private and public sector partners, set an ambitious target to achieve

Universal Financial Access (UFA) by 2020. The UFA goal envisions that, by 2020, adults globally will be able to have access to a transaction account or electronic instrument to store money, send and receive payments. The WBG has committed to enabling one billion people to gain access to a transaction account through targeted interventions. Ethiopia is one of the 25 priority countries for UFA initiative.

So where does Ethiopia stand in terms of financial inclusion? The

Global Findex database tracks how adults save, borrow, make payments, and manage risk. Here are 10 takeaways for Ethiopia from the newly released Global Findex.

Double digit growth in account ownership

In 2017, the percentage of adults with an account rose to 35%, up from 22% in 2014. Account usage has improved as well. Now 26% of adults save at financial institutions (as compared to 14% in 2014) and 11% borrow from financial institutions (as compared to 7% in 2014).

… but still Ethiopia lags behind other Sub-Saharan African countries

Despite this increase in account ownership, Ethiopia lags behind its neighboring countries. In Kenya, for example, 82% of adults have an account, while in Rwanda, account ownership stands at 50%. And in the region overall, 43% of adults have an account.

People rely more on informal institutions for their financial needs

Although 62% of Ethiopians reported saving money in the past year, only 26% saved formally at financial institutions, while 38% saved with a person outside of a family or

at an informal saving club (for example, Iqub is a rotating saving and credit association where each member agrees to regularly pay a small sum into a common pool so that each, in rotation, can receive one large sum). During the same period, 41% of Ethiopians said they borrowed money, but only 11% borrowed from financial institutions. The rest borrowed from family or friends (31 percent) and 8% borrowed from a saving club (8%).

The gender gap is widening

Women account for a disproportionate share of the unbanked, and the gap is widening. In 2017, the gender gap jumped to 12% from being virtually insignificant in 2014!

Now, 41% of men have an account, compared to 29% of women, whereas in 2014 account ownership was essentially even, with 23% of men and 21% of women with an account.

Account ownership among men has nearly doubled in three years, but for women it has increased by only eight percentage points.

Wealthier adults are twice as likely as poorer ones to have an account

Among adults in the richest 60% of households within Ethiopia, 43% have an account as compared to 22% account ownership among the poorest 40% of adults.

In general, women, rural, less educated, unemployed, and poorer adults are less likely to own an account.

Key Barriers for financial inclusion

Of the total unbanked surveyed adults, 85% reported insufficient funds as a reason for not opening an account. This seems to signal a perception among adults that ‘financial services are not meant for the poor.’ Distance (cited by 20% adults) and lack of documentation (cited by 11% of adults) were mentioned as the second and third barriers for financial inclusion. The cost of financial services doesn’t seem to be much of a barrier, cited by only 5% of adults without an account. This is not surprising considering that banks and microfinance institutions (MFIs) provide free of charge basic financial transactions like opening an account, and making deposits and withdrawals. The minimum balance to open an account is less than a dollar (Birr 25).

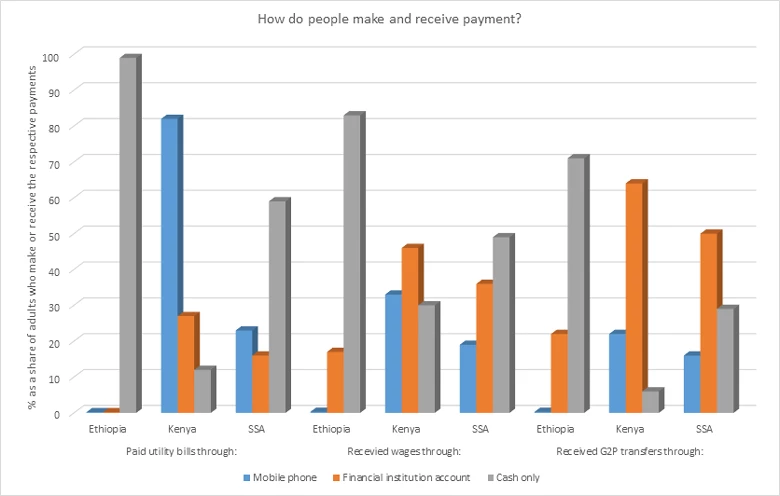

Cash is an overwhelmingly dominant payment method

Most people still rely on cash to pay utility bills and receive payments. Almost all (99%) adults pay utility bills with cash, compared to 12% of people in Kenya and 59% in the region as a whole.

Source: Global Findex database

Ethiopia is an outlier among its peers when it comes to access to and usage of digital financial Service

Ethiopia hasn’t taken advantage of digital financial services (DFS) that have driven access to and usage of financial services in Sub-Saharan Africa, as illustrated in the table below.

Ethiopia

Kenya

Rwanda

SSA Average

Mobile money accounts (in %, age 15+)

0.3

73

31

21

Debit card ownership (%, age 15+)

4

38

5

18

Made or received digital payments in the past year (%)

12

79

39

34

Paid utility bills using a mobile phone (out of adults who paid utility bills)

0

82

44

23

Paid utility bills using an account (out of adults who paid utility bills)

0.2

85

48

31

Received wages into an account (out of adults who received wages)

17

68

33

45

Received payments for agricultural products into an account (out of adults who received ag. payments)

1

46

14

Used a mobile phone or the internet to access a financial institution account in the past year (out of adults with a financial institution account, age 15+)

1

57

13

24

Source: Global Findex database

Should we blame low mobile phone subscription for low mobile money penetration?

Low mobile phone subscription is usually blamed for low mobile money account penetration in Ethiopia. But this isn’t really the case. Ethiopia had 34.7 million mobile subscribers in 2017 (

GSMA 2017 report,2017). But only 0.3% of adults had a mobile money account in the same year, according to Findex. About 13 million people with a mobile phone are unbanked. This illustrates that mobile phone adoption alone isn’t sufficient to drive mobile financial services. The ‘analog complements’ to digital financial service – such as regulation, skills and institutions -- could be behind low penetration of mobile financial services. This needs to be looked into further.

One fifth of Ethiopians would sell their assets to meet a need for small emergency funds

Asked if they could come up with an amount equal to 1/20 of Gross National Income (GNI) per capita in local currency within the next month, more than half of adults replied ‘yes’. However, most of these respondents said they would turn to family or friends, use money from working or sell their assets; only 18% of adults who reported being able to come up with emergency funds said they will rely on savings. Alarmingly, 21% of adults who reported that it was possible to come up with emergency funds, said they would sell their assets to come up with these emergency funds. This would imply that a large number of adults don’t have an alternative risk coping mechanism (e.g. insurance, saving or short-term credits). For more information on risks and coping mechanisms of low-income households in Ethiopia, please see

demand research conducted by the World Bank.

The Government of Ethiopia, with the support of WBG, launched a National Financial Inclusion Strategy (NFIS). The headline indicator for the strategy is to increase the percentage of adults with a transaction account from 22% in 2014 to 60% in 2020. The WBG is implementing eight Advisory Service and Analytics (ASA) projects, and two, line-of-credit operations aimed at advancing financial inclusion and access in Ethiopia.

Thank you for choosing to be part of the Africa Can End Poverty community!

Your subscription is now active. The latest blog posts and blog-related announcements will be delivered directly to your email inbox. You may unsubscribe at any time.

The e-mail address: [email] is already subscribed for newsletters.

Join the Conversation