Remittances to Sub-Saharan Africa (SSA) have increased steadily in recent decades and are estimated to have reached about $32 billion in 2013. Though studies have shown that remittances can affect aggregate financial development in SSA — as measured by the share of deposits or M2 to GDP (Gupta et al. 2009), to my knowledge there is no evidence for this region on the impact of remittances on household financial inclusion defined as the use of financial services. This question is important because there is growing evidence that financial inclusion can have significant beneficial effects for households and individuals. In particular, the literature has found that providing individuals access to savings instruments increases savings, female empowerment, productive investment, and consumption. Furthermore, the topic of financial inclusion has gained importance among international bodies. In May 2013, the UN High-Level Panel presented the recommendations for post-2015 UN Development Goals, which included universal access to financial services as a critical enabler for job creation and equitable growth. In September 2013, the G20 reaffirmed its commitment to financial inclusion as part of its development agenda.

In a recent paper, my co-author, Gemechu Ayana Aga and I explore the link between international remittances and one aspect of financial inclusion in SSA: households’ use of bank accounts.1 This issue is particularly important for SSA, given that on average only 24 percent of the population has an account with a formal financial institution. In contrast, 55 percent of adults in East Asia, 35 percent in Eastern Europe, 39 percent in Latin America, and 33 percent in South Asia have accounts.

Remittances may affect households’ use of bank accounts in at least two ways. First, remittances might increase the demand for savings instruments. The fixed costs of sending remittances make the flows lumpy, potentially providing households with excess cash for some period of time. This might increase their demands for deposit accounts, since financial institutions offer households a safe place to store this temporary excess cash. Second, remittances recipients’ exposure to banks, for example, when banks act as remittances paying agents, may familiarize them with the services offered by banks and increase their demand for bank accounts. Therefore, so long as lack of awareness is the main reason for households’ financial exclusion, remittances may increase households’ use of bank accounts.

Using World Bank survey data including about 10,000 households in five countries — Burkina Faso, Kenya, Nigeria, Senegal and Uganda — we find that receiving international remittances increases the probability that the household opens a bank account in all the countries in our study. This result is robust to controlling for the potential endogeneity of remittances, using as instruments indicators of the migrants’ economic conditions in the destination countries.

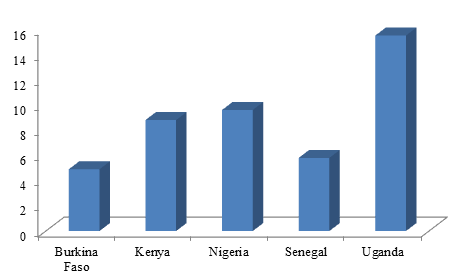

The size of the impact varies across countries (see Figure 1). In Kenya and Nigeria, receiving international remittances increases the probability of a household having a bank account by about 10 percentage points. The size of the coefficient is larger for Uganda, where receiving international remittances increases the probability of having a bank account by about 15 percentage points. The size of the coefficient is smaller for Senegal and Burkina Faso, where receiving international remittances increases the likelihood of having a bank account by about 5 and 6 percentage points, respectively.

Figure 1:

The impact of remittances on the likelihood that households own a bank account

Join the Conversation