The question has been asked often in the context of the post-2005 commodity price boom. In a recently published working paper,

What drives local food prices? Evidence from the Tanzanian maize market

, we examine the factors driving movements of prices in 18 major regional maize markets in Tanzania. The results underscore the importance of measuring and accounting for the influence of domestic drivers of local food prices, such as harvest cycles and weather disturbances. They also find that while the main external market (Nairobi) exerts a small, but statistically significant, influence on maize markets in Tanzania, the effect is much less than that of South Africa or the US market, often considered the “world” price.

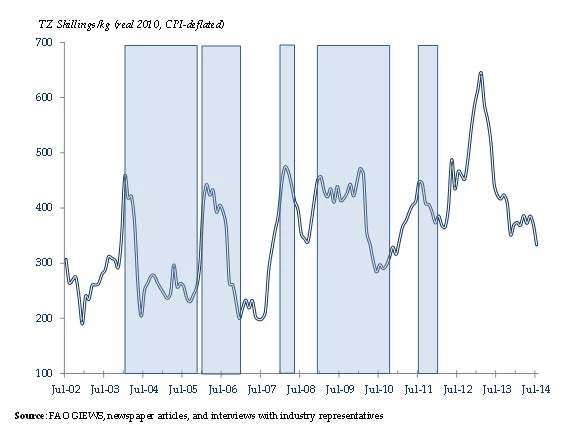

Perhaps most importantly, because the Tanzanian maize sector is subject to government control, export bans are also an important driver of maize prices. While export bans increase domestic supplies of maize (which is typically the government’s stated objective), they do so at the expense of depressing domestic prices, consequently dampening incentives to improve agricultural productivity. For example, between August 2002 and August 2014, export bans were imposed during 65 of the 144 months (see Figure 1). While the bans did succeed in lowering maize prices. From the perspective of rural households, this uncertainty is of grave importance—because the value of their produce, in many cases the basis of their livelihoods, is subject to unanticipated shocks.

Figure 1 Maize price in Dar es Salaam and export bans

The paper finds two mechanisms that may reduce price uncertainty arising from domestic sources. First, investments that engender a shift away from primitive agrarian techniques and towards more modern production and marketing methods may partially mitigate the impact of domestic weather shocks—less than 10 percent of households in mainland Tanzania have access to irrigation and the main maize surplus area has poor transport infrastructure. Second, and perhaps more importantly, a more open trade policy regime lessens the influence of domestic shocks, especially the ones associated with weather.

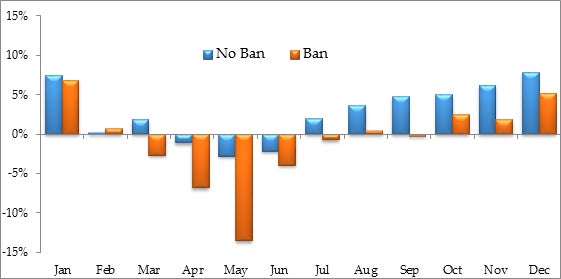

The difference in monthly price changes between periods during which the export ban was effective and periods when it was not, is particularly large at the start of the southern harvest season in May (Figure 2). When the export ban is imposed and the harvest is good, it will result in a large fall in local prices at precisely the time when rural households would like to sell their produce. This is surprising since the surplus cannot be exported because of the export ban. This result highlights an even more important issue. If climate change will increase the frequency of weather disturbances, trade will become even more relevant in the future.

Figure 2 Average price change during ban and no ban periods

Source: Authors’ calculation based on unadjusted price data

The study, which constitutes an early attempt to simultaneously measure the impacts of both external and domestic drivers of food prices, also provides a dynamic picture of the Tanzanian rural economy – one that may complement the less dynamic, but more granular, perspective that is gained through an analysis of household surveys.

Perhaps most importantly, because the Tanzanian maize sector is subject to government control, export bans are also an important driver of maize prices. While export bans increase domestic supplies of maize (which is typically the government’s stated objective), they do so at the expense of depressing domestic prices, consequently dampening incentives to improve agricultural productivity. For example, between August 2002 and August 2014, export bans were imposed during 65 of the 144 months (see Figure 1). While the bans did succeed in lowering maize prices. From the perspective of rural households, this uncertainty is of grave importance—because the value of their produce, in many cases the basis of their livelihoods, is subject to unanticipated shocks.

Figure 1 Maize price in Dar es Salaam and export bans

The paper finds two mechanisms that may reduce price uncertainty arising from domestic sources. First, investments that engender a shift away from primitive agrarian techniques and towards more modern production and marketing methods may partially mitigate the impact of domestic weather shocks—less than 10 percent of households in mainland Tanzania have access to irrigation and the main maize surplus area has poor transport infrastructure. Second, and perhaps more importantly, a more open trade policy regime lessens the influence of domestic shocks, especially the ones associated with weather.

The difference in monthly price changes between periods during which the export ban was effective and periods when it was not, is particularly large at the start of the southern harvest season in May (Figure 2). When the export ban is imposed and the harvest is good, it will result in a large fall in local prices at precisely the time when rural households would like to sell their produce. This is surprising since the surplus cannot be exported because of the export ban. This result highlights an even more important issue. If climate change will increase the frequency of weather disturbances, trade will become even more relevant in the future.

Figure 2 Average price change during ban and no ban periods

Source: Authors’ calculation based on unadjusted price data

The study, which constitutes an early attempt to simultaneously measure the impacts of both external and domestic drivers of food prices, also provides a dynamic picture of the Tanzanian rural economy – one that may complement the less dynamic, but more granular, perspective that is gained through an analysis of household surveys.

Join the Conversation