أنقاض قصبة تقف بين المنازل السكنية في قرية حديثة بجبال الأطلس بالمغرب بسبب زلزال 8 سبتمبر 2023

أنقاض قصبة تقف بين المنازل السكنية في قرية حديثة بجبال الأطلس بالمغرب بسبب زلزال 8 سبتمبر 2023

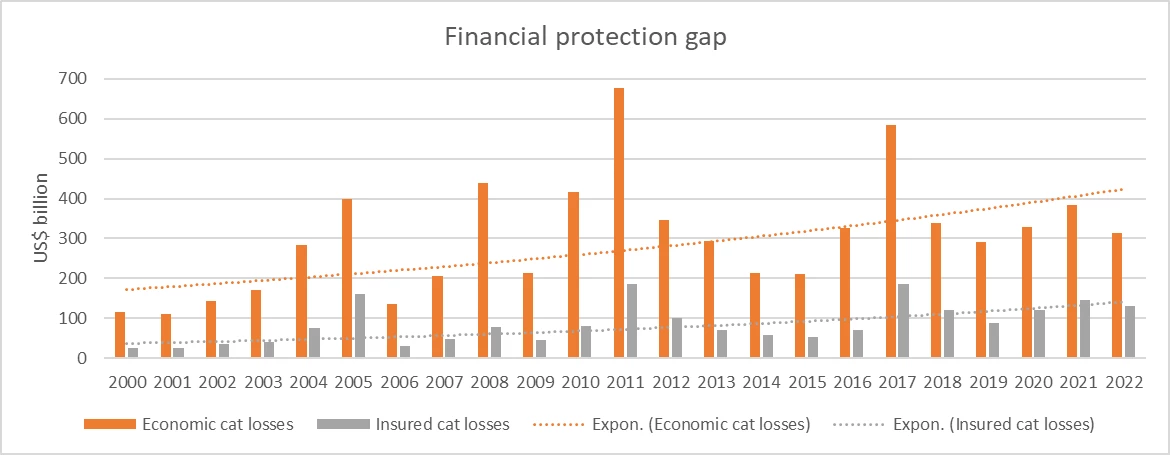

The financial protection gap against climate shocks and disasters is widening. Morocco was hit by an earthquake in September 2023, affecting more than 300,000 people in Marrakesh and surrounding areas. The direct physical damages from this disaster are estimated at US$3 billion (2.6% of GDP).

Worldwide Financial Protection Gap

To respond to the emergency needs of the affected population, Morocco was able to leverage its dual public-private financial protection program, including catastrophe risk insurance. The official declaration of “natural disaster” in October 2023 allowed for the registration of victims so that the domestic private insurance sector and Solidarity Fund (FSEC) could compensate them. The FSEC was able to mobilize the accumulated reserves from the parafiscal tax proceeds (US$50 million) and then activating a US$275 million insurance payout under its earthquake reinsurance policy.

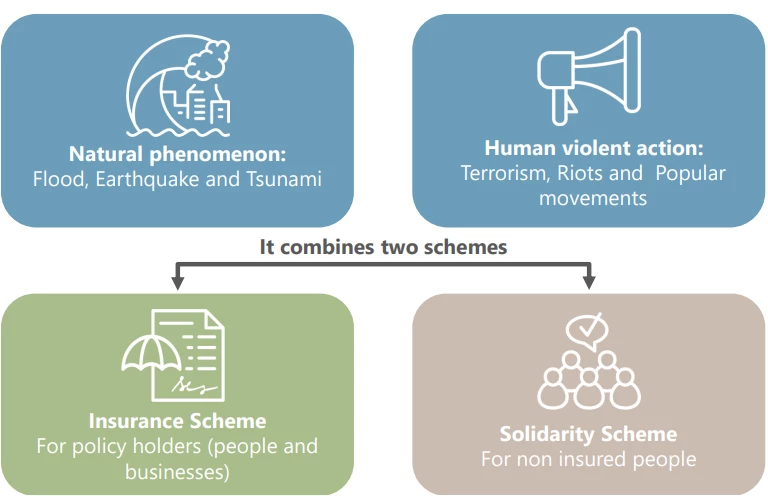

Morocco’s financial protection program relies on a dual public-private system, the first of its kind. This dual scheme builds on market-based insurance and solidarity principles to protect insured and uninsured households against disasters. Insured households are covered through a compulsory extension of guarantees against catastrophe risks in property insurance policies. Given Morocco’s low penetration of property insurance (below 5%), only a small fraction of houses is covered against catastrophic events. To compensate uninsured households affected by disasters, the government established a dedicated public Solidarity Fund. This differs from most catastrophe insurance programs in emerging and developing economies where uninsured households affected by a disaster can only rely on ad-hoc financial support.

The dual public-private financial protection program was the result of several years of preparation and implementation led by the government in partnership with the domestic insurance industry and technical and financial assistance from the World Bank (WB) and SECO through the WB Disaster Risk Financing and Insurance Program. Here are six lessons for other countries:

Dual financial protection system in Morocco

- Understand the underlying physical risks and their financial impacts to prepare for liability-payout projects. In the wake of the 2004 earthquake in Al Hoceima, the government and WB had initiated a collaboration on disaster risk management and financing. The first phase (2008-2013) focused on technical assistance and risk modeling to improve the understanding of catastrophe risks, contingent liability for disasters for the government, and the capacity of the domestic private insurance underwrite such risks. This was achieved through close collaboration with the Moroccan insurance regulator and Insurance Federation, which quantified where and how catastrophes were prevalent in Morocco. This helped to inform the most recent resilience response in 2023.

- Leverage the financial markets and partners across a public-private partnership. Firstly, national insurers offer a compulsory extension of catastrophe cover in their property insurance policies, enabling insured households to be covered against disasters. Secondly, international reinsurers provide reinsurance capacity to domestic insurers through treaties. In addition, the Solidarity Fund designed its financial risk-layered strategy based on public resources to cover small losses and private capital to cover excess losses. A parametric earthquake insurance policy was underwritten in 2019 and been renewed since triggering a payment of US$275 million following the 2023 earthquake. The Solidarity Fund can also mobilize private capital through alternative risk transfer solutions like catastrophe bonds.

- Set up an enabling legal and regulatory environment. This dual approach was successful in Morocco because it was institutionalized with the adoption of Law 110-14 in 2016, which defined the scope of financial protection, including perils covered (earthquakes, floods, tsunamis) and damages (bodily injury and residential losses). The law also established FSEC as a legal entity.

- Operationalize the disaster risk finance strategy. To operationalize the program, the Solidarity Fund was created through WB technical and financial support. Operationalization of the fund required expertise and financial support to develop a sustainable governance, technical, and financial structure. The Solidarity Fund relies on a parafiscal tax on non-life insurance policies, generating about US$25 million per year, enabling accumulation of reserves and the purchase of insurance for excess losses. The victims’ registration system was a critical step to ensure that affected households could register and be eligible for compensation.

- Complement financing resilience with physical resilience. Reinforcing its physical stability has complemented these efforts to strengthen the country's financial resilience by redesigning Morocco's disaster fund from an emergency response vehicle into a national resilience fund. As of March 2022, the fund has supported 180 disaster risk reduction projects, for an investment of US$304 million, with the fund co-financing US$111 million, benefitting more than 174,000 people.

- Continuously improve the program to respond to a changing world. Such programs need continued improvements to better respond to the needs of the beneficiaries. Disasters are evolving in the context of climate changes, and vulnerability and exposure of people change as the economy grows. The WB and the Global Risk Financing Facility are assisting the government of Morocco in further strengthening its technical, operational, and financial capacity by incorporating climate change into its modeling. Moving forward, this program could expand to cover new perils (drought, pandemics) and new assets (critical infrastructure).

Join the Conversation