Illustration of debt increase. | © Adobe Stock

Illustration of debt increase. | © Adobe Stock

Credit markets are often affected by market failures, which makes them prone to government interventions. While there are many ways in which governments can intervene in financial markets, a common method is through state-owned banks. These financial intermediaries allow governments to lend directly to households and firms and are commonly found across the world. Development and commercial government banks are frequently used for interventions in credit markets during crisis, in a countercyclical style. Nevertheless, there is little consensus about how programs based on lending by government banks affect private banks, and how adjustments in private lending would change the effects of these policies. This raises an important question: what happens when state-owned banks are used in normal times to address market failures?

In our recent working paper, we address this question by exploring a large-scale program implemented in Brazil. In March 2012, the Brazilian government announced an increase in the credit supply of two of its largest commercial banks, which, together, were responsible for 38 percent of the outstanding credit in Brazil before the intervention. Focusing on term loans to firms, we document a large increase in the amount of lending by public banks, at much lower loan interest rates than charged by private banks. We show that while there were benefits from the increase in lending by government banks, such as a reduction in loan interest rates and positive employment effects, there were also large costs, linked to an increase in corporate debt and higher loan default rates for state-owned banks.

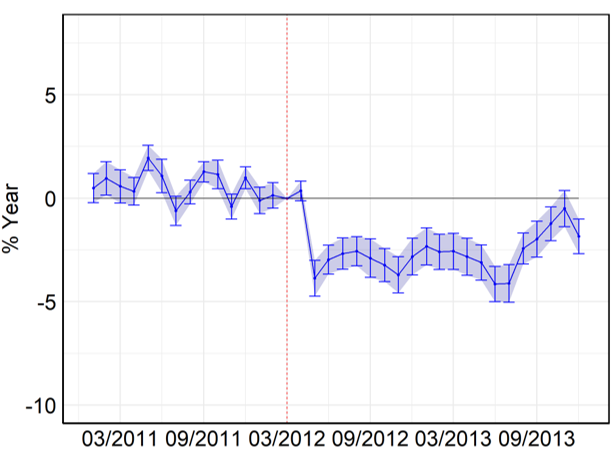

To perform a broad and comprehensive overview of government interventions in credit markets is a challenging endeavor. The decision to intervene, adjustments made by private banks in their loan interest rates, and outcomes of the borrowers that benefit from the intervention can be correlated with unobservable economic characteristics that can bias the analysis. The richness of our data and the unique setting in which we perform our evaluation – namely, outside a financial crisis – enable us to overcome these challenges. When documenting the effects of the policy on loan interest rates and firm leverage and default, we focus on loans and firms with identical characteristics – such as the same sectors, location, and (in the case of loans) maturity. This allows us to isolate specific changes that were due to the introduction of the policy in early 2012. Figure 1 shows the evolution of the difference in interest rates of private and public banks. The negative coefficients after March 2012 indicate that private banks greatly reduced their interest rates in response to the increase in lending by state-owned banks.

Figure 1. Difference in loan interest rates of private and public banks

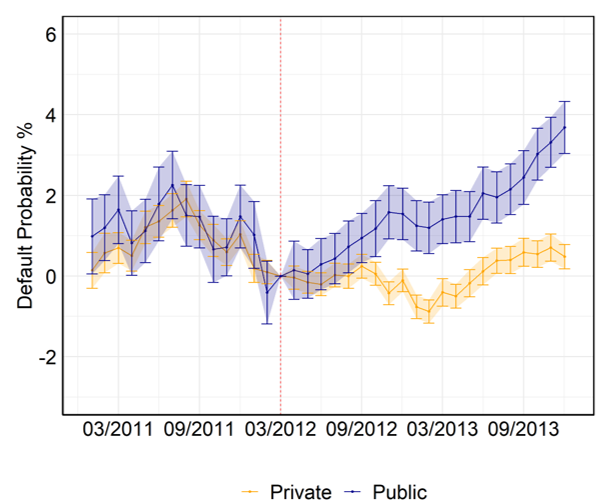

The increase in lending also benefited firms that had access to public banks and led such firms to become more levered compared with firms that borrow exclusively from private banks. The increase in leverage and the difference between the interest rates charged by public and private banks can both affect firm loan default risk. We link these differences to the policy by comparing the delinquency rates of very similar firms that borrow from government and private banks. Figure 2 shows the delinquency trajectories for public and private banks, relative to their delinquency when the policy was announced. Importantly, the dynamics of delinquency rates for the two banks were quite similar until the policy was announced. After that, public banks experienced a deterioration in the quality of their loan portfolio. This difference only exists when looking at levered firms, with unlevered borrowers of public and private banks (mostly firms without outstanding loans) having similar risk. Furthermore, the difference in delinquency rates between government and private banks after the policy increases with larger firm leverage. Therefore, the increase in leverage led to the variation in delinquency rates after the policy, overcoming potential benefits to public banks due to their lower loan interest rates.

Figure 2. Delinquency trajectories for public and private banks

The last step in our analysis is to understand whether the credit expansion by public banks had positive effects on employment and output. Our analysis comparing similar firms suggests that firms with access to public banks increased their employment after the policy. However, to the extent that all firms, both those who enjoyed lower interest rates from private banks and those who could borrow larger amounts from state-owned banks, benefited from the policy, this simple analysis can lead to biased results. To overcome this challenge, we compare employment and output in neighboring cities with different degrees of exposure to public banks, as measured by their market share pre-intervention. Comparing neighboring cities allows us to isolate any variation due to different types of regional economic activity, which increases the confidence that our results indeed capture the effect of the increase in public credit. This regional exercise reveals that, indeed, the increase in credit was associated with larger output and employment growth in cities that were more exposed to state-owned banks. However, the implied elasticity of output growth with respect to credit growth is modest compared to other studies of the real effects of changes in credit supply.

In summary, our study provides a detailed exploration of the costs and benefits of interventions that make use of lending by state-owned banks. While there are potential benefits from added competition and consequently lower interest rates charged by private banks, the real effects are modest and come at the cost of higher firm leverage and default. Our results suggest that policy makers should not underestimate the costs of added leverage and default that can come from public lending programs outside financial crisis, even when offering lower loan interest rates than prevailing market rates.

The views expressed herein are those of the authors and do not indicate concurrence by the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System. The views expressed herein do not necessarily reflect those of the Bank of England or its committees. The views expressed herein do not necessarily reflect those of the Banco Central do Brasil.

Join the Conversation