Aerial view of combine harvester.

Aerial view of combine harvester.

The global recession caused by the pandemic in early 2020 led to a widespread collapse in commodity prices. The collapse was followed by a synchronized sharp rebound in prices. Such synchronized booms and slumps in commodity prices have been common in recent decades. In the years ahead, the transition away from fossil fuels to low-carbon technologies will cause profound, far-reaching shifts in the pattern of demand and supply for commodities, which can have major macroeconomic consequences. Commodity-exporting emerging market and developing economies (EMDEs) generally need to take steps to better manage future commodity price shocks and to reduce their reliance on commodities.

Read more on the topic in the January 2022 Global Economic Prospects.

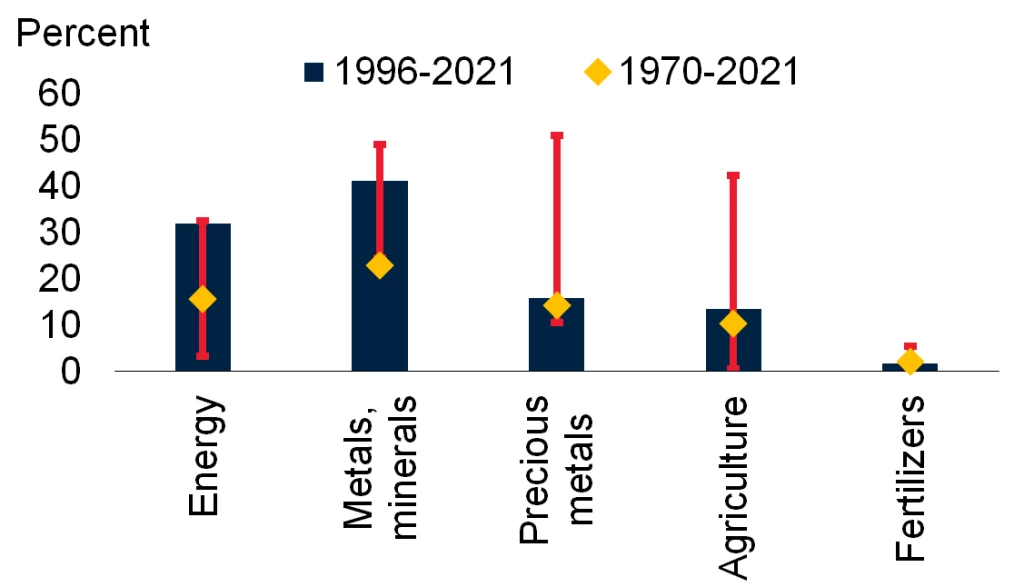

Price cycles are highly synchronized across commodities.

Commodity prices have undergone repeated cycles over the past 50 years and these price cycles have been highly synchronized across commodities. A common “global factor”—a common factor derived from 39 commodity price series—accounted, on average, for roughly 15-25 percent of the price variability for energy and metals, but only 2-10 percent for agricultural commodities and fertilizers. The synchronization in prices has become more pronounced over time for industrial commodities. Since the mid-1990s, on average, the common global factor accounted for about 30-40 percent of the variability in industrial commodity prices—twice as much as during the 1970-2021 period.

Commodity price variation due to the global factor, 1970-2021 and 1996-2021

Sources: Baumeister and Hamilton (2019); Ha, Kose, and Ohnsorge (2021); Kabundi and Zahid (Forthcoming); World Bank.

Note: Share of variation in month-on-month growth of 39 commodity prices—for 3 energy commodities, 7 metal and mineral commodities, 3 precious metals, 5 fertilizers, and 21 agricultural commodities—accounted for by the global factor and derived from a one-factor dynamic factor model as in Kose, Otrok, and Whiteman (2003). Bars show consumption-weighted averages. Whiskers indicate range from minimum to maximum during 1996-2021.

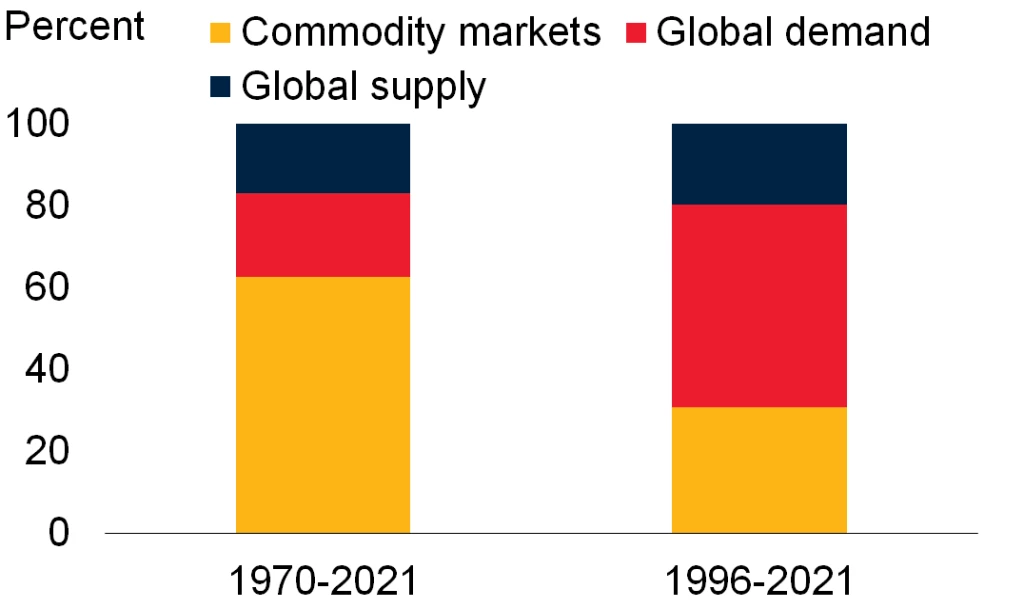

Global macroeconomic shocks have become the main source of commodity price volatility.

Since 1996, global macroeconomic shocks have been the main source of commodity price volatility. Global demand shocks have accounted for 50 percent of the variance of global commodity price growth, while global supply shocks have accounted for 20 percent of the variance. In contrast, between 1970 and 1996, supply shocks specific to particular commodity markets—such as the oil price shocks of the 1970s and 1980s—were the main source for variability in global commodity price growth.

Contributions of global shocks to the variation in global commodity prices

Sources: Baumeister and Hamilton (2019); Ha, Kose, and Ohnsorge (2021); Kabundi and Zahid (Forthcoming); World Bank.

Note: For technical details, see the January 2022 Global Economic Prospects.

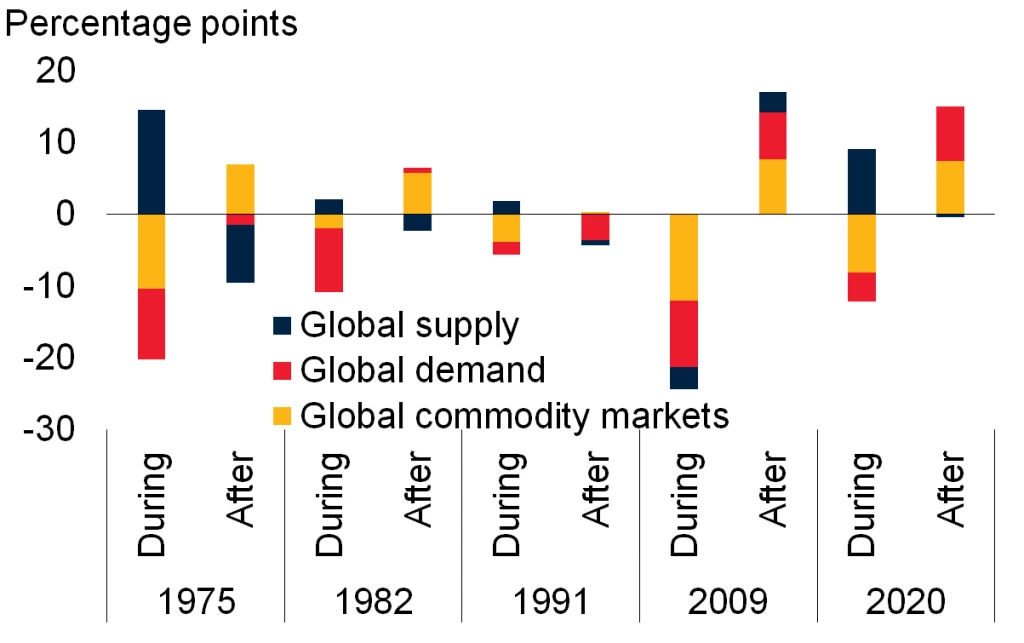

Global recessions have been accompanied by demand weakness and supply disruptions.

In the past, global recessions have been associated with weak demand and disruptions in supply, which combined to depress commodity prices. Market disruptions in specific commodities have sometimes provided an offset. During global recessions, demand pressures on commodity prices were compounded by supply pressures specific to commodity markets (1975, 1991, 2020); in 1975 and 2020, these were offset by supply pressures resulting from large-scale trade embargoes (in 1975) or widespread supply chain disruptions (in 2020). The recovery of commodity prices after recessions has been driven by an unwinding of supply or commodity market shocks and, since early 2000, also by rebounds in demand. Consistent with this, the surge in commodity prices in 2020-21 can be explained by a strong resurgence of demand, combined with unusually widespread supply bottlenecks.

Contributions of global shocks to the variation in global commodity prices around recessions and slowdowns

Sources: Baumeister and Hamilton (2019); Ha, Kose, and Ohnsorge (2021); Kabundi and Zahid (Forthcoming); World Bank.

Note: For technical details, see the January 2022 Global Economic Prospects.

Policy options

Global macroeconomic shocks have become the main source of fluctuations in commodity prices, accounting for more than two-thirds of the variance of global commodity price growth. The swings in commodity prices witnessed in 2020-21 have brought to the fore the vulnerabilities of the many EMDEs, especially low-income countries (LICs), highly dependent on commodity exports. Recent events have also highlighted how climate change is a growing risk, including to energy markets, affecting both demand and supply.

Commodity-exporting EMDEs have multiple policy options to smooth the near- and long-term effects of commodity price swings and, more broadly, to reduce their reliance on commodities. Countries can strengthen their fiscal, monetary, and prudential policy frameworks. They can also take measures to reduce their reliance on commodities by encouraging diversification of exports and, more importantly, “national asset portfolios”—investing to diversify their physical and human capital, and strengthen their institutions.

References

Baumeister, C., and J. D. Hamilton. 2019. “Structural Interpretation of Vector Autoregressions with Incomplete Identification: Revisiting the Role of Oil Supply and Demand Shocks.” American Economic Review 109 (5): 1873-1910.

Ha, J., M. A. Kose, and F. Ohnsorge. 2021. “One-Stop Source: A Global Database of Inflation.” Policy Research Working Paper 9737, World Bank, Washington, DC.

Kabundi, A., and H. Zahid. Forthcoming. “Commodity Price Cycles: Commonalities, Heterogeneities, and Drivers.”

Kose, M. A, C. Otrok, and C. H. Whiteman. 2003. “International Business Cycles: World, Region, and Country-Specific Factors.” American Economic Review 93 (4): 1216-1239.

Join the Conversation