This is the first blog post I write after revisiting China’s recent economic developments, the outlook, and policy implications as part of writing our latest China Quarterly Update. After this general overview I will in a few days write one on some interesting medium term trends on relative prices and the relative importance of external trade in China’s economy (they are also discussed in the Quarterly).

The term “normalization” has been used a lot lately in relation to the composition of growth and macroeconomic policy stance, also in China. But it is hard to avoid it. During 2010, China’s composition of growth started to “normalize”—as in look like it typically does—after the spectacular developments in 2009, when a massive government-led domestic demand surge offset a huge contraction in exports. Later in 2010, the macroeconomic policy stance also started to “normalize”. I guess many of us use the word “normalization” to describe or prescribe a macro policy stance that would be in line with the “normalized” economic outlook, as opposed to a particularly tight stance.

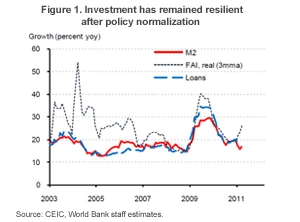

In discussions on the normalization of the macro stance most of the attention tends to go to the monetary side. In particular, the multiple increases in interest rates and RRRs since October 2010 have been in the headlines. More importantly, though, the authorities re-inforced the “window guidance” on bank lending, especially this year. As a result, credit and M2 growth slowed in early 2011, regardless of how broad your definition of total bank credit is (the Quarterly discusses how in recent years total bank credit extension has been quite a bit larger than the headline data suggests).

Actually the fiscal side is important too. When we look at China’s overall fiscal accounts, including the social security funds, the extra-budgetary funds and the quasi fiscal activity carried out by local government investment platforms, fiscal policy was highly expansionary in 2009. But the overall fiscal accounts for 2010 and 2011 do not imply stimulus—rightly so, given that the economy operates close to full capacity.

The economy held up well against this normalization of the macro stance. Quarter on quarter GDP growth eased to 8.7% in the first quarter of 2011 at a seasonally adjusted annualized rate (SAAR), according to the new estimates of the National Bureau of Statistics (NBS), leaving output up 9.7% on a year ago. Our own estimates suggest somewhat faster sequential growth.

After contributing significantly to growth in 2010, the contribution of net external trade to real GDP growth came down to broadly zero in the first quarter. With the terms of trade falling because of the surge in raw commodity prices, the trade balance declined substantially in the first quarter.

Inflation—the key priority of policymakers

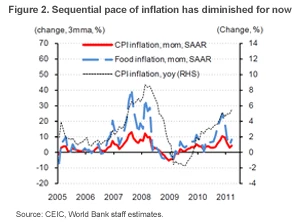

Meanwhile, the increase in inflation to 5.4% in March has received a lot of attention. So far inflation has basically been driven by higher food prices, caused by problematic weather domestically last year and hikes in international food prices.

Vegetable prices, the key driver in 2010, have come down recently, sequentially, after peaking in February, in part because of measures taken. In addition to normalizing the macro policy stance the government took some measures to boost food supply and reduce the cost of production and logistics, limit the increase in domestic fuel prices arising from higher oil prices and applied moral suasion on manufacturers of food and consumer products. It also allowed some appreciation against the US dollar, although the RMB depreciated in nominal effective terms.

As a result, the (yoy) rate of increase in food prices is likely to diminish later in the year. Much of the higher prices of other raw materials is still in the pipeline. But so far core inflation remains low. It was 2.3 percent in March (yoy). Based on the (fairly benign) global price outlooks of the World Bank and the IMF, the moderation in food price inflation in the coming 12 months should more than offset the rise in non-food inflation, resulting in a slowdown in headline CPI inflation.

Other aspects of the outlook

The growth economic outlook remains broadly favorable. The global growth outlook has so far been little affected by the higher raw commodity prices and the earthquake in Japan. Domestically, there is some headwind from the tighter macroeconomic stance, inflation, and somewhat slower global growth. However, this is likely to be partly offset by solid corporate investment and a still robust labor market. Mainstream housing construction is likely to slow down. But this should in part be compensated by the government’s ambitious social housing construction plans. In all, with a broadly neutral contribution of net trade, real GDP growth of 9.3 percent in 2011 and 8.7 % in 2012 is in reach.

Because of the surge in raw commodity prices the current account surplus should show another decline this year. However, whether the trend towards a lower external surplus and lower dependence on external trade will be sustained remains to be seen (the quarterly looks at it and I will write a blog about it).

Notwithstanding the (sanguine) outlook, there are risks, on inflation and otherwise, and a fully normalized macro policy stance is needed to address them. One key risk on prices is further increases in global raw material prices. To address inflation risks at a time of high inflation expectations and with little spare capacity in the economy, macro policy is typically better placed than moral suasion and administrative measures. It seems too early to stop the macro tightening. Two way risks are better dealt with by maintaining fiscal and monetary flexibility.

While the macro and financial risks on the property market require macroeconomic measures and reforms, social concerns require a different policy response. On the property market, Macro and financial policy is supposed to prevent different types of risks from building up and make the economy and the financial system robust to a possible property downturn, rather than mainly focus on containing overall housing prices. In any case, If housing prices are considered systematically too high from a market perspective, macroeconomic levers are more obvious than administrative measures, especially locally administered ones.

On the other hand, making housing more affordable for targeted groups requires sustainable rules-based arrangements, almost unavoidably explicitly subsidized by the government. The scaling up of social housing is in the right direction. However, finding a transparent, rules based financing model is key.

The Quarterly also discusses several aspects of the 12th 5 Year Plan. Its two key overall objectives are rebalancing and industrial upgrading and moving up the value chain in manufacturing. Policy-wise, it is important to find the right balance between these two.

In all, still a rather favorable outlook, especially if the right policy instruments are used to achieve the different objectives.

Join the Conversation