This is the second in our series of posts by students on the job market this year.

In 2013 alone, donors pledged $31 billion to support financial inclusion programs—an attempt to deliver financial services to the 2 billion adults that do not have access to such services. In the past, microcredit and insurance programs received all of the attention, but improving the savings capacity of the poor and unbanked has recently drawn increasing attention as well. Access to a savings account has been shown to improve account holders' overall financial situation and their ability to cope with shocks. In addition, access to savings may also lead to greater educational aspirations and completion of additional years of schooling for the children of account holders.

A complete evaluation of the welfare benefits of microsavings programs should also account for the indirect effects, or spillovers, on the social and financial networks in which individuals are embedded. In Nepal and Malawi, some positive spillovers have been documented. Can microsavings programs have negative spillovers? In my job market paper, I study the effects of access to savings on one’s risk-sharing network, a type of financial network where negative spillovers are most likely to occur, if at all they do.

In risk-sharing arrangements, as with many informal institutions, trust makes up for the absence of written binding contracts. Access to savings can reduce this trust, because it increases the incentive to break one’s promise to provide support. At the extreme, access to savings can reduce overall welfare by crowding out risk-sharing and reducing the ability to smooth consumption.

The Experiment

We use data from vulnerable women in Kenya to undertake the first study to document the negative effect of access to savings on risk-sharing. In Kisumu, Kenya, we randomly assigned 627 participants to treatment and control groups. The treatment was a microsavings program which included enrollment in a mobile money savings account, a session in which women set savings goals, and the receipt of weekly SMS reminders about these goals.

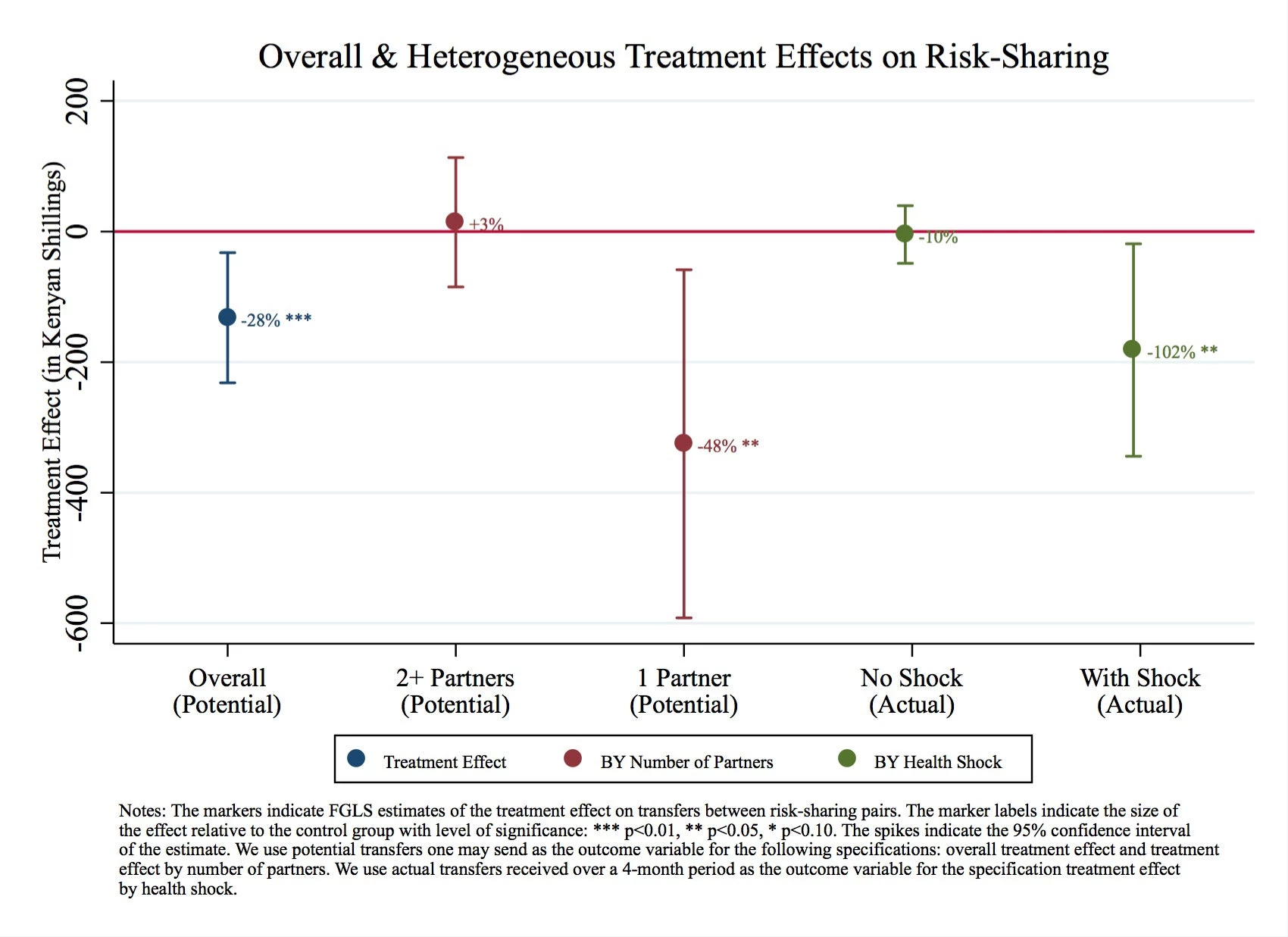

A key highlight of the paper is that we carefully identify interpersonal risk-sharing as ex-ante (pre-shock) agreements about mutual and state-contingent support. That is, we recognize that the value of risk-sharing is the insurance it provides against potential shocks, and actual interpersonal exchanges are merely manifestations of this ex-ante agreement. Also, of the various types of informal insurance, risk-sharing is unique in that the direction of support goes both ways and the necessity of mutuality is what generates the trust problem. We thus measure risk-sharing as potential (rather than actual) transfers received and sent between two individuals who can mutually rely on each other. We do this by asking “what is the maximum amount that this person (you) would give you (this person) in the event that you (this person) faced an unexpected expense?”

Results

First, in a separate working paper, we show that the microsavings program had a positive (but imprecisely estimated) effect on savings. The program did lead to statistically significant increases in savings for those who report having problems saving due to spending on temptation goods. Those facing temptation constraints saw an over threefold increase in mobile banking savings due to the intervention.

Second, we show that the microsavings program reduced risk-sharing. Several months after the intervention, we find an individual with access to the microsavings program reduced the potential value of transfers received from and sent to her risk-sharing partners by 21% and 28%, respectively. Actual transfers received and sent also decreased, particularly among those who experienced a negative health shock. This suggests that our result is not driven by some oddity of the potential (hypothetical) transfers measure. Treatment women who experienced a shock received 102% less transfers relative to control women who also experienced a shock. The size of the decrease in transfers is 78% of the median cost to treat a health shock. The figure below summarizes these results.

Interestingly, the negative effect is concentrated among those who report to have only one risk-sharing partner; and consistent with this result, we find that risk-sharing instead increased between partners of partners. These findings imply that the trust problem in risk-sharing arrangements may be worse when one has only a few risk-sharing partners, and that safety nets are especially important for those who have smaller risk-sharing networks.

More generally, our results suggest that formal financial inclusion programs can undermine existing informal institutions. Interventions aimed at strengthening trust in existing informal institutions may be a useful endeavor, such as initiatives to support Village Savings and Loans Associations (VSLAs) in Mali and initiatives to support informal burial associations (IDDIRs) in Ethiopia.

While we document that the microsavings program reduced transfers within one’s risk-sharing network, we cannot conclusively say whether reduced transfers led to negative welfare impacts among risk-sharing partners. We find no negative impacts on the network members’ food security or ability to meet non-food expenses. It may well be that the negative effect on risk-sharing may be too small relative to the full portfolio of risk-coping strategies, and as such the net effect on food security is zero. Indeed, our intervention helped women to build rather small buffer stocks. It remains an open and important question whether microsavings programs that enable individuals to build much larger buffer stocks would impact the welfare of one’s risk-sharing network.

Similar to many other microsavings programs discussed above, we had shown that our intervention had direct benefits to program recipients. The overall welfare gains to microsaving programs can likely outweigh the consequences of reductions in risk-sharing. Nonetheless, program design could be improved by identifying possible welfare losses and minimizing such losses if they exist.

Felipe Dizon is a PhD Candidate at the University of California, Davis. He is on the job market this year; more details about his research can be found on his personal webpage.

Join the Conversation