William Baah-Boateng, a guest blogger, is Senior Lecturer in Economics at the University of Ghana.

After recovering from recession in the early 1980s, Ghana’s growth hovered around 5% but rose in the current millennium to about 7% annually. A rebase of the national accounts in 2006 pushed the country’s per capita income over the US$1,000 minimum threshold and Ghana gained entry into the league of middle income countries in 2007. The country also commenced commercial production and exports of oil in 2011, which aided growth to reach the highest levels in the country’s history. Ghana officially became one of the fastest growing economies in the world.

The country managed to achieve the key MDG goal of halving poverty ahead of the target period, with a decrease from 51.7% in 1991/92, to 24.2% in 2012/13. However, the depth of poverty remains a challenge, with a considerably high poverty gap ratio of 34.2. Moreover, income inequality continues to widen with the Gini coefficient rising from 38.1 to 42.3 over the same period.

The effect of the impressive growth of the economy on job creation has also been questioned, with the employment output elasticity declining since the 1990s (see Aryeetey and Baah-Boateng, 2015). There has been a shift in employment away from agriculture to low productivity service activities. The labor market is also dominated by low-earning self-employment in the informal sector. Indeed, employment growth in the country has largely occurred in the informal sector, reflecting an increased share of employment in the sector from 84% in 1984 to 88% in 2013. Consequently, working poverty (an outcome of a high proportion of low-paid and vulnerable employment) remains high at 22%, suggesting that at least one of every five working Ghanaians is poor.

As part of fiscal reform measures to address the country’s fiscal deficit challenge, the government undertook public sector retrenchment and privatization of State Owned Enterprises (SOEs) in the 1980s and 1990s and a freeze on new recruitment in the public sector to avoid over-bloated public sector and manage the high public sector wage bill. This has contributed to the dwindling size of public sector employment to 5.7% of total employment in 2014 compared to 10.2% in 1984. At the same time, the private formal sector is struggling in an insecure macroeconomic business environment, with an unstable exchange rate, and high interest and inflation rates, coupled with unreliable supply of power and generally weak infrastructure. It is increasingly difficult for employment in this sector to expand.

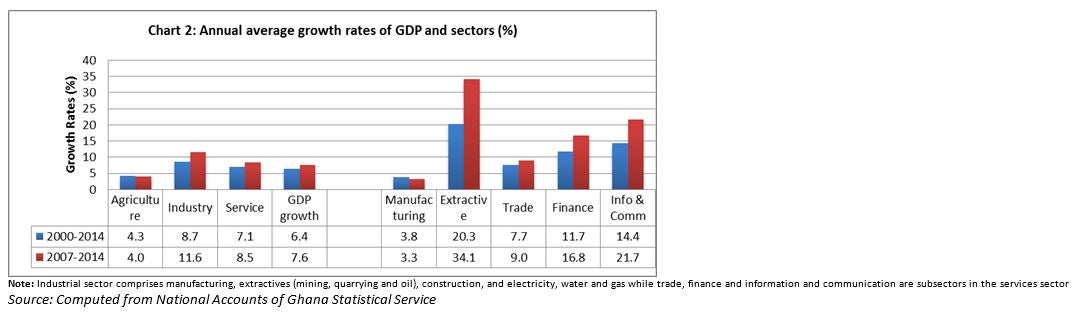

Weak job creation and widening income inequality, in the midst of a long period of strong economic growth, have also been linked to the sources of that growth. Indeed, the major driving force behind Ghana’s strong growth has been strong growth in extractives, and in the services sector. With the exception of trade (and to some extent information and communication activities), financial intermediation and extractive activities are associated with limited employment generation. As Chart 2 shows, between 2000 and 2014, the extractive sub-sector (mining and oil) of the industrial sector grew annually by 20.3% on average, and in the last eight years that growth accelerated to 34.1%. Financial intermediation also expanded by 11.7% in fifteen years, while information and communication, and trade, recorded 7.7% and 14.4% annual average growth rates, respectively.

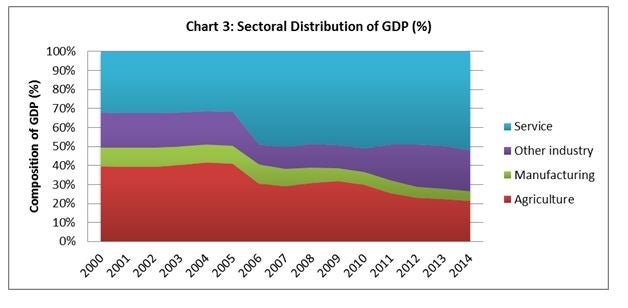

In contrast, manufacturing and its backward linkage sector of agriculture are thought to have better job creation effects. But they have recorded weak annual growth rates of 3.8% and 4.3% respectively over 2000-2014 - dropping to 3.3% and 4.0% in the last eight years. Consequently, the contributions of these two high labor-absorbing sectors have dwindled from about half of GDP at the beginning of the millennium, to just about a quarter today. In addition, manufacturing’s share of GDP declined continuously by more than half from 10.1% to 4.9%, while the size of agriculture output also dropped by almost half from 39.4% to 21.5%. In contrast, services output expanded substantially from about a third to more than half of total national output. Similarly, the output of other subsectors of the industrial sector, which dwindled from 18.3% in 2000 to 10.6% in 2006, jumped to 21.7% in 2014 as a direct consequence of the rebase of national accounts, and faster growth of mining and oil extraction. Clearly, while some level of growth has been recorded in agriculture and manufacturing, the reality is that it has been outpaced by growth in services and extractives (mining and oil) sectors and thus reducing the share of the two sectors in GDP.

It is difficult to interpret the shift from agricultural dominance to a service led economy, within the framework of dwindling manufacturing activities, as amounting to structural economic transformation. Essentially, the path of structural economic transformation begins with a shift from the dominance of primary activities to secondary-led manufacturing activities. It ends with a high productive tertiary-led economic structure in terms of both output and employment.

However, in Ghana’s case, the path of economic transformation appears to have skipped manufacturing from primary to a rather low productive tertiary activity with adverse implication for quality of employment generation. Thus, besides the virtual collapse of manufacturing activities, increased employment in services emanates from a shift from low productive agriculture labor to informal-dominated services. Employment in manufacturing has also suffered a decline (particularly in waged manufacturing jobs) in terms of its share in total employment, while the jobs that emerged in the services sector are mostly informal, resulting in low productivity growth in the sector. The low productive service sector dominated by informal economic activities cannot effectively support the manufacturing and agriculture sectors towards the goal of high-productive industrial economic status.

Weak employment effects, and rising inequality despite a decline in poverty, must reinforce the need to re-evaluate Ghana’s growth strategy. The starting point is for policy makers to acknowledge the adverse consequences of a strong obsession with economic growth, regardless of the source of that growth and its job creation effect. Indeed, growth is a necessary condition, but it must also translate into the generation of productive and high-earning jobs for all. This requires a redirection in growth strategy, towards the promotion of manufacturing activities that are strongly linked with agriculture. Thus, fixing the problem of a missing middle and raising productivity in agriculture, should be the priority of policy for more inclusive growth. This calls for investment in areas that would promote manufacturing and agricultural activities, where the potential for job creation is high. The country could also leverage on the strong growth of the extractive sector to boost employment-friendly growth by channeling the returns from the sector into infrastructure to support the growth of agriculture and manufacturing.

For World Bank perspectives on Ghana please read the recent report on Ghana: Poverty Reduction in Ghana : Progress and Challenges. T his blog also summarises these findings.

After recovering from recession in the early 1980s, Ghana’s growth hovered around 5% but rose in the current millennium to about 7% annually. A rebase of the national accounts in 2006 pushed the country’s per capita income over the US$1,000 minimum threshold and Ghana gained entry into the league of middle income countries in 2007. The country also commenced commercial production and exports of oil in 2011, which aided growth to reach the highest levels in the country’s history. Ghana officially became one of the fastest growing economies in the world.

The country managed to achieve the key MDG goal of halving poverty ahead of the target period, with a decrease from 51.7% in 1991/92, to 24.2% in 2012/13. However, the depth of poverty remains a challenge, with a considerably high poverty gap ratio of 34.2. Moreover, income inequality continues to widen with the Gini coefficient rising from 38.1 to 42.3 over the same period.

The effect of the impressive growth of the economy on job creation has also been questioned, with the employment output elasticity declining since the 1990s (see Aryeetey and Baah-Boateng, 2015). There has been a shift in employment away from agriculture to low productivity service activities. The labor market is also dominated by low-earning self-employment in the informal sector. Indeed, employment growth in the country has largely occurred in the informal sector, reflecting an increased share of employment in the sector from 84% in 1984 to 88% in 2013. Consequently, working poverty (an outcome of a high proportion of low-paid and vulnerable employment) remains high at 22%, suggesting that at least one of every five working Ghanaians is poor.

As part of fiscal reform measures to address the country’s fiscal deficit challenge, the government undertook public sector retrenchment and privatization of State Owned Enterprises (SOEs) in the 1980s and 1990s and a freeze on new recruitment in the public sector to avoid over-bloated public sector and manage the high public sector wage bill. This has contributed to the dwindling size of public sector employment to 5.7% of total employment in 2014 compared to 10.2% in 1984. At the same time, the private formal sector is struggling in an insecure macroeconomic business environment, with an unstable exchange rate, and high interest and inflation rates, coupled with unreliable supply of power and generally weak infrastructure. It is increasingly difficult for employment in this sector to expand.

Weak job creation and widening income inequality, in the midst of a long period of strong economic growth, have also been linked to the sources of that growth. Indeed, the major driving force behind Ghana’s strong growth has been strong growth in extractives, and in the services sector. With the exception of trade (and to some extent information and communication activities), financial intermediation and extractive activities are associated with limited employment generation. As Chart 2 shows, between 2000 and 2014, the extractive sub-sector (mining and oil) of the industrial sector grew annually by 20.3% on average, and in the last eight years that growth accelerated to 34.1%. Financial intermediation also expanded by 11.7% in fifteen years, while information and communication, and trade, recorded 7.7% and 14.4% annual average growth rates, respectively.

In contrast, manufacturing and its backward linkage sector of agriculture are thought to have better job creation effects. But they have recorded weak annual growth rates of 3.8% and 4.3% respectively over 2000-2014 - dropping to 3.3% and 4.0% in the last eight years. Consequently, the contributions of these two high labor-absorbing sectors have dwindled from about half of GDP at the beginning of the millennium, to just about a quarter today. In addition, manufacturing’s share of GDP declined continuously by more than half from 10.1% to 4.9%, while the size of agriculture output also dropped by almost half from 39.4% to 21.5%. In contrast, services output expanded substantially from about a third to more than half of total national output. Similarly, the output of other subsectors of the industrial sector, which dwindled from 18.3% in 2000 to 10.6% in 2006, jumped to 21.7% in 2014 as a direct consequence of the rebase of national accounts, and faster growth of mining and oil extraction. Clearly, while some level of growth has been recorded in agriculture and manufacturing, the reality is that it has been outpaced by growth in services and extractives (mining and oil) sectors and thus reducing the share of the two sectors in GDP.

It is difficult to interpret the shift from agricultural dominance to a service led economy, within the framework of dwindling manufacturing activities, as amounting to structural economic transformation. Essentially, the path of structural economic transformation begins with a shift from the dominance of primary activities to secondary-led manufacturing activities. It ends with a high productive tertiary-led economic structure in terms of both output and employment.

However, in Ghana’s case, the path of economic transformation appears to have skipped manufacturing from primary to a rather low productive tertiary activity with adverse implication for quality of employment generation. Thus, besides the virtual collapse of manufacturing activities, increased employment in services emanates from a shift from low productive agriculture labor to informal-dominated services. Employment in manufacturing has also suffered a decline (particularly in waged manufacturing jobs) in terms of its share in total employment, while the jobs that emerged in the services sector are mostly informal, resulting in low productivity growth in the sector. The low productive service sector dominated by informal economic activities cannot effectively support the manufacturing and agriculture sectors towards the goal of high-productive industrial economic status.

Weak employment effects, and rising inequality despite a decline in poverty, must reinforce the need to re-evaluate Ghana’s growth strategy. The starting point is for policy makers to acknowledge the adverse consequences of a strong obsession with economic growth, regardless of the source of that growth and its job creation effect. Indeed, growth is a necessary condition, but it must also translate into the generation of productive and high-earning jobs for all. This requires a redirection in growth strategy, towards the promotion of manufacturing activities that are strongly linked with agriculture. Thus, fixing the problem of a missing middle and raising productivity in agriculture, should be the priority of policy for more inclusive growth. This calls for investment in areas that would promote manufacturing and agricultural activities, where the potential for job creation is high. The country could also leverage on the strong growth of the extractive sector to boost employment-friendly growth by channeling the returns from the sector into infrastructure to support the growth of agriculture and manufacturing.

For World Bank perspectives on Ghana please read the recent report on Ghana: Poverty Reduction in Ghana : Progress and Challenges. T his blog also summarises these findings.

Join the Conversation