The region’s output expanded by an estimated 4.9 percent, faster than in 2010 and just shy of the pre-crisis (average of 2003-08) level of 5 percent. Excluding South Africa, the regional growth rate was 5.9 percent. Particularly notable is the fact that this growth was widespread: over a third of countries posted 6 percent or higher growth; another 40 percent grew at between 4-6 percent. Equally important is the fact that several countries saw sustained growth rates of over 6 percent a year in both 2010 and 2011.

So what can Sub-Saharan Africa expect in 2012? Barring a serious deterioration in the global economy, the outlook for the region seems bright, with a pickup in GDP growth to 5.3 percent in 2012 and 5.6 percent in 2013. High commodity prices and strong domestic demand, especially buoyant private consumption, are expected to sustain the expansion.

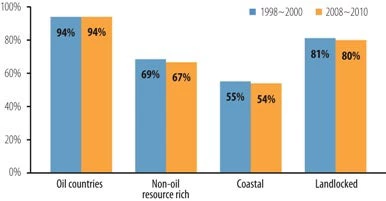

But these factors also point to Africa’s vulnerability. Most African countries are dependent on two or three primary commodities for their export revenues (see figure). Those that export consumer goods, such as Mauritius, Seychelles and Cape Verde, sell 70-90 percent to the European Union.

Median share of the largest 3 commodities in total exports in SSA by country group

Sources: COMTRADE and staff calculation based on SITC3 classification 4-digit subgroups

A sharp contraction in Europe, therefore, would pull down global demand, significantly depressing commodity prices and trade and lowering growth rates in Africa. Moreover, with many African countries entering 2012 with less fiscal and monetary policy space than in 2008-09, it will be harder for these countries to respond to global shocks as they did in the wake of the 2008 global financial crisis. Finally, parts of Africa remain susceptible to food price shocks—the Horn of Africa last year, possibly the Sahelian countries of Mali, Niger, Chad and Mauritania this year.

Join the Conversation