Now zoom forward several thousand years: saving has become central to individual and collective prosperity. As a rule of thumb those who save more become wealthier because foregoing consumption today allows one to invest in the future (e.g. you can save to buy a bicycle, a car, or a house). Businesses can invest in new equipment and governments in new roads, schools and health facilities. All of these investments are associated with better economic futures.

People and companies tend to save and invest if they can trust the institutions that manage their money and the economy at large. In the past, it was not always safe to keep deposits at banks in many African countries. It is different today. In fact some may feel more secure entrusting their savings to African banks than those in Europe (as depositors in Cyprus’ banks recently realized). But you need more than robust and credible banks for increasing savings and investments. Investors will only enter and stay in large numbers if they can trust that the state won’t change the rules of the game in mid-course.

Poorer countries save less than rich ones (just like households) because a greater share of their income goes to meeting basic needs such as shelter, clothing, and food. Richer countries also have an increasingly large group of retirees who tend to stash money aside. However, some poor countries have broken out of the cycle of low savings and high consumption, especially so in East Asia. There, high savings and investment have fueled the economic boom. China is an extreme case: more than half of what is produced is saved and then invested. But even a relatively poor country like Vietnam can boast having a savings rate of 33 percent. Some economists, including Nobel-prize winner Joseph Stiglitz, argue that, besides cultural factors, it is high growth that explains high savings in East Asia. Clearly there is a virtuous cycle between economic growth and saving.

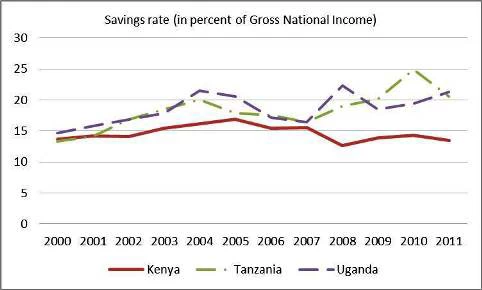

In most of Africa, savings rates are relatively low, around 17 percent of gross domestic product. Kenya is no exception and in fact it saves less than many of its peers (around 13-14 percent of GDP over the last five years). This is half of the average for all low-income countries (26 percent of GDP). By contrast, neighboring Uganda and Tanzania have already crossed the 20 percent mark (see figure) even though their per capita income is significantly lower.

Figure – Kenya’s savings rate is lagging Tanzania and Uganda

Source: World Development Indicators, World Bank

Why don’t Kenyans save more? Consumption drives Kenya’s economy and its vibrant services sector reflect this strength. The flip side is moderate growth rates and weak exports, which requires higher investment. Kenya’s economy is weak partly because infrastructure investments are still recovering from years of neglect which makes it difficult for long-term investors to position themselves despite the strengths of Kenya’s financial sector, including innovations such as M-Pesa and M-Shwari. This also means that the financial flows which enter Kenya are not necessarily transmitted into the sectors of the economy which need long-term investments, especially manufacturing.

What can be done to boost saving? Three stakeholders must be convinced to put money aside: households, companies and the government. There are at least three ways the government can act to increase savings and thereby generate more investment. First, it can strengthen property rights, especially around land titling, which will promote greater saving and investment by households in real estate. Second, it can take measures to improve the business environment and address infrastructure bottlenecks (especially energy and transport), so that business will have an incentive to save more and invest in new projects. Third, it can continue the shift in public expenditures and spend more on infrastructure than on wages, goods and services.

In sum, if Kenya wants to emulate the success of the world’s fast growing economies it needs to put money aside and borrow only if you have a strategy for generating future wealth.

------------------------------

Follow Wolfgang Fengler on Twitter @wolfgangfengler

Join the Conversation