Southern African countries had a tough 2019. The Government of Lesotho declared a national disaster as a result of the drought which left a fourth of its population facing severe food insecurity. Zambia and Zimbabwe were hit with the worst drought in nearly 40 years, which brought the roaring Victoria Falls to a trickle, and brought millions to the brink of famine. Namibia was hit with its worst drought in 90 years and declared a State of Emergency, the second one in three years, which caused a third of its population to go hungry. Botswana declared 2018/9 a drought year and commenced distribution of relief food packages in drought-stricken parts of the country. The fiscal response needed to address the drought put additional strain on these countries. By the end of 2019, several countries in the region were facing debt distress including Lesotho, Malawi, Mozambique, Zambia and Zimbabwe.

There were hopes that 2020 would be better. But with the outbreak of the COVID-19 (coronavirus) global pandemic, it quickly became clear this wasn’t to be. In March 2020, South Africa declared two back-to-back States of Disaster in an 11-day period, first for drought and then for the pandemic. Neighboring countries followed suit soon after. Responding to COVID-19 has required significant financial resources. For example, South Africa announced a R500 billion, or $30 billion (roughly 10% of GDP) relief package, Namibia announced a stimulus and relief package amounting to N$ 8.1 billion, or $544 million (4.25% of GDP), and Lesotho allocated M1.9 billion, or $113 million (about 6% of GDP), for the National COVID-19 Response Integrated Plan and emergency assistance.

The existing macro-financial risks facing the region have been exacerbated by the increasing levels of debt distress coupled with expansionary fiscal and monetary policies needed to limit the adverse effects of the COVID-19 and other shocks. This has led to downgrades in credit ratings of Botswana (by S&P Global Ratings) and South Africa (by Fitch, leaving the country without an investment-grade rating for the first time in 25 years).

The post-pandemic transition to fiscal consolidation is important to improving debt sustainability, but for the Southern Africa region, a key part of this fiscal consolidation is strengthening countries financial resilience to future shocks. According to the International Panel on Climate Change, temperatures in Southern Africa are rising at twice the global average, so climatic shocks are likely to continue increasing in both frequency and severity. These shocks are costly. The ‘The Chronology of a Disaster’ World Bank report finds that the cost of delayed response to drought could be as much as 3.9% of GDP per capita in low income countries.

Supporting countries to be better financially prepared to respond to shocks is a new yet rapidly expanding area of work for the World Bank Group in the Southern Africa region, embedded in broader crisis risk management strategies. Countries are not only embracing tools and instruments to strengthen financial resilience, but also driving innovation in the space.

For example, in 2017/2018, Zambia bundled agriculture insurance with the Government’s Farmer Input Subsidy Program (FISP). This increased the number of farmers with access to agriculture insurance from a mere 20,000 to over 900,000 within one year, making it the largest agriculture insurance program in sub-Saharan Africa. Although there are implementation challenges to this insurance program, this bold and innovative move by the government facilitated an expansion of agriculture insurance previously considered unobtainable (further discussion in the World Bank’s Zambian Agriculture Finance Diagnostic report).

Countries are also exploring the potential cost savings they can achieve through risk layering, establishing a suite of complementary risk financing instruments such as contingency funds, contingent credit and insurance. A disaster risk finance diagnostic carried out in Lesotho estimated that, through adopting such an approach, the government could save on average $4 million per year, and for an extreme shock as much as $42 million.

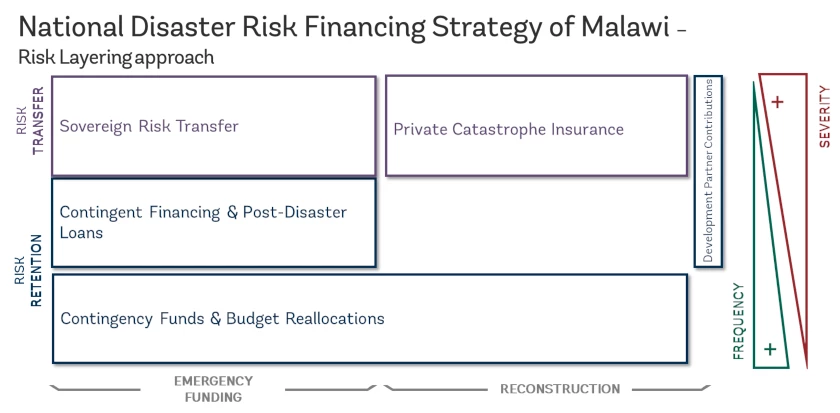

And finally, countries are increasing their preparedness by proactively developing strategies for financing future disaster response. In 2019, the Government of Malawi became the first country in Southern Africa (and second in Africa) to adopt a national disaster risk financing strategy, which identified the countries strategic priorities for financing disaster response (see Figure below).

Figure: National Disaster Risk Finance Strategy of Malawi

The COVID-19 pandemic has shown us how vulnerable households, firms, and countries are to shocks, and how unprepared many countries were. Without a vaccine, we don’t know how long the pandemic will last, but the prospect of finding an effective vaccine is likely. In contrast, analysis carried out by the World Bank shows that the risk of climatic shocks remains. Eswatini, Lesotho, South Africa and Zambia, among other countries in the Southern Africa region, have taken the first steps on increasing their financial preparedness to respond to shocks, by developing a customized suite of risk financing instruments, protecting the budget and GDP, and most importantly, the poor and vulnerable. Improving financial preparedness is the first step to strengthening financial resilience – and 2020 has shown has just how important that is.

Join the Conversation