The recently-published Regional Economic Outlook for Sub-Saharan Africa (SSA) by the International Monetary Fund underscores the enduring view of international financial institutions that the depth, pace and perfecting of structural reforms needs to continue, not only for competitiveness and growth but also for resilience should external headwinds emerge. The report also presents an important opportunity to further develop this agenda, by the additional treatment of the underlying causes, particularly non-price based ones, and thereby generate a more actionable view of the growth, competitiveness and equality trends so incisively presented in the report.

Growth

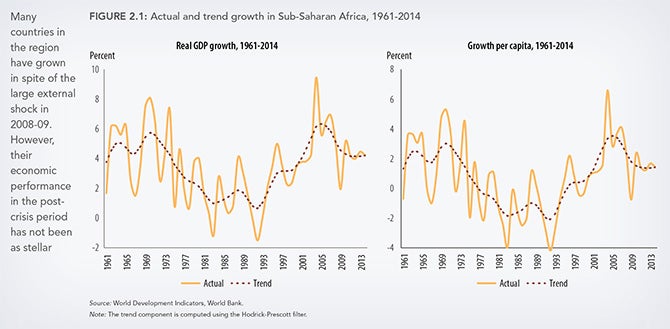

The report shows that many of the resource based countries in SSA, where commodity export revenues account for a greater share of fiscal revenue, have been rendered more vulnerable (irrespective of their currency regimes) to the fall in commodity prices and the global slowdown. Growth in these countries is expected to slow significantly in the coming years. In many of the non-resource dependent and low-income countries, in spite of the global slowdown, growth on average is expected to continue uninterrupted. By mentioning some of the structural reforms in connection with the growth analysis, the report sets the stage for drawing out the role of these reforms more rigorously in accounting for the differences in outlook and resilience between these different groups of countries.

The report’s comprehensive treatment of outputs and outcomes derived from indicators and rankings provides the basis to go one step further to causally link these to the underlying inputs and policy efforts. If data limitations are overcome, it will allow a deeper examination of the causal linkages by incorporating in the analyses, the structural reforms that had taken place, and thereby render these findings more prescriptive and actionable in terms of what policy makers have done or should be doing in order to generate growth and build resilience.

Competitiveness

In the chapter on competitiveness, the comprehensive analyses of real effective exchange rates does not detract from or understate the importance of structural reforms, but recognizes that they constitute many of the other (and often unmeasured) factors that go towards creating the terms of trade differences between countries. For example, in the case of South Africa, the report very incisively points out that the advantages created by shifts in real effective exchange rates have not generated the expected export response. The main reason given for this were structural constraints presumably attributable to lagging reforms. This raises a very key development question, namely if policy priority should focus, and scarce resources be deployed, on depreciating the real effective exchange rates or on achieving first, the structural reforms that are needed. This example could in fact, be the tip of the iceberg of unfinished reforms, hiding in the data already reviewed, and now made visible by this report for further analysis from the perspective of structural reforms and their effects on the competitiveness of a country.

While the paper relies primarily on price level or price index-based indicators of competitiveness, it also opens the door to more fully capture the impact that non price-based indicators (These include “institutions, policies and factors that determine productivity in a country” Table 2.1 and pages 41 and 42) may have had on these differences, in growth and resilience between the countries analyzed. While the objective of the report may have been to mainly track the trends, it also provides the intellectual bridge to the larger story. The need to better understand the reasons for the difference in the post slump performances between the resource-rich and non-resource-rich and low income countries, in addition to what is explained by the data, will prompt the necessary additional research in order to answer questions such as: why are the non-resource-rich countries and the low income countries in particular, continuing to grow? Did they become more competitive during the growth spell or is it just because they have been less impacted by the global slowdown because of lack of export revenues?

The report raises the possibility that the terms of trade in non-resource sectors may have remained at a greater disadvantage in the resource rich countries vis-à-vis trading partners, than in non-resource dependent countries (both middle and low income) due to a possible lack of reform effort in the former. For the latter, in the absence of the commodity export engine, bootstrapping growth through structural reforms may have been the only feasible option at the time, which subsequently enabled this group to weather the later emergence of global economic headwinds. The findings of the report legitimizes and strengthens these previous, and sometimes conjectural, hypotheses, and provides the rationale and justification to more seriously explore if the data can support and verify these more prescriptive and useful explanations.

Equality

The report suggests that the commodity exporters continue to experience greater economic inequality. As a result they might not be getting the potential 0.7-1.5% uptick in growth, projected for the non-resource based and low income countries that have achieved greater equality. Economic equality is driven by many factors and often requires deliberate reform efforts by Government. The apparent differences in equality between the resource and non-resource based countries found by the report also provides the rationale for a further look into the data, and particularly, into the extent to which non-price indicators might have captured the equality related policy reforms and other efforts, made by government in these country groupings.

Conclusion

A key lesson for policy makers is actually embedded in the report suggesting that Government should focus not only on improving price related indicators of competitiveness but also non-price indicators. The additional work mentioned above, once done, will have made the report and the results of any follow up work, together, more actionable and thus useful for policy-makers. The slowing growth in the resource rich countries and the resilience demonstrated by the non-resource dependent group of countries, upon completing the additional analyses, could very likely substantiate the rationale and guidance that Structural Reforms are not something that a country needs to do when times are bad, but rather they are something that a country needs to do, when times are also good, and on a continuing basis in order to remain competitive.

Join the Conversation