While there is a consensus among researchers and policy makers that the 2008–2009 crisis was triggered by financial market disruptions in the United States, there is little agreement on whether the transmission of the crisis and the subsequent prolonged recession were caused by credit factors or a collapse of demand for goods and services. On the one hand, a credit crunch, defined as a reduction in the ability of firms to get loans or a sudden tightening of the conditions required to obtain a bank loan, squeezes firms’ working capital and hurts their production. On the other hand, adverse demand shocks to firms come from declines in demand for firms’ products and services. Each type of factor has fundamentally different policy implications. If credit factors are found to play the main role, the solution would be to provide more and cheaper credit. But if demand factors are the main drivers, the focus should be on boosting investors’ and consumers’ confidence. Interestingly, most of the effort to understand the impact of the crisis focuses on credit and not on demand.

In our new research, we find that demand collapse, not credit factors, was hurting firms the most in the crisis. Based on data from the Financial Crisis Survey, which was conducted by the World Bank, on firms in six Eastern European countries, we show that the drop in demand for firms’ products and services is very severe and is reported as the most damaging factor on firms in these countries. Other "usual suspects," such as rising debt or reduced access to credit, are reported as minor.

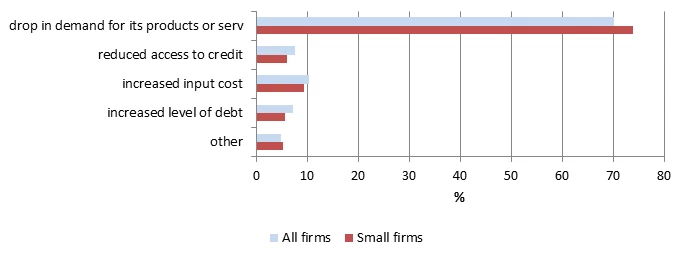

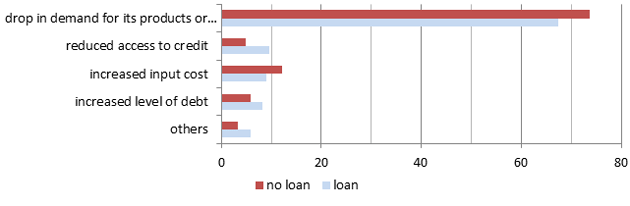

The data show that the demand factor is reported as the number-one cause for firms’ declining performance. Among the 1,478 firms that responded, 69 percent pointed to the drop in demand for their products and services as the main effect. Increase in the level of debt, increase in input cost, and reduced access to credit each account for about 7–10 percent of firms. The percentages are similar between small firms and larger firms. Furthermore, even for firms that have some ongoing credit relationship with lenders, demand is still the most important factor. For instance, among 857 firms that had loans in 2007, 67 percent pointed to demand as the main factor for their poor performance in 2009, which was only slightly less than the percentage for those that did not have loans.

Figure 1: Main effects of the crisis, by firm size

Figure 2: Main effects of the crisis, by credit status

One might argue that a decline in demand for firms’ goods and services can still be a credit problem because the decline in firms’ demand is due to consumers’ reduced access to credit. We cannot rule out this possibility. Nevertheless, even if consumers face credit crunches and cut back on consumption, from the firms’ perspective, it is a demand shock. Examining whether consumers actually face credit crunches is an interesting question in itself, but answering it would require household data. In fact, studies on firms in general will not be able to say much about consumers’ credit situations.

We provide econometric evidence regarding the impact of demand and credit sensitivities on the performance and operation of firms during the crisis. The main indicators for firms’ performance and operation are firms’ sales, employment, and capacity at the beginning of the crisis. We find that the change in firm sales and the change in capacity are significantly and negatively correlated with the demand sensitivity of the sector in which the firms operate; this is robust across specifications. However, these indicators are not robustly correlated with various proxies for firms’ credit needs. The results imply that the association between firms’ performance and their sectors’ demand sensitivity is strong.

Join the Conversation