Illustration of money transfer through mobile devices | © shutterstock.com

Illustration of money transfer through mobile devices | © shutterstock.com

In many emerging economies, local governments depend largely on transfers from the central government to meet a growing demand for public services and infrastructure and to cope with adverse events. Access to credit markets could alleviate their financial constraints. However, their borrowing capacity is limited by fiscal rules and financial sector regulations that seek to prevent overborrowing. In this context, it is uncertain to which extent subnational governments use debt to smooth income fluctuations intertemporally.

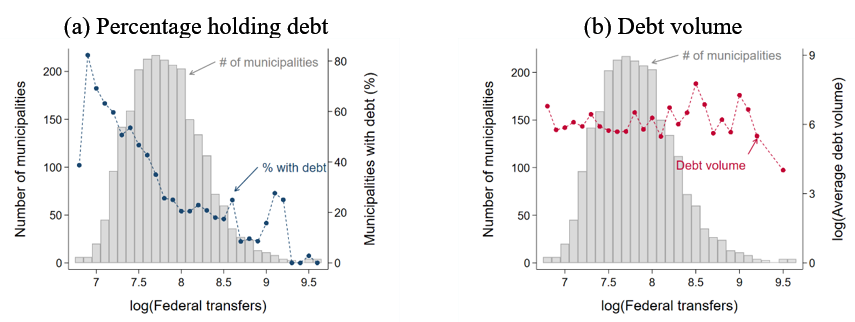

In a new paper, I study how a shock to federal transfers affects municipal debt in Mexico. Such a shock will have different effects on the demand and supply of credit. On the demand side, a negative effect will arise if there is a substitution between grants and debt. This is expected from governments that are not borrowing constrained. On the supply side, there should be a positive effect given that present and future grants can be used to collateralize debt. This effect is expected among the more collateral constrained governments. It could raise concerns if more transfers soften budget constraints and this leads to overborrowing (see, e.g., Velasco 2000; Rodden 2002). Figure 1, panel a, shows that the fraction of indebted municipalities decreases with the per capita level of federal transfers, which is suggestive of a substitution between the two. Conditional on being indebted, panel b shows no clear relationship between the per capita levels of municipal debt and transfers.

Figure 1: Municipal debt with financial institutions by level of federal transfers

Note: The horizontal axis shows 0.1-logarithmic-unit bins of the average federal transfers. The gray bars (left axes) show the number of municipalities in each bin. The dots (right axes) represent the average fraction of municipalities holding debt (panel a) and the logarithm of the average volume of debt (panel b). Values are in December 2010 Mexican pesos and are normalized by population. The data cover from August 2009 to December 2016 and are extracted from the R04 C commercial credit report (National Banking and Securities Commission).

Since the determinants of local revenue and financing needs could be correlated, I adopt an empirical strategy like that in Gordon (2004) to provide causal evidence. States allocate federal grants to municipal governments using distribution formulae that generally depend on population. Following the release of census data, municipalities with a higher intercensal population growth within a state start receiving a higher share of federal revenues. This update in the distribution coefficients is a function of long-term, discrete changes in the official population data. Importantly, it is imperfectly correlated with the determinants of local financing needs in the short term, which should change continuously with current changes in population. Hence, the revenue shock is given by the growth in population between the 2010 census and the 2005 intercensal count. The goal is to compare the post-census outcomes of municipalities that, within a state, experienced high and low population growth in the past quinquennium.

First, I confirm that the census shock leads to a persistent increase in federal transfers to municipalities with higher population growth relative to those experiencing lower growth. Following a 10% increase in population between 2005 and 2010, transfers increase by 3% more over 2011–2012 relative to 2010 and this is a long-lasting effect. Since the census shock has no effect on other sources of municipal revenue, such as state transfers or taxes, federal transfers are the main channel mediating the debt response. For the analysis on municipal debt, I look at its monthly stock per bank (bond issuances are rare), aggregated from loan-level supervisory data. I find that a 10% population shock reduces the probability of having debt by 0.2 p.p. (2.3% of municipality–bank pairs have credit relationships). This negative effect is temporary, lasting for two years at most. Conditional on being indebted, the shock has no effect on debt volume.

In addition, I examine the role of local governments' creditworthiness in the debt response. Insufficient own revenues and volatile and unpredictable intergovernmental transfers erode creditworthiness (Hanniman 2000). Thus, I use a high ratio of transfers to own-source revenue as a proxy for low creditworthiness. I find that the shock effect on the probability of being indebted is stronger for the governments that were less transfer dependent before the shock. For governments with lower financial autonomy, the shock does not affect their probability of being indebted. It has some positive effect on loan volume, consistent with a loosening of collateral constraints, but it is generally insignificant to raise concerns about overborrowing.

Political factors could also affect the response to the shock, especially in this setting in which a federally-owned development bank is the main lender. However, I find no differential effects of the shock on the probability of being indebted when the lender is public, not even in the proximity of local elections or when the municipal mayor is aligned with the presidential party.

Finally, to complete the understanding of the impact of the shock on municipal budgets, I look at municipal expenditures. For a 10% increase in population, primary expenditures increase by 2%. Even though the increase in grants is permanent, what increases is short-term, current spending rather than investment in capital goods. This could reflect either myopic spending decisions or that the shock is not perceived as permanent given the volatile nature of grants.

Conclusion

For local governments in an emerging country, this study shows that only the few with more tax collection capacity can substitute federal transfers for bank debt. Since they are deemed more creditworthy, they can access credit markets when grants are low and, therefore, are also able to reduce debt during good times. One implication for decentralization policy is that diversifying the revenue base of local governments will enhance their access to credit markets and, hence, their ability to smooth income shocks. For the more transfer-dependent governments, the inability to become indebted reinforces such dependency and reduces their financial autonomy even further. The results do not provide evidence of higher transfers leading to excessive indebtedness. This is documented for a period prior to the strengthening of the prudential rules for subnational financing. However, financial sector regulations for subnational lending were already operating under a no-bailout commitment of the central government. This suggests that a market-based borrowing framework has the potential to ensure financial discipline.

Join the Conversation