The Global Financial Crisis of 2007 to 2009 has spurred renewed widespread debates on the “bright” and “dark” sides of financial innovation. The traditional innovation-growth view posits that financial innovations help reduce agency costs, facilitate risk sharing, complete the market, and ultimately improve allocative efficiency and economic growth. The innovation-fragility view, by contrast, has identified financial innovations as the root cause of the recent Global Financial Crisis, by leading to an unprecedented credit expansion fueling a boom-bust cycle in housing prices, by engineering securities perceived to be safe but exposed to neglected risks, and by helping banks and investment banks design structured products to exploit investors’ misunderstandings of financial markets and exploit regulatory arbitrage possibilities. Paul Volcker, former chairman of the Federal Reserve, claims that he can find very little evidence that the financial innovations in recent years have done anything to boost the economy.

There is an extensive descriptive literature that discusses financial innovation, but a relative dearth of empirical studies that are based on quantitative analysis. In joint research with Tao Chen, Chen Lin, and Frank Song, I gauge these two opposing hypotheses on the effects of financial innovation, by using a new cross-country indicator of financial innovation and relating it to real and financial sector outcomes. Specifically, we gauge the relationship between financial innovation and economic growth and volatility, as well as between financial innovation and banks’ risk taking and fragility.

Measuring financial innovation

Cross-country data on financial innovation are scarce due to the absence of patent data in the financial sector. R&D expenditures are typically not collected for financial institutions nor are data on research staff. This lack of data, as already pointed out by Frame and White (2004), has impeded the rigorous study of financial innovation across countries.

We fill this gap by collecting data on R&D expenditure in the financial intermediation industry from the Analytical Business Enterprise Research and Development database (ANBERD) of the OECD. Most R&D data are derived from retrospective surveys of the units actually carrying out or “performing” R&D projects, and collected from enterprise surveys via the OECD/Eurostat International Survey of Resources Devoted to R&D from 32, mostly high-income, nations in the world from 1987 to 2006. As our main indicator, we use financial R&D intensity relative to the value added in the financial intermediation sector, but confirm our finding by standardizing financial R&D with total operating cost of banks.

Our indicator of financial innovation is certainly subject to measurement error, though we can show that it is correlated to specific dimensions of financial innovation, including the importance of off-sheet balance sheet items, the prominence of syndicated credit facilities and the use of CDS. Financial innovation across countries is also significantly correlated with innovation in manufacturing, as measured by the same survey instrument (which in turn is highly correlated with patent filings). In a placebo test, however, we show that innovation in manufacturing cannot explain our findings, i.e., our findings cannot be explained by a general innovative attitude in an economy. It is important to note that our indicator of financial innovation is focused on the process rather than on specific outputs of financial innovation, which can take many forms, such as new securities or products, new screening, monitoring and risk management tools or new types of institutions and markets.

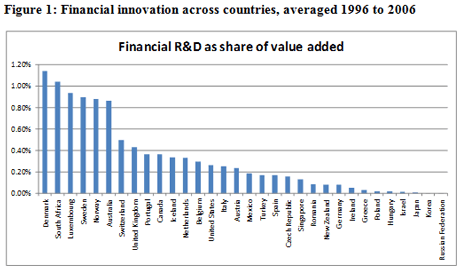

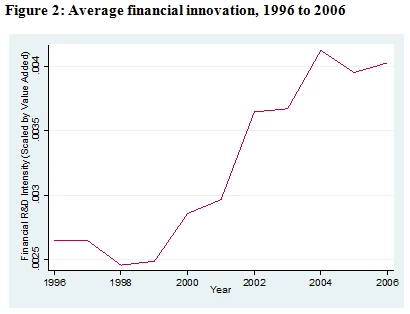

Looking at financial innovation across countries, we note that it is rather small, with the mean value of Financial R&D Intensity being 0.33% of value added. This is in line with an average R&D intensity of 0.428% in the service industry, but much smaller than an average of 2.113% in manufacturing. There is wide variation in financial innovation across countries, ranging from high levels in Denmark and South Africa to almost zero in Russia (Figure 1). There is an increasing trend in financial innovation over time across our sample countries, almost doubling between 1996 and 2006, consistent with anecdotal evidence on increasing innovative activity within the banking system during this period (Figure 2).

The effects of financial innovation

When relating our cross-country indicator of financial innovation to an array of real and financial sector outcomes, we obtain evidence for both the bright and dark sides of financial innovation:

- Countries where financial institutions spend more on financial innovation are better able to translate growth opportunities into GDP per capita growth.

- Industries that rely more on external finance and more on R&D activity grow faster in countries where financial institutions spend more on financial innovation.

- However, industries that rely more on external finance and more on R&D activity also experience more volatile growth in countries where financial institutions spend more on financial innovation.

- In countries where banks spend more on financial innovation, banks are also more fragile. This relationship is especially strong for banks with smaller market shares, banks with faster asset growth and banks with higher shares of non-traditional intermediation activities. This higher fragility is due to higher profit volatility of banks in countries with higher levels of financial innovation.

- In countries where banks spent more on financial innovation before the crisis, they suffered greater reductions in their profits, relative to both total assets and equity.

These findings hold controlling for a large array of other country characteristics, including a traditional measure of financial depth, Private Credit to GDP. Together, these results provide evidence for both the innovation-growth and innovation-fragility hypotheses.

What do we learn from these findings?

Our results are the first cross-country evidence on the effects of financial innovation. Our findings, however, also shed light on the recent discussion on non-linearity in the finance-growth relationship that has highlighted declining, insignificant or even negative associations of finance with economic growth at high levels of GDP per capita (Aghion et al., 2005, Arcand et al., 2012). Our finding that financial innovation is associated with higher levels of economic growth, even when controlling for aggregate indicators of financial development, in our sample of high-income countries, suggests that it is not so much the level of financial development, but rather the innovative activity of financial intermediaries, which helps countries grow faster at high levels of income. Our results, however, point again to the double-sided nature of financial deepening, bringing opportunities but containing risks, which calls for appropriate regulatory policies.

On a closing note, it is important to stress that our research refers to a sample of high-income and upper middle-income countries. Financial innovation has played a very important role in many low and lower middle-income countries, as also discussed on this blog, such as rainfall insurance or mobile banking.

References

Aghion, Philippe, Peter Howitt, and David Mayer-Foulkes. 2005. The Effect of Financial Development on Convergence: Theory and Evidence. Quarterly Journal of Economics 120, 173-222.

Arcand, Jean Louis, Enrico Berkes, and Ugo Panizza. 2012. Too Much Finance? IMF Working Paper12/161.

Beck, Tao Chen, Chen Lin, and Frank M. Song. 2012. Financial Innovation: The Bright and the Dark Sides. HKIMR Working Paper 05/2012.

Frame, W. Scott, and Lawrence J. White. 2004. Empirical Studies of Financial Innovation: Lots of Talk, Little Action? Journal of Economic Literature 42, 116-44.

Join the Conversation