A chess board depicting shadow banking concept | © shutterstock.com

A chess board depicting shadow banking concept | © shutterstock.com

Shadow banks — non-depository lenders — have disrupted every aspect of traditional banking activity from lending to payments. In the $10 trillion U.S. residential mortgage market, for example, shadow banks have been originating more than half of the total new loans every year since 2017, and six of the largest 10 mortgage lenders were shadow banks (Buchak et al. 2018). Despite their central role in evaluating regulations and policies, the evidence on how these intermediaries are funded is rather limited (Jiang et al. 2020).

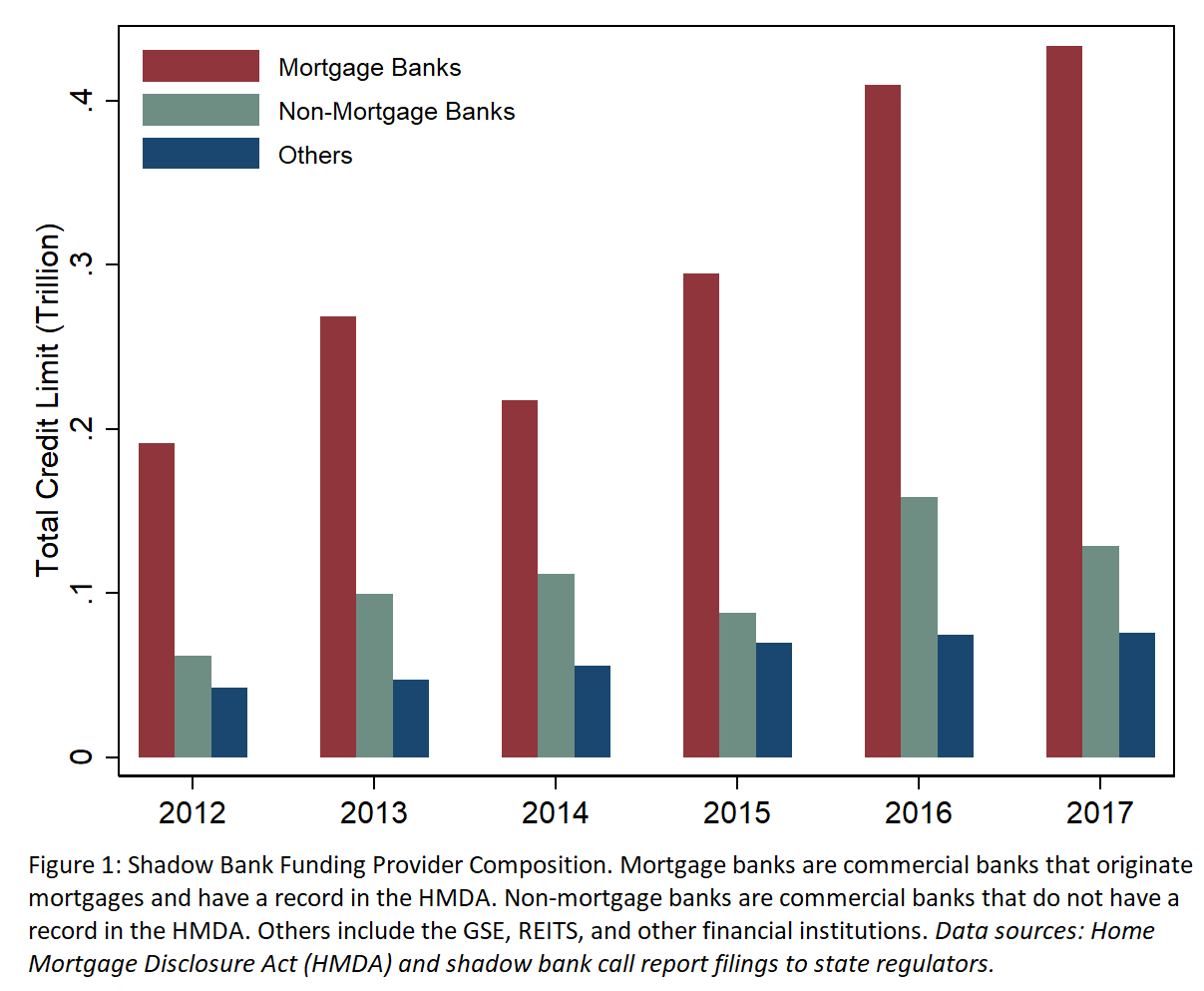

In my recent working paper, I use new data on shadow banks’ funding to document a key distinguishing feature of their funding sources: shadow banks are funded by the very banks they compete with in originating mortgages. Banks with in-house mortgage origination supplied about 70% of total warehouse credit lines — a form of short-term debt — received by shadow banks from 2011 to 2017 (figure 1). In 2017, about a trillion dollars were flowing through these warehouse lines that have total credit limits of $570 billion. These persistent warehouse funding relationships are clustered between the banks and the shadow banks that originate mortgages in the same geographic regions and thus compete for the same local mortgage borrowers. I then study how this upstream funding relationship between banks and shadow banks affects competition in the downstream mortgage origination market.

There are two countervailing forces in banks' decisions to extend funding to a shadow bank when banks have upstream market power. Both forces lessen the competition in the downstream market. On the one hand, lending to shadow banks lowers a bank’s profits in the downstream market. This cannibalization channel induces banks to decrease upstream lending to shadow banks, reducing competition in the downstream market. On the other hand, market power in the upstream market allows the bank to partially capture shadow banks’ mortgage lending profits. Through this funding channel, banks have stakes in the shadow banks and thus internalize the cost of competition in the downstream market.

Empirical evidence suggests that banks have market power in the upstream warehouse lending market. I show that these relationships are costly to substitute by exploiting a sharp, unanticipated oil price decline. This decline resulted in differential net worth shocks to banks based on their balance sheet exposure to the oil and gas industry. Following the shock, exposed shadow banks' cost of funding increased relative to that of other shadow banks, suggesting that replacing the relationship is costly. The shock propagates into shadow banks’ mortgage origination in the downstream market. Exposed shadow banks raised their mortgage interest rates in the downstream market and originated fewer mortgage loans than other shadow banks in the same county at the same point in time. The results imply that banks’ market power in the upstream funding market spills over to the downstream mortgage market.

Consistent with the cannibalization channel, a bank is less likely to lend to shadow banks in counties where its own mortgage origination market shares are high. These are markets in which the cannibalization effect would be most severe. Consistent with the funding channel, a bank that funds more shadow banks in a county charges higher rates in the downstream market, suggesting that it does not compete too severely with shadow banks, and instead appropriates the rents in the upstream market.

I then build a quantitative model and show that banks’ upstream market power softens competition in the downstream mortgage origination market, lowering consumer surplus by $14 billion in an average metropolitan statistical area (MSA). This effect is almost double in MSAs with one standard deviation higher downstream mortgage market concentration. Thus, the costs of banks’ warehouse lending market power are largely borne by households in the least competitive downstream mortgage market who are already suffering from restricted access to credit. It would seem that the added competition from shadow banks would help these borrowers most. Yet, shadow banks' expansion is limited in these areas due to banks' market power in the upstream warehouse lending market.

Policy Implications. If shadow banks can sell loans quickly, warehouse costs become small relative to overall funding costs, and banks cannot undo this change by simply charging more. The model counterfactual shows that improvements in the secondary markets, specifically in the speed of government-sponsored enterprise loan purchase programs following mortgage origination, would spill into the downstream mortgage market.

Moreover, given the large role of shadow banks in mortgage origination, disruptions in their funding and its potential spillovers to lending have been concerning regulators; these concerns have increased in prominence during the ongoing COVID-19 pandemic. Another model counterfactual shows that in an economy with a reduced number of banks supplying warehouse funding to shadow banks, shadow banks make up some of the shortfalls by pivoting to alternative sources, while banks do not completely offset the shock to consumers. Mortgage rates increase and lending declines, suggesting a large negative consequence borne by mortgage borrowers as banks withdraw from the warehouse lending market, even if they continue providing mortgages. The analysis supports the idea that disruptions in shadow banks’ funding can have important consequences and should be given appropriate attention by regulators.

Overall, the findings shed light on the benefits and limits of the growth of nonbank financial intermediaries. Banks' market power in the upstream funding market allows them to keep their rents in the least competitive downstream consumer credit market, limiting the benefit of the growth of nonbank financial intermediaries passed onto consumers. The paper thus uncovers a new channel through which regulatory interventions and technological developments improve consumers' access to credit by reducing such funding reliance between financial intermediaries.

Erica Jiang is an Assistant Professor at USC Marshall. More details about her research can be found on her website.

References

Buchak, G., Matvos, G., Piskorski, T., & Seru, A. (2018). Fintech, regulatory arbitrage, and the rise of shadow banks. Journal of Financial Economics, 130(3), 453–483.

Jiang, E., Matvos, G., Piskorski, T., & Seru, A. (2020). Banking without deposits: Evidence from shadow bank call reports (No. w26903). National Bureau of Economic Research.

Join the Conversation