The Middle East and North Africa (MENA) region is home to about 70 million of the world’s poor (living on less than two dollars per day) and 20 million of the world’s extremely poor (living on less than US$1.25 per day). According to a recent Gallup survey, 95 percent of the adults residing in MENA define themselves as religiously observant. The combination of these two facts has produced a growing interest in Islamic finance as a possible tool for reducing poverty through financial inclusion among the region’s religiously conscious Muslim population (see Mohieldin et al. 2011).

Uneven access to financial services and instruments that are compliant with Shari’ah, or Islamic law, could be one of the contributing reasons for the low number of bank accounts in the MENA region. A mere 18 percent of adults (above the age of 15) have accounts in formal financial institutions, the lowest in the world (Figure 1). There is ample evidence that, if done correctly, increasing access to and the use of various financial services can help both reduce poverty and its severity (for example see Burgess and Pande 2005 and Beck, Demirgüç-Kunt and Levine 2007 among many). With no access to financial services, many of the poor in MENA will continue to be trapped in poverty with little to no chance of escaping it in the foreseeable future.

Source: The Global Financial Inclusion Database (the Global Findex)

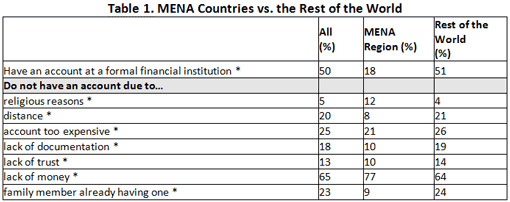

The main issue here is that many Muslim-headed households and micro, small, and medium enterprises (MSMEs) may voluntarily exclude themselves from formal financial markets because of religious requirements. The Islamic legal system has guidelines and regulations pertaining to the financial transactions of Muslim believers. One such tenet is the prohibition of pre-defined interest-bearing loans and other financial services. Another important tenet is "loss-sharing profit-sharing" which requires financial providers to share in the losses (and profits) of the business activities for which they provide financial services. The majority of conventional financial services do not meet these two main requirements, and are therefore not relevant to religiously minded Muslim individuals and firms in need of financing in the MENA region and other parts of the world. While roughly four percent of respondents without a formal bank account in non-MENA countries cite religious reasons for their lack of an account, this figure is about 12 percent for the MENA region (Table 1).

Source: Calculations based on the Global Financial Inclusion Database (the Global Findex).

*: The means t-test between the MENA and Non-MENA countries is significant at less than 1% level.

MENA countries, however, are far from uniform in terms of religiously motivated financial exclusion. For example, while 27 percent of adults in Tunisia and Morocco point to religious reason for not having an account at a formal financial institution, only three percent of respondents in Kuwait and UAE offer similar reasons (Table 2). To some degree, this could be traced back to the level at which Islamic financial institutions (IFIs) are present in a given country. While IFIs are practically absent in Tunisia and Morocco, they enjoy a widespread presence in many Persian Gulf economies, providing ample Shari’ah compliant financial alternatives for the religiously-minded population of these countries (Table 2).

Islamic microfinance instruments (such as Qard-Hassan and Murabaha) could be particularly attractive tools for reaching and providing vital credit to the region’s poor, who represent about 17 percent of the total population of the various MENA countries. Global surveys conducted by the Consultative Group to Assist the Poor (CGAP) in 2007 and 2012 provide some initial insights into the rapidly growing Islamic microfinance industry. Based on the 2007 CGAP survey, it was estimated that less than 130 Islamic microfinance institutions were serving 500,000 customers (CGAP 2008). In five years, these figures have more than doubled. By 2012, there were 256 Islamic microfinance institutions with 1.3 million active clients (CGAP 2013).

Apart from its strategic value in bringing the poorer segments of the population into the financial fold, the signs point to even more growth for an industry that could play an important role for the region as a whole. According to the 2011 Global Findex, more than 19 million adults in MENA avoided interactions with formal financial institutions for religious reasons. The presence of this relatively large population that has opted out of currently available financial services provides a great business opportunity for IFIs. However, several obstacles have hindered the growth of this industry, the most important of which has been the lack of transparency and the absence of a broadly accepted standardized process for assessing the compliancy of financial institutions with Shari’ah guidelines. This has made it difficult for many individuals to distinguish between financial institutions that are genuinely operating based on Shari’ah specifications and those institutions that are not. Another main difficulty has been the lack of available information and training on Islamic finance. For example, only about 48 percent of adults in Algeria, Egypt, Morocco, Tunisia, and Yemen have heard about Islamic banks (Demirguc-Kunt, Klapper, and Randall 2013). Finally and partly because of the lack of a standardized process, information and training, it is usually the case that Islamic financial products are more expensive than their conventional counterparts, reducing their competitiveness among faithful Muslims despite their clear religious appeal.

The World Bank is well-positioned to initiate and lead the efforts in addressing these and many other challenges hindering the growth and efficiency of the Islamic Banking and Finance Industry. With the signing of Memorandum of Understandings with the Islamic Development Bank (IDB) and the International Centre for Education in Islamic Finance (INCEIF), the Bank has established formal relations with two of the world’s leading institutions in Islamic Finance. This is in addition to increasing collaboration with various central banks and stock exchanges of the Persian Gulf countries, Turkey, and Malaysia. The Bank will be able to act as a key conduit for knowledge and expertise in Islamic finance and, backed by its decades-long history in development, will be able to assist in the design of relevant Islamic financial services and instruments that will have the greatest impact on poverty.

Source: Author’s calculation based on Islamic Development Bank, BankScope, Gallup Survey 2010, and World Development Indicators 2012.

Note: The “religiosity index” captures the percentage of adults in a given country who responded affirmatively to the question "is religion an important part of your daily life?" in a 2010 Gallup survey.

(Author’s Note: This work is part of the analysis for the forthcoming 2014 Global Financial Development Report on Financial Inclusion, which covers this topic and other related subjects in more details.)

Join the Conversation