Vendor displaying different QR code based payments at local cloth shop | © shutterstock.com

Vendor displaying different QR code based payments at local cloth shop | © shutterstock.com

Technology-based payment service providers—payment fintechs—have disrupted payment market transformationally and are entering the credit market . PayPal and Square are the most prominent examples of such payment fintechs, but others are active in the lending markets all over the world. Tyro payments in Australia has been operating with a full banking license since 2016. Among developing countries, other than the BigTechs in China, the payment fintechs offering credit are Paytm, Mswipe, and Pine Labs in India; KopoKopo in Kenya, which lends to merchants accepting payments through Lipa na M-Pesa; and iKhokha in South Africa. Many of these fintechs offer credit to merchants who use the fintech's point-of-sales (PoS) device for electronic payments.

An often-heard argument for why payment fintechs have entered the lending business is that they are digital adept, and that they possess the information on the (digital) sales of the merchants. A merchant’s digital payment footprints allow the payment fintech to assess the creditworthiness of the merchant. Less attention is paid to the argument that payment fintechs have direct access to the borrowing merchant’s cash flow when processing transactions. This gives them ultimate seniority compared with all other creditors as they can enforce loan repayment before the merchant can spend the sales revenue elsewhere.

Many credit products of payment fintechs (including those of PayPal and Square) are designed such that the lending fintech automatically deducts a proportion of each transaction it processes for the borrowing merchant. That is, from each transaction processed through the fintech's PoS device, the fintech keeps a proportion that goes toward loan repayment, while the borrowing merchant receives only the remaining amount. This “enforcement technology” not only brings benefits to the lender, it may also enable credit-constrained micro, small, and medium-size enterprises (MSMEs) to access credit. Many MSMEs are excluded from the credit market not only because of lack of financial information, but also often because of the high debt enforcement costs, which—in relation to the small credit volume—are unattractively high. A further potential benefit of payment fintech lending stems from their ability to offer flexible-repayment loans to MSMEs by making repayment sales-linked, as described above. The flexibility could be valuable to MSMEs that face volatile sales. With flexible repayments, MSMEs can share some risk with the lender by paying less in periods with lower sales and making up for it in periods of higher sales.

We are collaborating with one of India's largest payment fintechs to understand these three potential benefits of this innovative form of lending. In a recent paper, we analyze the effectiveness of the second advantage—payment fintech’s seniority from its payment processing activity. The payment fintech mostly serves micro and small businesses, many of which have low credit scores, or no credit history at all (10% of loans). During the analysed period between October 2017 and November 2018, the fintech issued loans with 2% interest per month and an average volume of INR ~38,000 (USD ~550 at PPP) per loan. On average, borrowing merchants typically transacted about INR 4,000 per day. The average time taken until full loan repayment was about 4 months. Of the loans issued by the fintech, about 31% were nonperforming (defaulted or more than 30 days past due date implied by the merchant’s sales volume before loan disbursal), of which 12% actually defaulted.

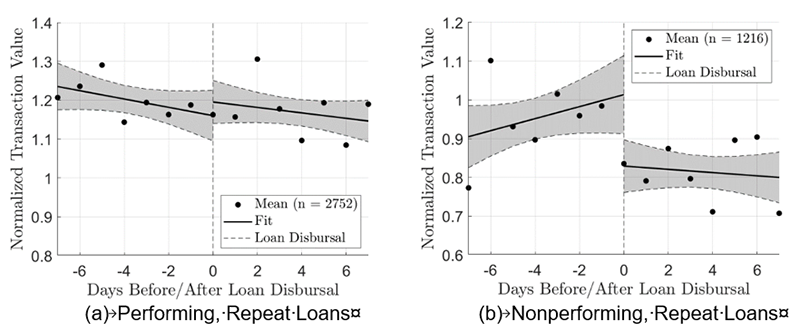

An interesting observation is that most nonperforming merchants significantly and discontinuously reduce their transactions via the lender fintech's PoS immediately on the day after credit disbursal. In particular, we observe the phenomenon for nonperforming merchants who had already borrowed from the fintech before (nonperforming, repeat loans). The discontinuous drop in sales among nonperforming borrowers indicates an intentional element in default. Figure 1 shows the average daily total transaction volume of borrowing merchants, before and after disbursal of their repeat loan. Each merchant’s transaction volume is normalized by the merchant's pre-disbursal long-term average total daily volume (=1). The figure shows that the sales of the nonperforming repeat borrowers are discontinuously reduced to only 83% of the long-term pre-disbursal average on exactly the day of loan disbursal. The reduction corresponds to 17.8% compared with what the sales should have been on the day of disbursal absent any change. This discontinuous pattern is not prevalent among performing loans or first loans of repeat borrowers, with the latter result pointing toward learning effects.

Figure 1 Average of Merchants' Daily Sales Pre- and Post-Loan Disbursal

The fact that this reduction in sales occurs (i) immediately on the day of borrowing and (ii) is measurable as a significant discontinuity indicates that the loan default is intentional. If the loans were nonperforming due to exogenous income shocks, we would expect the days when these shocks hit not to be concentrated at any particular day after disbursal. Rather, we would expect the days of the shocks to be smoothly distributed around disbursal and across affected merchants. Hence, it would be unlikely to observe a discontinuity on any particular day. Since neither the shock nor the day of disbursal is perfectly predictable, we can also rule out the explanation that the discontinuity on the disbursal day is because merchants perfectly synchronize the loan disbursal with the date when they expect a sales shock. Moreover, since we pool in our analysis different loans from different districts, industries, and disbursal dates, we can also rule out that the discontinuity would be due to macroeconomic shocks.

Our study shows that the enforcement technology is not able to prevent intentional defaults completely. Our explanation for this is the fact that merchants can bypass the automatic loan repayment by diverting sales from the fintech's PoS to alternative means of payment, especially cash. This is of course only possible if they have the power to convince their customers not to pay by card (or digitally) but in cash. An indication that merchants are indeed diverting sales to cash is provided by an episode in the spring of 2018, when a cash crunch occurred in some Indian districts. Because of the cash shortage, it would be more difficult for the merchants to persuade their customers to pay in cash in the affected districts during the cash crunch. Consistent with this explanation, we do not find discontinuity in sales in the cash-crunch districts.

Thus, our study shows that payment fintechs are unable to exploit fully the enforcement technology. Alternative payment methods, especially cash, can negate the seniority advantage. Our results suggest that as economies shift toward digital payments, this problem could be mitigated to a certain extent. The increasing importance of digital payments will also accelerate the spread of payment fintechs offering credits with automatic sales-based repayment . However, despite the benefit of the enforcement technology, providers of sales-based credit must still adequately screen and monitor their borrowers. Likewise, they must make their credit contract sufficiently robust to de-incentivize the use of alternative means of payment. But digital transformation and the Internet of Things can help address these issues and facilitate similar financial products even beyond payment fintechs.

Join the Conversation