Union Pacific Railroad train loaded with freight containers | © shutterstock.com

Union Pacific Railroad train loaded with freight containers | © shutterstock.com

This blog is part of this year’s series of posts by PhD students on the job market.

Recent decades have been characterized by a high degree of trade integration, accompanied by increases in both income and wealth inequality. A growing body of work has argued that increased trade exposure can have heterogeneous effects across households. What is the impact of lower trade costs on inequality? How does the level of financial development affect the response of inequality to lower trade costs?

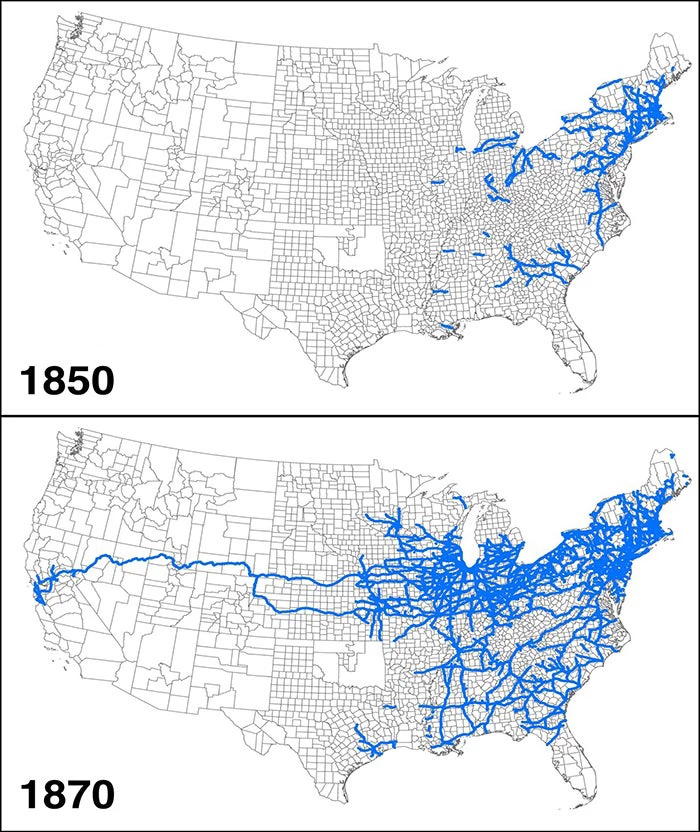

In my job market paper, I answer these questions from a historical perspective. I study the effects of lower trade costs on wealth inequality using the expansion of the railroad network in the United States in the 19th century as an empirical laboratory. Railroad track mileage increased from 9,000 miles in 1850 to approximately 50,000 miles in 1870 (figure 1). Railroad network expansion is a natural empirical setting to study the effect of trade costs as railroads drastically reduced the cost of transporting goods within the United States. Compared with shipping goods via wagons, railroads were an order of magnitude cheaper. The 19th century in the United States is also an ideal setting to study wealth inequality due to the availability of wealth data for all households. Newly digitized complete-count census schedules of 1850, 1860, and 1870 provide data on real estate wealth for every individual in the United States, and the 1860 and 1870 censuses provide data on both real estate and personal wealth.

Figure 1: The US Railroad Network in 1850 and 1870

Following Donaldson and Hornbeck (2016), a county’s market access is defined as a trade cost–weighted sum over populations in all other counties, and it captures how cheaply goods can be transported from this county to all trading partners. A county has greater market access when it is cheaper to trade with another county, particularly when that other county has a larger population. The expansion of the railroad network across the country reduced trade costs drastically and thus increased counties’ access to other markets. While railroad construction is potentially endogenous and may depend on local economic conditions, changes in county market access are primarily due to changes in the railroad network elsewhere, rather than local railroad construction. The identification assumption is that counties with relative increases in market access would otherwise have changed similarly to nearby counties.

I estimate that the increased county-level market access induced by the expanding railroad network led to a significant increase in county-level wealth inequality. From 1850 to 1870, a one standard deviation increase in county market access leads to a 0.023 point increase in the Gini coefficient and a 3.24 percentage point increase in the real estate wealth share of the top 10%. This finding is robust to using different measures of wealth inequality, controlling for time-varying county characteristics, and adjusting for effects of the Civil War and westward migration.

I then show that a dynamic general equilibrium model featuring heterogeneous households, entrepreneurship, financial frictions, and trade can rationalize this result. Railroads are modeled as a device that leads to a decline in trade costs. I calibrate the model to match data moments in the United States in 1850. I use the calibrated model to study how the expansion of the railroad network affected income, wealth, and inequality. Both income and wealth are higher in the economy with lower trade costs. Lower trade costs lead to larger gains at the top of the distribution, increasing both income and wealth inequality. My calibrated model shows that the empirically observed reductions in average trade costs can explain approximately 60% of the observed increase in the real estate wealth share of the top 10% between 1850 and 1870.

Two key channels drive the differential effect of lower trade costs across the wealth distribution in the model. First, similar to Melitz (2003), the increased exposure to trade induces high productivity entrepreneurs to export, while at the same time forcing less productive entrepreneurs who were marginally profitable before railroads to exit. This selection mechanism reallocates market shares and thus incomes toward more productive (and wealthier) households. Second, financial frictions distort household decisions on the extensive margin by reducing the number of households that choose to be entrepreneurs and exporters. This happens because these choices require high levels of wealth to operate at a profitable scale. Financial frictions also affect household decisions on the intensive margin by distorting their production scale. When trade costs go down, constrained entrepreneurs hoping to take advantage of increased trading opportunities face a relatively steeper cost compared to unconstrained (wealthier) entrepreneurs.

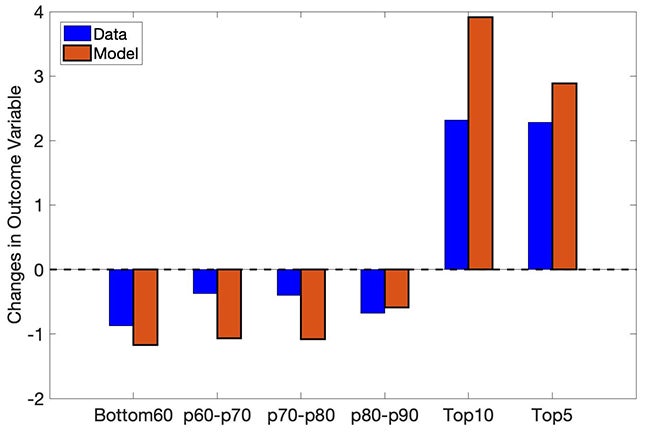

I validate the model by checking that its implied predictions are consistent with the empirical results. First, there is a reallocation of wealth toward the wealthier households. The model implied response of the wealth shares held by different parts of the distribution to a decline in trade costs is quantitatively consistent with the empirical findings (figure 2). Second, financial frictions limit lower wealth households from taking advantage of lower trade costs. The effect of lower trade barriers on inequality is attenuated in a more financially developed economy. My empirical results indicate that the impact of market access on the top 10% wealth share is weaker in states with higher existing financial development , as measured by per capita number of banks, amount of loans, or amount of bank capital in 1850. This result is consistent with the idea that higher credit availability may help low-wealth individuals take advantage of increased economic opportunities.

Figure 2: Effects of Trade Costs across the Wealth Distribution

In terms of welfare, I find that most households in the model economy gain from the railroad induced decline in trade costs. The average household gains 0.65% in consumption-equivalent units. Lower trade costs increase wages, which benefit the poor, and benefit the rich by allowing them to expand production and enter the export market.

My estimates highlight that lower trade costs promote economic growth but at the cost of higher inequality. My results also suggest that, in the presence of credit constraints, the effect of increased trade openness on wealth distribution depends on financial development in the economy . My quantitative framework can be used to study tax policies that can alleviate the growth versus inequality trade-off and ensure equitable growth in the face of declining trade barriers.

References

Donaldson, D. and Hornbeck, R. (2016). Railroads and American Economic Growth: A “Market Access” Approach. The Quarterly Journal of Economics, 131(2):799–858.

Melitz, M. J. (2003). The Impact of Trade on Intra-industry Reallocations and Aggregate Industry Productivity. Econometrica, 71(6):1695–1725.

Join the Conversation