Fruits, vegetables and greens, for sale in a market in Guatemala City

Fruits, vegetables and greens, for sale in a market in Guatemala City

COVID-19 and its associated economic downturn is aggravating the stability of our global food system. Growing stressors to our food system include conflict, increasing inequality, and a changing climate with greater incidences of heatwaves, droughts, floods, and an unprecedented locust outbreak.

Another significant, but rarely talked about stressor threatening our food security are inefficient cold chains. Cold chains are a series of facilities to safely maintain ideal storage conditions for micro-nutrient rich perishable foods from the point of origin to the point of consumption. In many countries these are inexistent or fragmented.

Aside from food insecurity, inefficient cold chains contribute to greenhouse gas (GHG) emissions and can increase the risk of poverty for vulnerable communities.

The good news is, sustainable cold chain investments and technical assistance by Multilateral Development Banks (MDBs) can contribute to building more resilient food systems, improving smallholder livelihoods and buffering against future crisis.

Threats to the food system

Oxfam estimates an 82% increase of people experiencing crisis level hunger by the end of the year. An increase from 149 million to 270 million people in one year. There is a very real large-scale famine crisis looming.

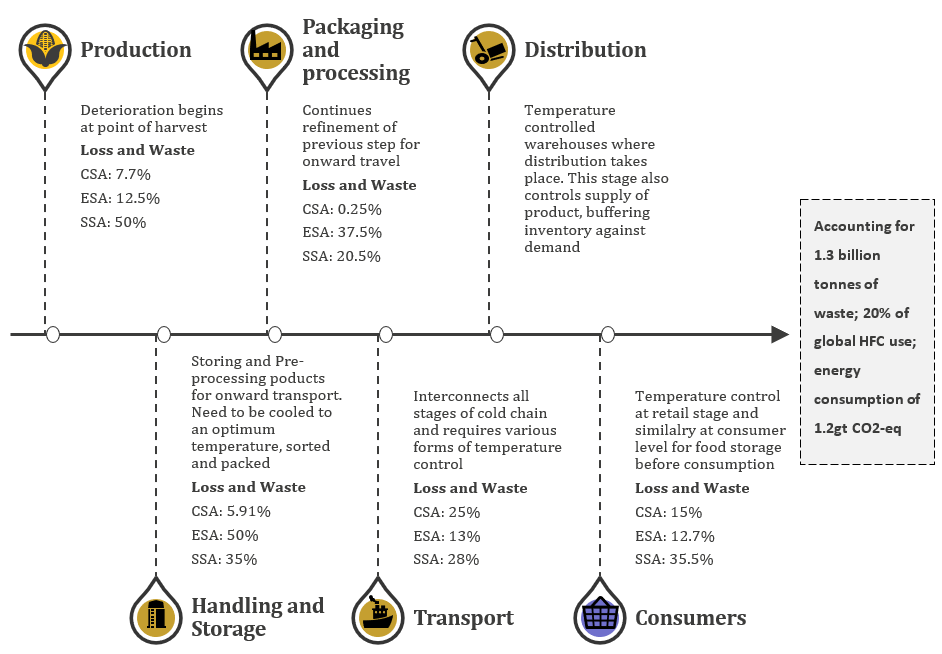

This potential crisis puts food loss into perspective. A third of food is lost or wasted within the value chain, contributing an estimated 8% of GHG emissions, see Figure 1 below. UNEP estimates a staggering 15% of food waste related CO2 emissions come from inefficiency in post-harvest cold chains.

The environmental cost of inefficient cold chains cannot be understated. Currently, refrigeration and cold transport technologies predominantly rely on fossil fuel based energy sources and Hydrofluorocarbons (HFCs) which are a type of fluorinated, or F- gases witha global warming potential 23000 times higher than CO2. Cold chains in agriculture account for 20% of global HFC use.

The value of sustainable cold chains

Aside from decreasing global emissions, sustainable cold chains bring multiple benefits. Not least, the potential to reduce food waste by half, potentially feeding 1 billion people.

Efficient cold chains also enable climate-friendly sustainable development in four key areas;

- energy efficiency;

- improved food security;

- inclusive growth by strengthening livelihoods for smallholders through post-harvest food loss reduction; and

- facilitating control and commercialisation of agricultural produce in regional and international markets.

One example of efficient cold chain resilience can be seen in the case of Uganda’s dairy and fish value chains. Uganda’s fish value chain, lacking access to adequate cold chains, collapsed with the additional challenges posed by COVID-19. The dairy sector however has been using a cooperative driven, bottom-up aggregated approach to invest in cold chain and storage solutions. By building resilience into the supply chain, small scale dairy farmers were protected from supply and demand fluctuations during the pandemic.

Food security is a focal area at MDBs. The Asian Development Bank’s (AsDB) 2030 Strategy identifies ‘promoting rural development and food security’ as its fifth operational priority. The African Development Bank’s (AfDB) ‘Feed Africa’ strategy has ambitious goals to eliminate extreme poverty and end hunger and malnutrition in Africa by 2025. The EBRD’s Green Economy Transition 2.1 strategy has ‘sustainable food systems’ as one of their Green Transition Acceleration Platforms.

Some MDBs are already working on this, the World Bank’s recent flagship report on addressing food loss and waste recommends financing for storage systems or cold chains. This was followed by the issuance of sustainable development bonds in Scandinavian currencies amounting to USD550 million, to enhance Scandinavian investor awareness of food loss and waste. The IBRD in addition is providing USD4.6 billion in lending to middle-income countries to address farm to fork food loss and waste. Furthermore the International Finance Corporation (IFC) notes reducing post-harvest food loss and improving food security through cold storage facilities as a strategic area in climate smart agriculture. However, because of the complex nature of cold chains requiring various levels of cooperation it can be difficult to implement successfully. One action for MDBs is to integrate cold chain considerations into their climate risk appraisals for agriculture projects. This can also help identify areas of future risk.

MDBs are actively deploying large amounts of capital to respond to COVID-19. For instance, the World Bank announced USD160 billion in funds to respond to the health, social and economic impacts of COVID-19. Resilient food value-chains form a component of this response.

Sustainable cold chain investments have a place in the recovery story. By offering strategic investments in physical and human capital it could deliver climate, health, and economic benefits. For instance, creating sustainable cooling hubs, by aggregating rural cold chain demand, gives access to energy efficient cold storage for many. This is vital for medicines, along with food security, nutrition and inclusive growth.

To learn more broadly about the importance of sustainable cooling and the actions that can be taken by Development Finance Institutions, read E3G’s latest briefing here.

Join the Conversation