Conventionally the governing law should not affect the cost of borrowing in international markets. If it did, borrowers would use the cheaper jurisdiction. Also, if somehow the spread differed at the time of the launch of the bond, trading in the secondary market should eliminate the difference. A recent paper shows otherwise: Sovereign bonds issued under the UK law had a persistent higher spread than those under the US law, but only since the global financial crisis in 2008.

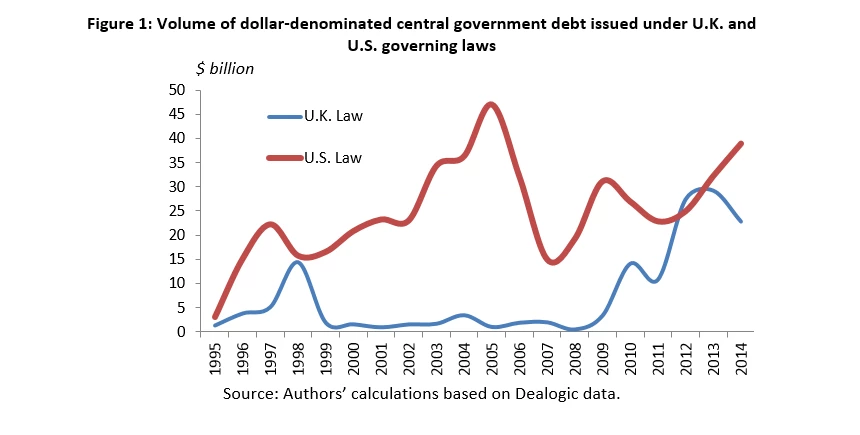

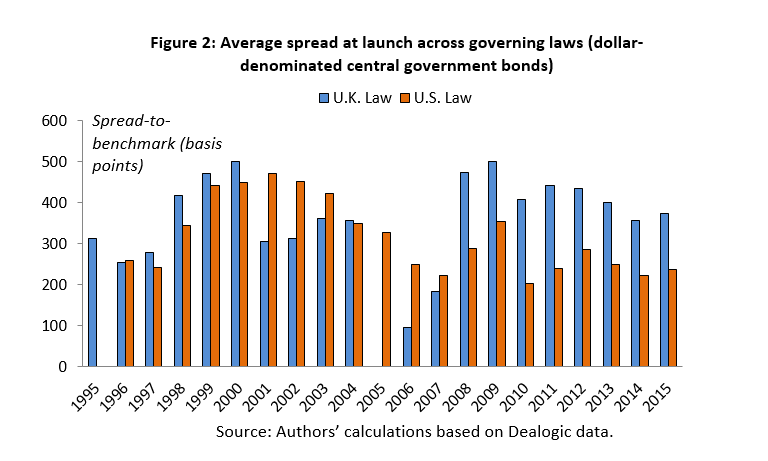

Historically, U.S. law issuances formed the dominant part of the volume of dollar-denominated central government bond issuances, barring 2012 when U.K. law issuances briefly overtook U.S. law issuances (Figure 1). There were also divergences in characteristics of dollar-denominated central government bonds issued across the two jurisdictions. Average spread at launch for bonds issued under U.K. law became distinctly higher after the global financial crisis in 2008 (Figure 2). On average, bonds issued under U.K. law also had weaker ratings and shorter tenors post-crisis.

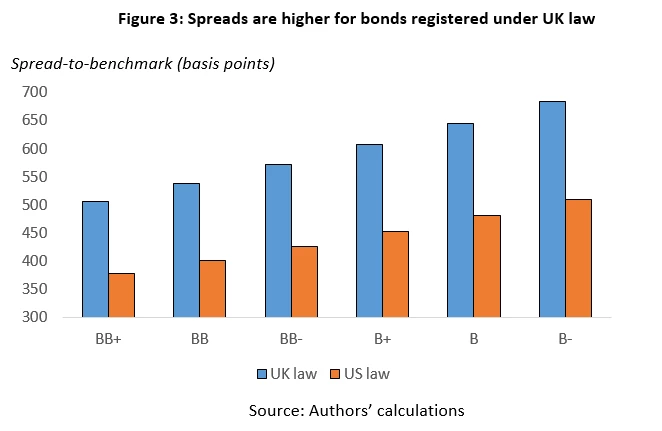

An analysis of 435 U.S. dollar–denominated bonds issued by 53 emerging market sovereigns during 1990–2015 reveals that controlling for bond and issuer characteristics, after the financial crisis of 2008, the launch spread of sovereign bonds issued under U.K. law has been higher than those issued under U.S. law, by 130 basis points for BB+ bonds and 175 basis points for B- bonds. The absolute impact is higher for lower rated bonds, for instance, for Ghana, which is rated B- by S&P (Figure 3).

An analysis of 435 U.S. dollar–denominated bonds issued by 53 emerging market sovereigns during 1990–2015 reveals that controlling for bond and issuer characteristics, after the financial crisis of 2008, the launch spread of sovereign bonds issued under U.K. law has been higher than those issued under U.S. law, by 130 basis points for BB+ bonds and 175 basis points for B- bonds. The absolute impact is higher for lower rated bonds, for instance, for Ghana, which is rated B- by S&P (Figure 3).

The difference in spreads persists in the secondary market even after 180 days. This effect was not significant for investment grade bonds. The post-crisis impact of governing law on sovereign bond spreads is not explained by collective action clauses, or first-time bond issuances. Instead, the difference seems to be related to the perception that U.S. law offers stronger investor protection, and that the investor base for bonds issued under U.S. law is larger than that for bonds issued under U.K. law.

The magnitude of spread difference is large enough to deserve detailed analysis of their effect on public finances and a re-examination of governments’ issuing strategies. Governments tend to overlook the fact that, however cumbersome or costly the SEC registration process may appear, it also helps them tap the U.S. investor, signal greater transparency and substantially reduce the cost of debt.

For a country rated B- (say, Ghana), a saving of 175 basis points in annual interest costs on a $1 billion bond would translate into a saving of $17.5 million in the first year alone, far exceeding any additional cost that may be required for tougher registration requirements. Over a 10 year period, that would amount to a saving of $175 million.

Readers may also be interested in two related papers – on predicting sovereign ratings for unrated countries and the concept of relative risk ratings.

Join the Conversation