Imagine having to skip work every month to travel to the city center just to pay your electricity bill or your child’s school fee? Would you not worry if your income relied on remittances and you were unable to pay rent because they were tied up in a network of agents? And wouldn't it frustrate you if you didn’t have a say in how your salary was spent or invested?

Having a bank account could help in all of these situations. Most of us probably have auto-pay set up so we don't need to worry about our monthly bill payments or money transfers. But the conveniences we take for granted are out of reach for the world's 1.1 billion women who lack an account. According to World Bank’s Global Findex database, men in developing countries are 9 percentage points more likely than women to own an account. The gap is largest in South Asia, where only 37 percent of women have an account compared with 55 percent of men.

A new report prepared for the Turkish G20 presidency by the World Bank Development Research Group, Better than Cash Alliance, Bill & Melinda Gates Foundation, and Women's World Banking shows how digital financial services can help women take control of their economic lives. The report also explores the ways governments, businesses, and donors can help ensure these services are accessible to all, especially women.

Women face several hurdles to getting an account. Some think it's too expensive to open and operate one, while others lack the necessary documentation or live too far away from the nearest bank branch. But that doesn’t mean they don’t need an account. Even in the absence of formal banking facilities, women tend to save money through informal means, like a community savings group or local agent. The problem is that these informal methods are often unsafe or have a high negative interest rate. Some women have no choice but to keep cash savings at home, where they are easily pilfered by covetous husbands or other relatives.

Digital financial services can help women deal with these challenges. First and foremost, women can avoid costly trips to faraway bank branches and transact from the convenience of their homes. In rural Malawi and Nigeria, women have started using mobile phones through a network of agents to make deposits and withdrawals. They find it cheaper, more convenient, and more efficient than using cash. The increased privacy and control afforded by digital payments helped female farmers in Niger strengthen their financial autonomy and household bargaining power. With their earnings, they were better able to invest in their business, increase profits, and get jobs.

New financial services are also helping farmers ride out irregular harvests that once would have spelled disaster. In Kenya, a micro-insurance scheme makes automatic payments to farmers when there's a drought or excessive rainfall. Women who use Kenya's flagship mobile money service M-Pesa can now borrow funds from family or friends through a simple text message. Some mobile money providers record mobile transactions to create an initial credit history of their clients which can make them eligible for larger loans.

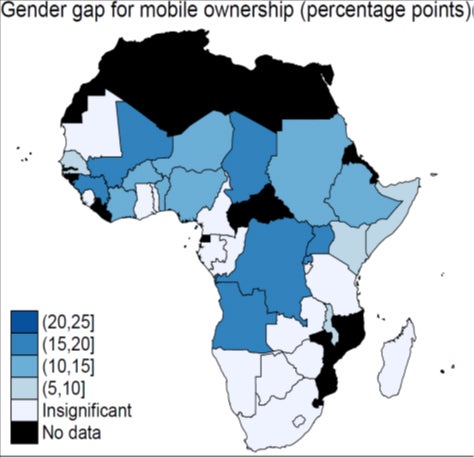

However, there are several challenges which keep women from adopting these services. Some 1.7 billion women in low and middle-income countries do not own mobile phones in the first place. This might be because they're too expensive or women are afraid of being harassed with unwanted calls and messages. Social norms that discourage women's phone use could also be a factor. Women who do have access to a mobile handset do not always use it to make digital financial transactions. Reasons include lack of trust in agents and operators; poor network quality and coverage; and low technical and financial literacy or confidence.

Source: Gallup World Poll, 2014.

Women in developing countries are also less likely than men to have Internet access in their home. In South Asia, for example, women are half as likely as men to be online. Consequently, while 54 percent adults in high-income OECD countries report using the Internet to make online payments, only 10 percent of adults from developing economies do so.

In addition to access problems, women are locked out of the financial system by sexist laws. Yet even women who are willing and able to use financial services often struggle to do so since there's a dearth of financial tools that actually cater to their unique needs. Weak consumer protection regimes reduce women's trust in financial institutions, as they are naturally more risk averse than men. Some large scale digitization programs for women like Pakistan’s Benazir Income Support Program have stumbled because the users didn't know how to use the ATM cards or PIN codes.

Governments have the most power and responsibility to boost women's access to financial services. They can start by creating or digitizing national identification databases and giving a unique digital identification number to each citizen and resident. To avoid the hassle of using PIN codes, governments can use biometrics to capture a user’s identity. They can also support the financial and telecom sector through policies that encourage uptake of digital financial services. At the same time, they should build strong consumer protection regimes to safeguard users from fraud and abuse. Instead of cash, governments should use digital technology to pay wages and distribute social benefits. Some governments, like Mexico, are already doing this – and saving billions of dollars as a result. Finally, governments should scrap laws that discriminate against women and curb their access to financial services.

Banks and mobile network operators can share their respective customer networks and make financial services cheaper and more accessible for everybody. Financial service providers can create new ways of capturing credit history and design products that suit women’s needs. For their part, businesses can pay their employees digitally and invest in infrastructure that supports such innovations. All of these efforts can benefit from the technical and financial support of international donors.

Digital financial services are a proven way to empower women. We hope all stakeholders will read our report and put its findings to good use.

Join the Conversation