Also available in:

Español

Download the January 2018 Global Economic Prospects report.

The 2014-16 collapse in oil prices was driven by a growing supply glut, but failed to deliver the boost to global growth that many had expected. In the event, the benefits of substantially lower oil prices were muted by the low responsiveness of economic activity in key oil-importing emerging markets, the effects on U.S. activity of a sharp contraction in energy investment and an abrupt slowdown in key oil exporters.

Biggest drop in oil prices in modern history

Between mid-2014 and early 2016, the global economy faced one of the largest oil price declines in modern history. The 70 percent price drop during that period was one of the three biggest declines since World War II, and the longest lasting since the supply-driven collapse of 1986.

Real oil prices

Source: World Bank.

Source: Rystad Energy NASWellCube Premium.

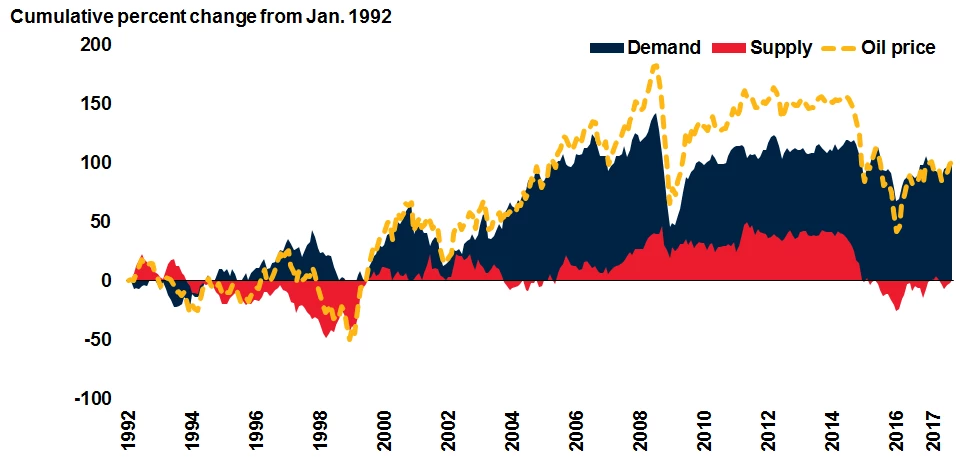

Supply glut reinforced by weakening demand prospects

The initial drop in oil prices from mid-2014 to early 2015 was primarily driven by supply factors, including booming U.S. oil production, receding geopolitical concerns, and shifting OPEC policies. However, deteriorating demand prospects played a role as well, particularly from mid-2015 to early 2016. This partly explains why the oil price plunge failed to provide a subsequent boost to global activity.

Oil price decomposition

Source: World Bank.

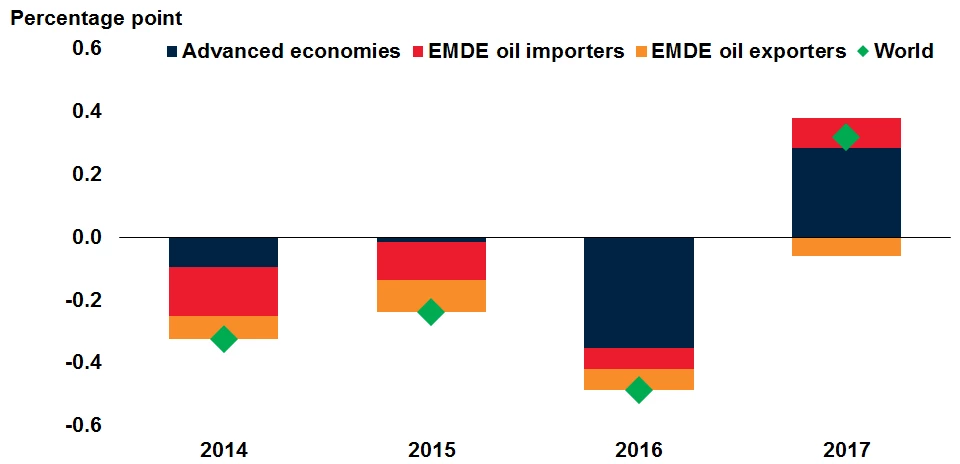

Disappointing growth in oil importers

Rather than lifting global growth, the oil price plunge was accompanied by a slowdown in 2015 and 2016. A sharp deceleration in oil-exporting economies dragged global economic activity down, but disappointing growth in oil-importing economies, including the United States, China and non-oil commodity exporting emerging markets, explained most of the negative surprise around that period.

Contribution to global growth forecast errors

Source: World Bank.

Sharper impact for some oil exporters

Among commodity exporters, fiscal consolidation was less pronounced and economic activity recovered more quickly in countries with flexible exchange rates and higher levels of export diversification.

Change in overall fiscal balance in oil-exporting EMDE sub-groups

Sources: International Monetary Fund, World Bank.

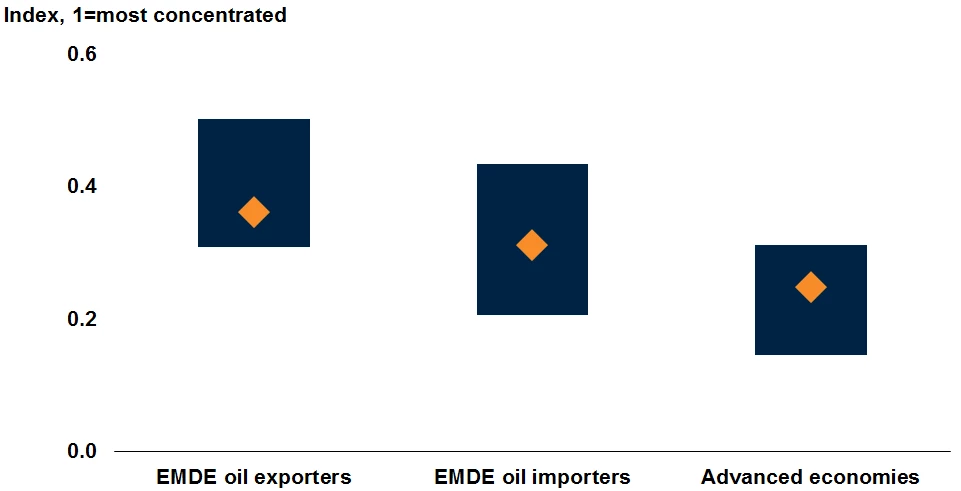

Need for greater diversification for oil exporters

Although low oil prices spurred significant policy responses in oil-exporters, more sustained reform efforts will be needed given subdued long-term prospects for oil prices. Oil exporters still have among the lowest levels of export diversification of any other country group.

Export concentration, 2016

Sources: United Nations Conference on Trade and Development (UNCTAD), World Bank.

Long-term price forecast downgraded

Long-term oil price forecasts have been considerably downgraded over the last few years, and numerous factors limit upside risks to the outlook. These include: the potential for further gains in shale oil production, an accelerated uptake of more fuel-efficient technologies, and policies supporting renewable energies.

Oil price forecasts

Source: World Bank.

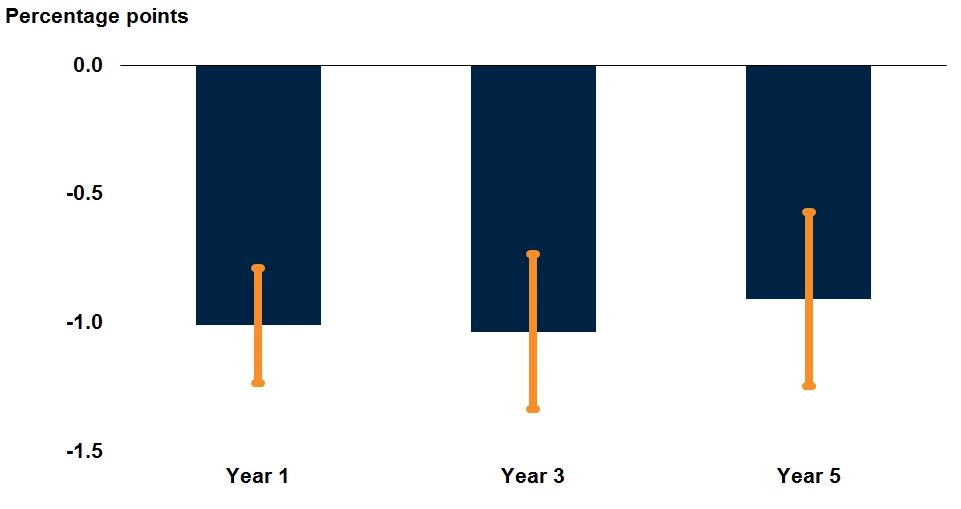

Hangover from the price plunge

The 2014–16 oil price plunge has cast a long shadow for oil exporters. Significant declines in investment and output generally lead to weaker potential output growth over extended periods of time. Expectations of markedly lower-than-expected oil prices ahead underscores the urgency of reforms to restore growth and fiscal sustainability.

EMDE potential growth response to contraction events

Source: World Bank.

Download the January 2018 Global Economic Prospects report.

The 2014-16 collapse in oil prices was driven by a growing supply glut, but failed to deliver the boost to global growth that many had expected. In the event, the benefits of substantially lower oil prices were muted by the low responsiveness of economic activity in key oil-importing emerging markets, the effects on U.S. activity of a sharp contraction in energy investment and an abrupt slowdown in key oil exporters.

Biggest drop in oil prices in modern history

Between mid-2014 and early 2016, the global economy faced one of the largest oil price declines in modern history. The 70 percent price drop during that period was one of the three biggest declines since World War II, and the longest lasting since the supply-driven collapse of 1986.

Real oil prices

Source: World Bank.

Notes: Real oil prices are calculated as the nominal price deflated by the international manufacturers unit value index, in which 100=2010. World Bank crude oil average. Last observation is November 2017.

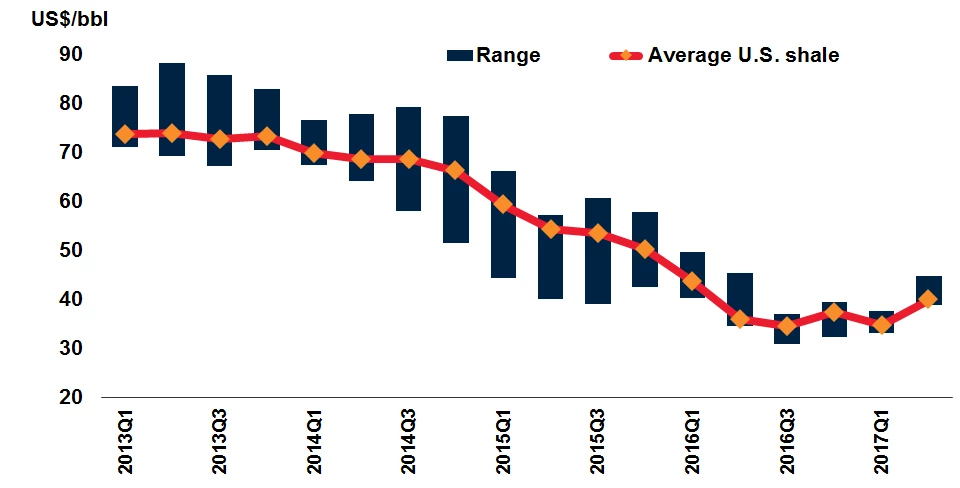

Rising efficiency gains in U.S. shale oil

Booming U.S. shale oil production played a significant role in the oil price plunge from mid-2014 to early 2016. Efficiency gains in the sector lowered break-even prices considerably, making U.S. shale oil the de facto marginal cost producer on the international oil market.

Average wellhead break-even oil price

Source: Rystad Energy NASWellCube Premium.

Notes: Does not include test activity, where well was shut-down after completion. Last observation is 2017Q2.

Supply glut reinforced by weakening demand prospects

The initial drop in oil prices from mid-2014 to early 2015 was primarily driven by supply factors, including booming U.S. oil production, receding geopolitical concerns, and shifting OPEC policies. However, deteriorating demand prospects played a role as well, particularly from mid-2015 to early 2016. This partly explains why the oil price plunge failed to provide a subsequent boost to global activity.

Oil price decomposition

Source: World Bank.

Notes: Based on the decomposition of oil price changes from a structural vector autoregressive (SVAR) model including global industrial production, global oil production, oil and metals prices. The identification scheme is comparable to that suggested in Caldara, Cavallo, and Iacoviello (2016), putting restrictions on short-term oil supply and demand elasticities based on a survey of the literature. Last observation is October 2017.

Disappointing growth in oil importers

Rather than lifting global growth, the oil price plunge was accompanied by a slowdown in 2015 and 2016. A sharp deceleration in oil-exporting economies dragged global economic activity down, but disappointing growth in oil-importing economies, including the United States, China and non-oil commodity exporting emerging markets, explained most of the negative surprise around that period.

Contribution to global growth forecast errors

Source: World Bank.

Notes: EMDEs: emerging market and developing economies. Forecast errors computed as the difference between actual global growth and forecasts at the beginning of each calendar year. Aggregate growth rates calculated using constant 2010 U.S. dollar GDP weights.

Sharper impact for some oil exporters

Among commodity exporters, fiscal consolidation was less pronounced and economic activity recovered more quickly in countries with flexible exchange rates and higher levels of export diversification.

Change in overall fiscal balance in oil-exporting EMDE sub-groups

Sources: International Monetary Fund, World Bank.

Notes: EMDEs: emerging market and developing economies. Sample includes 27 oil-exporting EMDEs (excludes Albania, Bolivia, Brunei Darussalam, Ghana, Libya, Myanmar, South Sudan, and Turkmenistan). Change in overall fiscal balance is measured from 2014-16. Exchange rate classification is based on the IMF’s Annual Report on Exchange Arrangements and Exchange Restrictions database, in which countries are ranked 0 (no separate legal tender) to 10 (free float). “Pegged” denotes countries ranked 1 to 6. “Floating” denotes countries ranked 7 to 10. Above average and below average oil revenue groups are defined by countries above or below the sample average of oil revenues as a share of GDP based on 2014 data.

Need for greater diversification for oil exporters

Although low oil prices spurred significant policy responses in oil-exporters, more sustained reform efforts will be needed given subdued long-term prospects for oil prices. Oil exporters still have among the lowest levels of export diversification of any other country group.

Export concentration, 2016

Sources: United Nations Conference on Trade and Development (UNCTAD), World Bank.

Notes: EMDEs: emerging market and developing economies. Orange diamonds denote the median and blue bars represent the interquartile range of individual country groups. Sample includes 34 oil-exporting EMDEs (excludes South Sudan), 116 oil-importing EMDEs, and 36 advanced economies. Concentration index measures the degree of product concentration, where values closer to 1 indicate a country’s exports are highly concentrated on a few products.

Long-term price forecast downgraded

Long-term oil price forecasts have been considerably downgraded over the last few years, and numerous factors limit upside risks to the outlook. These include: the potential for further gains in shale oil production, an accelerated uptake of more fuel-efficient technologies, and policies supporting renewable energies.

Oil price forecasts

Source: World Bank.

Note: Forecasts from various editions of World Bank’s Commodity Markets Outlook report.

Hangover from the price plunge

The 2014–16 oil price plunge has cast a long shadow for oil exporters. Significant declines in investment and output generally lead to weaker potential output growth over extended periods of time. Expectations of markedly lower-than-expected oil prices ahead underscores the urgency of reforms to restore growth and fiscal sustainability.

EMDE potential growth response to contraction events

Join the Conversation