Poor rainfall is one of the greatest risks faced by poor farmers throughout the world, but success has been elusive in developing private-sector financial products to manage this risk. Traditional indemnity insurance is not well-suited to smallholder farms (due to asymmetric information and high verification costs), and indeed this market has failed to materialize. Weather index insurance makes payouts based on readings at local weather stations (such as the amount of rainfall over a particular time period), and can have lower costs than indemnity insurance. However, multiple pilots have shown limited demand, leading many to conclude that stand-alone weather index insurance products are not viable. People have gained coverage in

cases where insurance was heavily subsidized or bundled with loans, but

research suggests that customers would choose loans without insurance if they could. Farmers tend to have some savings that can be drawn upon if a shock occurs, but there are lots of demands on savings and it is likely to provide insufficient risk coverage.

In a new

working paper (jointly authored with Jeremy Tobacman), we consider instead bundling insurance with savings. There is good precedent for this in commercial markets. For example, “whole life” insurance policies (in which customers are refunded their premiums at the end of a term) are essentially savings vehicles that receive insurance in lieu of interest. We hypothesized that a new product called a Weather Insurance Saving Account, or “WISA,” might have similar commercial viability, while providing insurance against rainfall risk.

We conducted an experiment with the twin objectives of studying demand for such a product and testing theories of decision-making under risk. We invited farmers into a computer lab in Ahmedabad, India, and elicited their demand for WISAs using a mechanism in which farmers are incentivized to reveal their true valuations of the products. Custom-designed weather insurance was underwritten by ICICI-Lombard for the experiment, and the participants played for real stakes involving the opportunity to receive actual WISAs. We adopted an experimental setup that allowed us to see how each participant valued multiple WISAs, as we varied the amount of insurance in the bundle.

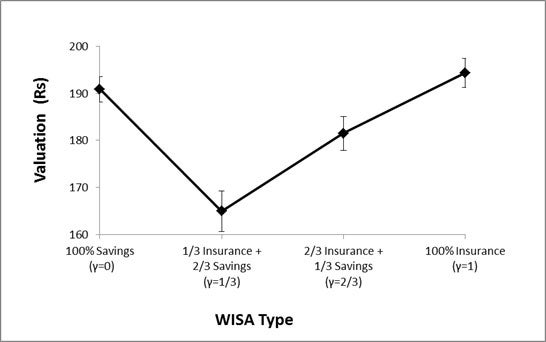

The results were somewhat surprising: we found that individuals prefer both pure insurance and pure savings to any intermediate WISA type.

WISA Demand versus WISA Insurance Share

Demand is higher for pure savings and pure insurance compared to interior mixtures.

This pattern reflects within-subject differences.

This pattern reflects within-participant variation, not heterogeneity in the market. Not only does this finding suggest that market demand for WISAs would be low, but it also contradicts standard theoretical predictions. Conventional insurance theory predicts that a risk-averse individual might prefer insurance to savings or savings to insurance, but can’t prefer both of these things to a mixture of the two. So, the results are at first perplexing.

What could be causing this deviation from conventional insurance theory? One hypothesis is that the participants found the WISAs to be confusing, and this lowered their demand. To permit a test of this, we had randomly varied whether participants received (complicated) explanations of the WISAs as a combination of insurance and saving or (simpler) explanations of the WISAs as insurance products with minimum payouts. This manipulation did not result in any change in observed patterns of demand.

A second possible explanation can be found in prospect theory, which incorporates “diminishing sensitivity” to losses. This means that if you lose money, the first dollar lost is much more painful than say, the 1000

th dollar lost. In other words, aversion to losing $100 from your reference point is much larger than the difference in aversion between losing $1000 and losing $1100.

If people have diminishing sensitivity to losses, low demand for a WISA makes sense. This is because a WISA provides just a little bit of insurance, and a small insurance payout after a large loss is not very attractive. For instance, imagine someone tried to sell you an insurance policy that would pay $100 if your house burned down. Even if this policy was actuarially appealing, you might value it little, perceiving its possible payout as trivial in proportion to such a large loss. Instead, for insurance to be appealing, a large percentage of the loss would need to be covered.

Our research suggests that providing rainfall insurance bundled with savings accounts is unlikely be attractive, because even if people have demand for insurance they will not value the small amount of coverage provided by this type of product. Instead, the study suggests that financial products that cover a large proportion of potential losses are likely to be more attractive. Given that stand-alone insurance products (which would provide more coverage) have also shown low demand, this means that new solutions are needed to help poor farmers deal with rainfall risk.

Get updates from Let's Talk Development

Thank you for choosing to be part of the Let's Talk Development community!

Your subscription is now active. The latest blog posts and blog-related announcements will be delivered directly to your email inbox. You may unsubscribe at any time.

The e-mail address: [email] is already subscribed for newsletters.

Join the Conversation