On affordability grounds alone, millions of people in the Middle East and North Africa (MENA) region could be excluded from today’s information revolution. Meeting this challenge has become a top regional priority. Many countries in the Arab world have identified broadband Internet as a critical input to the broader objective of nation building and the transition to a knowledge-based economy. There is growing consensus that broadband Internet is critical in fostering sustainable economic development and job creation, and a key component of strategies for reducing poverty, enhancing job opportunities, and advancing trade integration. Indeed broadband is expected to have a similar impact on the transformation of the economy and of society as a whole as the printing press, steam engines, or electricity had in the past. But for it to have its full impact, people will need access to it.

On affordability grounds alone, millions of people in the Middle East and North Africa (MENA) region could be excluded from today’s information revolution. Meeting this challenge has become a top regional priority. Many countries in the Arab world have identified broadband Internet as a critical input to the broader objective of nation building and the transition to a knowledge-based economy. There is growing consensus that broadband Internet is critical in fostering sustainable economic development and job creation, and a key component of strategies for reducing poverty, enhancing job opportunities, and advancing trade integration. Indeed broadband is expected to have a similar impact on the transformation of the economy and of society as a whole as the printing press, steam engines, or electricity had in the past. But for it to have its full impact, people will need access to it.

As a consequence, an increasing number of countries across MENA are adopting national broadband strategies to promote broadband access. Today 11 countries out of 19 in the region have already adopted such policies. The adoption of a national broadband strategy or policy means that a country is making dedicated efforts to stimulate broadband market development in a systematic and holistic way with all key stakeholders. At the core of such a plan are often ambitious national targets for broadband penetration or coverage. For example, the Arab Republic of Egypt’s “eMisr” National Broadband Plan calls for about 22 percent of households subscribed to fixed broadband by 2015 and about 40 percent by 2021.

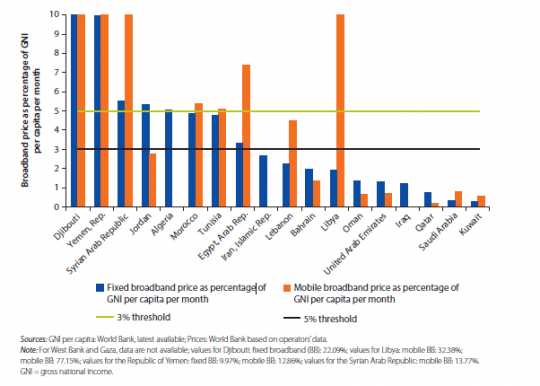

The price of broadband service will play a critical role in achieving these targets. According to the International Telecommunication Union (ITU), broadband penetration grows rapidly after the level of retail broadband price falls below 3 to 5 percent of average monthly income. In the MENA region, fixed broadband prices constitute roughly 3.6 percent of the average monthly income per capita, while mobile broadband prices stand at about 7.7 percent. While Djibouti, Syria, and the Republic of Yemen are significantly above the 5 percent threshold, a number of countries (i.e., Algeria, Egypt, Jordan, Libya, Morocco, and Tunisia) have just reached the level that makes rapid broadband takeoff possible.

Fixed and Mobile Broadband Prices

But the current level of broadband prices is not low enough to be truly inclusive. There is an ongoing risk that millions of people will remain excluded from the information revolution that is shaping the modern world. In countries such as Algeria, Djibouti, Morocco, Syria, Tunisia, and the Republic of Yemen, both fixed and mobile broadband services are far from being affordable for at least 60 percent of the population. For instance, a representative household in the lowest 60 percent income bracket of Morocco would need to spend about 26 percent of its disposable income to afford fixed broadband services and about 23 percent to afford mobile services. In spite of important reforms undertaken by Morocco, a leader in many respects, broadband services are still unaffordable for the majority of the population. In Yemen, a representative household in the lowest 60 percent income bracket would need to spend about 49 percent of its disposable income to afford fixed broadband services and about 38 percent to afford mobile services.

In our new report Broadband Networks in the Middle East and North Africa: Accelerating High –Speed Internet Access to be launched February 6 in Abu Dhabi, we identify the key factors limiting the development of broadband. For most countries in the region it is a lack of both effective competition and appropriate incentives to deploy and/or fully utilize infrastructure. Addressing these factors would allow the region to leverage two very distinctive assets more effectively. The first is the world class broadband fixed technologies such as Fiber To the Home / The Building or mobile technologies such as 4G/LTE that are currently being rolled out. The second is the extensive terrestrial fiber networks belonging to utilities that could potentially be opened up to telecoms operators. A strategic framework of reforms could speed up the deployment of cutting edge technology and extend the geographical reach and resilience of national networks connecting countries, regions, and cities. More competition would also guarantee that the new technologies and expanded networks were more affordable. Lower costs would increase access, especially for the region’s large youth population, who are the future engine of the economy and of society. Lowering the barriers of cost will ensure that broadband internet has its full developmental impact.

Join the Conversation