Metal industry worker.

Metal industry worker.

Aluminum is critical for the energy transition, powering many low-carbon technologies such as wind turbines, batteries, electrolyzers for renewable hydrogen, carbon storage for low-carbon hydrogen, transmission wires, and hydroelectric plants

It is also essential for solar photovoltaic (PV) technologies. As technology now stands, there is—and will be—no solar power without aluminum, which accounts for over 85 percent of most solar PV components today.

With the number of solar PVs set to increase to meet climate targets, so will the demand for aluminum. The World Bank estimates that demand for aluminum will more than double in a 2-degree climate scenario. Some estimates place demand for solar PV in 2050 at more than a third of current levels.

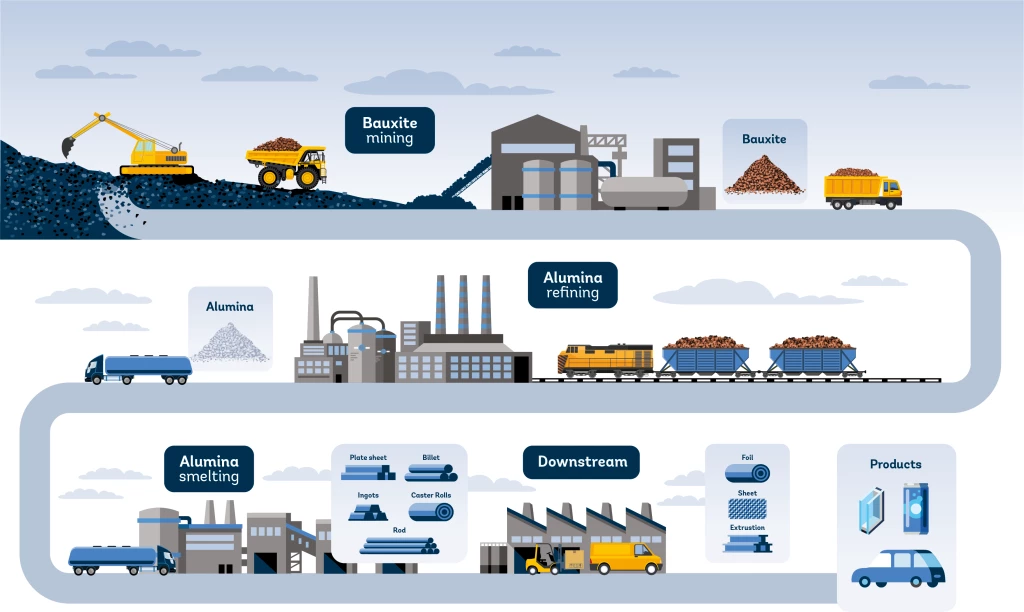

How is aluminum produced?

|

| Primary aluminum production consists of a multistage process:

|

Aluminum faces a competitiveness and high-carbon problem

The aluminum industry counts many producers, including many established refineries and smelters. Australia is only involved in the refining stage, while Canada, India, and Norway take part mainly in the smelting stage. Countries such as Brazil and China are present along the whole value chain. Others, such as Guinea, are involved in mining bauxite and refining alumina.

But over the past decade, relatively low global prices and intense competition have led to the closure and mothballing of much of the production capacity in many countries. At the same time, developing new aluminum production capacity has been challenging because of high capital, energy, and input costs.

Add to this an uncertain market with volatile prices. In March 2022, aluminum prices reached an all-time high because of the Ukraine-Russia war, leading to overstocking by many buyers. While prices have since decreased, speculation about future prices and stocks remains.

Aluminum production also has a large carbon emissions footprint, generating emissions throughout the whole supply chain from bauxite mining to aluminum refining and smelting. The World Bank estimates that under the International Energy Agency's 2-degree scenario, total emissions from aluminum for solar PV could be as much as 840 MtCO2e—more than Germany's total emissions in 2019.

Aluminum is critical for the energy transition. Not only do we need more of it, it has to be cost-competitive and low-carbon. Our new report offers insights on how to achieve this, while identifying new opportunities for developing and middle-income countries.

Demetrios Papathanasiou, Global Director for the World Bank's Energy and Extractives Global Practice

How to support a stable supply of cost-competitive, low-emissions aluminum?

A new report by the World Bank’s Climate-Smart Mining (CSM), Competitiveness of Global Aluminum Supply Chains Under Carbon Pricing Scenarios for Solar PV, examines aluminum competitiveness in the context of potential carbon prices.

One key takeaway is that decarbonization across the aluminum supply chain is essential to retaining competitiveness and diversifying supply. Decarbonizing the entire aluminum value chain—beyond electricity used to produce the metal—is critical to reducing emissions to the largest extent possible and ensuring that producers, including in low- and middle-income countries, can compete in an increasingly carbon-constrained world.

The good news is that several options exist to promote decarbonization across the aluminum value chain, including using more renewable-generated electricity to power smelters and/or using carbon-free anodes. However, more investment and research and development are needed, especially in non-electricity-related technology, to decarbonize the entire aluminum value chain and, in the process, ensure producers remain competitive

Another option is recycling. Aluminum is one of the most recycled elements, with the potential for near-infinite recyclability. Between 42 and 70 percent of aluminum is recycled at the end of its life, with rates as high as 90 percent in some countries. Using recycled aluminum reduces the carbon footprint of the material by up to 20 times. Yet the recycled content of new aluminum products has been estimated at only 34 to 36 percent. Finding ways to increase the supply of recycled aluminum, by increasing scrap collection and encouraging circularity is essential to decarbonizing the aluminum sector, and providing competitive, low-emissions material for the energy transition.

The report shows exactly how important it is for sectors to work together to ensure a successful transition to a low-carbon economy. Low-carbon aluminum, produced from renewable power, is crucial for the future of the aluminum industry and a more sustainable world.

Luciano Alves, CFO of Companhia Brasileira de Aluminio

Carbon pricing is not enough

Our research shows that while carbon pricing can play an important role in decarbonizing the aluminum sector, a balance must be struck to ensure sufficient capacity to meet the demand driven by the energy transition.

When carbon prices are applied, our modeling shows that opportunities for new and existing aluminum smelters are limited. This means that production will be restricted to existing producing countries such as China and India or that the price of aluminum will have to rise above historical levels to justify investments in new smelters in new countries. In both scenarios, this will result in higher production costs of low-carbon technologies such as solar PV panels, electric vehicles, and transmission lines.

The importance of aluminum to the low-carbon transition, the competitiveness challenges many producers face, the volatility of its market, and its potentially high greenhouse gas emissions warrant further research into the metal, its competitive position (especially in the context of climate policy such as carbon taxes) and alternative decarbonization options. Our hope is that our research will initiate discussions among partners to unleash more opportunities for green aluminum for the energy transition.

Subscribe here to stay up to date with the latest Energy blogs.

Related:

Climate-Smart Mining: Minerals for Climate Action

Competitiveness of Global Aluminum Supply Chains Under Carbon Pricing Scenarios for Solar PV (PDF) [Part I]

Competitiveness of Global Aluminum Supply Chains Under Carbon Pricing Scenarios for Solar PV (PDF) [Part II]

Minerals for Climate Action - The Mineral Intensity of the Clean Energy Transition

Sufficiency, Sustainability, and Circularity of Critical Materials for Clean Hydrogen

Blog: How to secure a sustainable lithium supply chain for electric vehicles?

Blog: How to make artisanal and small-scale mining forest-smart

Join the Conversation