Evidence gathered from transition economies shows that

formal work may not pay, particularly for low-wage earners. Synthetic measurements of work disincentives, such as the formalization tax rate or the marginal effective tax rate, confirm a significant positive correlation between these measurements and the probability of informal work. These measures are especially informative for impacts at lower wage levels, where informality is highest. Policymakers who want to increase formal work can use these measurements to determine the optimal labor taxation rates for low-wage earners and reforming the design of benefit systems.

Informal work is an integral part global labor market. In developing countries, it is often a substantial source of employment, production and income. However, it comes with several undesired economic and social outcomes. In informal work, economic activities are undeclared. This lowers competitiveness and growth, reduces the coverage of labor regulations and programs, weakens social cohesion, and diminishes tax receipts. These disadvantages may outweigh informal employment’s prospective positive contributions to job creation and poverty reduction.

There are several reasons why workers might prefer to stay in informal jobs over formal employment. Regulations in the product and labor market, such as product licensing, employment protection legislation, and minimum wages, might be too stringent. Certain administrative procedures related to paying taxes, keeping accounts, and complying with business and labor regulations might deter people from operating in the formal sector. Workers and employers might want to avoid paying taxes on revenues, income, profits, or property, and social security contributions. Formal income might lead to a withdrawal of social benefits, such as social assistance or unemployment benefits, so that people might prefer informal, or no work, over formal work. Finally, weak enforcement of existing legislation on regulations and taxation might lower the risk of getting caught when circumventing these obligations.

Source: IZA World of Labor

Measuring the incentives and disincentives posed by labor taxation and social benefit design sheds light on the question of whether it is actually prudent for the working-age population to engage in formal employment, register their activities, and pay taxes and contributions on income generated. This question is particularly relevant for policymakers who want to increase work formalization and quantify the disincentives workers face in this process. Measurements of incentives and disincentives can help the design of taxation and benefit systems, identify constraints, and lead to an understanding of whether these constraints are binding. In contrast, disregarding the issue of measurement will likely result in failed formalization policies because policymakers would not know whether formal work actually pays off, particularly at the lower end of the wage spectrum.

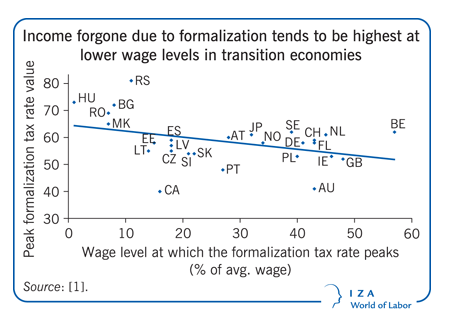

Policies that aim to formalize low-wage workers in transition economies can benefit from synthetic measurements, such as the formalization tax rate (FTR) and the marginal effective tax rate (METR). These measurements show whether formal work pays in the face of taxes and benefits. The FTR and METR provide measures on incentives and disincentives of transiting from informal to formal work and can help policymakers devise reforms of tax and benefit systems. Our research shows that measuring disincentives matters as there is a strong correlation between the FTR and the METR, and the incidence of being informal. Controlling for the characteristics of both the job and the worker, the higher the disincentive measures for formal work, such as the FTR or the METR, the more likely the worker will opt to be informal.

The FTR and the METR also allow for comparisons between countries and over time. In the absence of the FTR or METR, a second best solution could be to calculate the tax wedge at only 33% of the average wage rather than the average wage to better express the situation faced by the majority of low-wage workers. Evidence suggests that this group suffers from high disincentives to accepting formal jobs and this is particularly true for low-paying part-time work. This calls for policy reforms, as formal work does not seem to pay, particularly in this segment of the labor market. Policymakers can use the FTR or METR to help identify shortcomings in a country’s labor tax code and social benefit design. They can also test and compare reform options for the purpose of reducing disincentives to formal work.

This blog is based on the IZA World of Labor note ‘Measuring disincentives to formal work’.

Thank you for choosing to be part of the Jobs and Development community!

Your subscription is now active. The latest blog posts and blog-related announcements will be delivered directly to your email inbox. You may unsubscribe at any time.

The e-mail address: [email] is already subscribed for newsletters.

Join the Conversation