Elephant herd in savanna serengeti panoramic of wild life

Elephant herd in savanna serengeti panoramic of wild life

The coronavirus pandemic has renewed interest in sustainable investing strategies that allow investors to both protect the financial value of their assets and contribute to solutions to global problems such as climate change. These investments have become increasingly mainstream, and now account for more than $39 trillion in the five major global markets, a 34 percent increase over two years, according to the latest trends reported by the Global Sustainable Investment Alliance.

Such investments represent a sizable share of professionally managed assets in each region, ranging from 18 percent in Japan to 63 percent in Australia and New Zealand. How African investors reacting to these trends has been much less well documented. What we do know is that the market for ‘green investments’ across the region remain small. For example, although the labelled bond market reached over $1 trillion U.S. in aggregate issuance in late 2020, less than 0.1% was raised by Sub-Saharan Africa. The African Pension Supervisors Network - in collaboration with the World Bank – recently set out to investigate existing practices and how to incentive changes.

Attracting sustainable investment is a key challenge for the region for several reasons. First, while climate change and associated physical risks will be felt by all countries, some the most severe temperatures are predicted to occur in Sub-Saharan Africa. The region is also directly and indirectly exposed to the transition risks associated with climate change, which is amplified by the dependence of many economies, and jobs, on minerals, energy and mining. In addition, financial sector regulations that are rapidly being rolled out in the European Union and are being harmonized globally will impact all companies that are part of the supply chains that intersect with African countries.

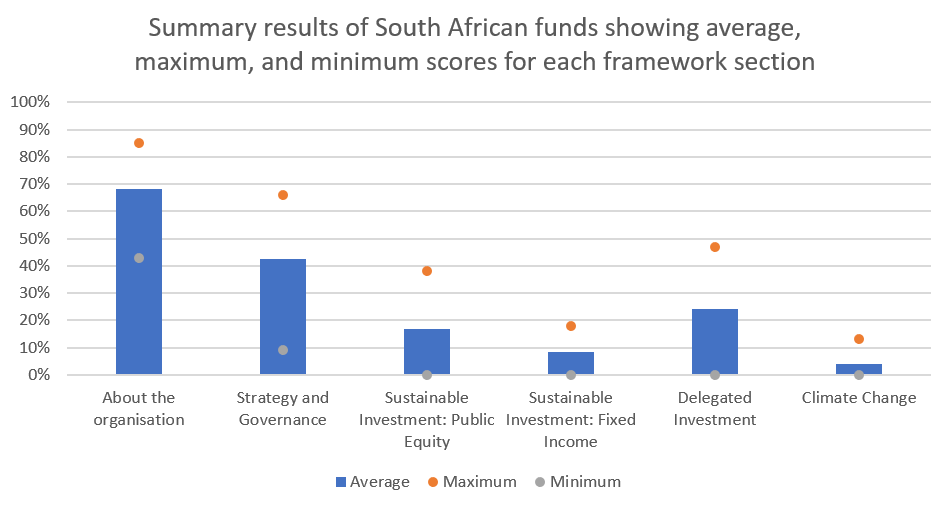

As the main asset owners in the region, the pension and social security funds are at the ‘elephants’ of the local financial markets and could be the catalysts for greening the continent’s financial systems. That’s why we started our search for answers by benchmarking the Environmental, Social and Governance (ESG) reporting practices of a number of the main pension funds in the region, using an assessment developed by the World Bank that has been applied to pension funds globally.

We found that all of the funds provide good disclosure about their organization, their financial performance and strategy – including their assets under management and in many cases their portfolio breakdown. Yet only half of the funds provide information on the importance of sustainability to their investments. They provide limited information on their sustainable investment strategies, and whether they are implemented across their portfolios or in specific asset classes and on delegated investment. The most concerning discovery is that the funds do not appear to disclose any information on their approach to climate change -- except for three that disclose board oversight.

This at least in part reflects the fact that across the region there is only patchy existing sustainable investment regulation and guidance requiring reporting or action from pension funds. South Africa is the furthest along in implementing such rules.

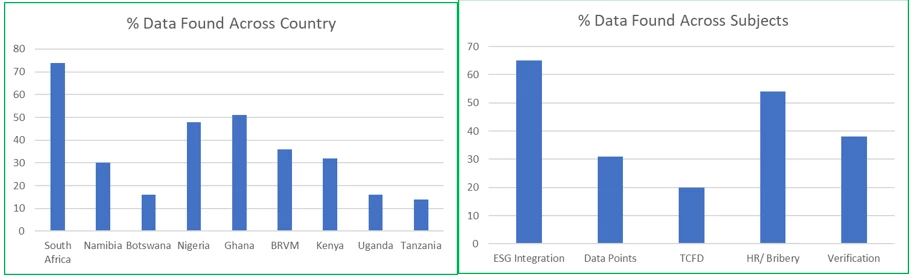

Next, we examined current disclosure practices of issuers in the nine key markets of Sub-Saharan Africa using a checklist developed by UN PRI and used by World Bank for benchmarking exercises globally. Given that the pension funds, the main local investors in the region, are not yet pressing for ESG information, it isn’t surprising that the companies they invest in do not provide extensive sustainability reporting. Even looking at best local practices, investors are sorely challenged to find useful information – with significant differences in consistency and quality between and within regions as well as between companies in the same country. Moreover, what is available could look to some like “green washing,” with long reports that simply repeat a small number of data points. This is despite the fact that public companies in most countries are subject to broader corporate governance requirements.

Percentage of ESG Information Found in Main Markets and in Regions Sub-Saharan Africa

First the region’s pension fund and capital market regulators need to work together to build our green financial regulatory frameworks. At the World Bank we have seen how these frameworks drive changes in investment behaviour though our engagements in countries including Colombia and Malaysia. Given that many of the capital markets across the Africa region are small and still in a development stage, a regional approach may be the best one to take, working together on green taxonomies, green bond guideline and reporting regulations that will align with international practice and reflect local market conditions. This may mean a strong focus on instruments such as transition bonds and guidance on how to integrate ESG factors into non-listed assets.

Second, regulators across the region will need to develop knowledge and experience, to become leaders and not followers of international good practice. That is what our South African colleagues have been doing for many years with their corporate governance codes. Rapid progress can be made by drawing lessons from the experience of global peers. Regional regulators can work with colleagues at international organizations and networks that already have well-developed training programs.

Third we need to build regional champions. We have seen how the large public pension funds not just in Europe and the U.S., but also in Asian markets can be key catalysts for greening domestic financial markets. We need to work with our own “elephants” – the large public and social security funds in the region to lay the foundations for our capital markets to grow sustainably. Institutions such as the Government Employees Pension Fund (GEPF) in South Africa - the largest pension fund in the region and one of the biggest funds in the world, has been leading the way for many years. There are lessons which they can pass on to their regional pension fund peers that, once taught, they will never forget.

Join the Conversation