COVID-19 has put e-commerce at the forefront of retail. Before the pandemic, online shopping was growing at a steady pace of 4.5 percent a year globally. But the retail landscape has deeply changed this year, due mainly to movement restriction measures aimed to protect public health and growing consumer preference to avoid physical stores. Businesses that were able to adapt to digital platforms thrived, in general, while traditional retailers with weak online strategies dwindled, with several prominent ones filing for bankruptcy.

The growth of e-commerce has also contributed to an increase in digital financial services provided to small businesses and consumers. Services such as digital payments, credit, and insurance are increasingly being offered at the point of sale by non-financial companies—a trend referred to as embedded finance. This surge in embedded finance can significantly improve access to finance for small and medium-sized enterprises, reducing costs and increasing efficiency in the digital economy.

In recent years, platforms such as Alibaba, MercadoLibre, Jumia, and Amazon ventured into finance following a similar arc: adding payments facilitation to their platforms and then expanding these capabilities beyond them. Rich data on payments and transactions enabled these companies to build solid credit scoring models and start extending credit and a variety of other financial services to merchants and consumers.

The trend of embedding finance is now expanding beyond e-commerce, shows a recently published report. Digital firms operating in agricultural value chains, ride-hailing platforms, and e-logistics are following a similar pattern and have either introduced financial services or have expressed interest in piloting new financial offerings.

A sudden shift with lasting consequences

The COVID-19 pandemic has heightened several kinds of uncertainty, but one trend has become clear: it has vastly accelerated digital adoption. Unique digital shoppers increased in most countries, with a few exceptions where lockdown policies restricted all types of economic activities, including e-commerce. Data show substantial growth rates in most regions, from the United States to Africa and the Middle East, reshaping consumer behavior and enterprise operations.

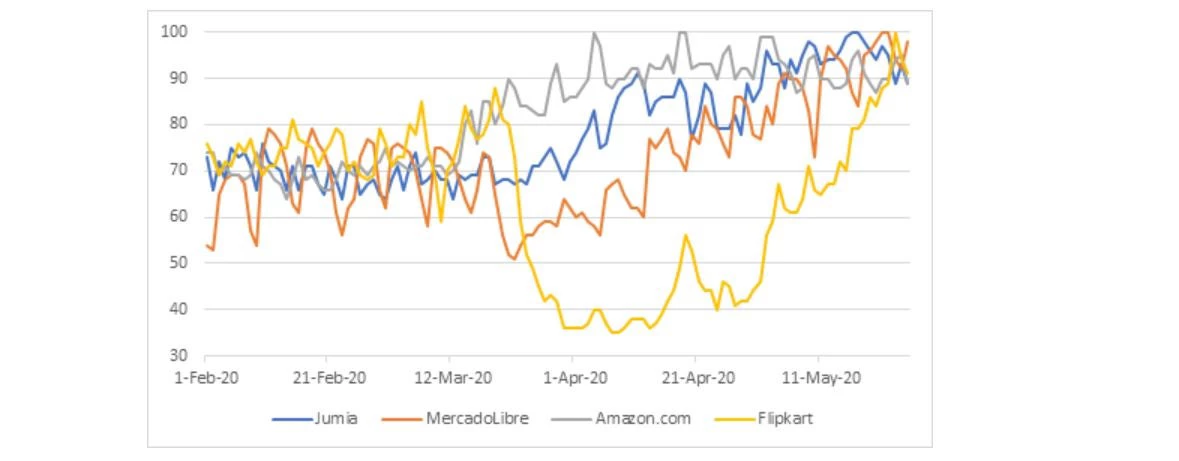

Figure 1: Google Trends for Some of the Largest e-Commerce Platforms between March and May 2020

Online sales are no longer an option, but a necessity for brick-and-mortar businesses. On the consumer side, the COVID-19 crisis has caused a structural shift of demand toward digital commerce that is likely to continue in the years to come. In Latin America, MercadoLibre registered a 100 percent year-on-year increase in demand for essential goods and pharmacy products in the early weeks after the onset of the crisis. In Africa, Jumia registered a fourfold increase in sales of grocery items. Amazon’s third-quarter sales in 2020 rose by 37 percent from a year earlier.

Several new platforms gained relevance in emerging markets of Africa, Asia, and Latin America, adopting new business models and helping the overall landscape to become more competitive. And the crisis might open opportunities for second-generation “niche” platforms that operate in specific market segments that are traditionally excluded from large e-commerce platforms. For example, in Kenya, agricultural value-chain platform Twiga Foods partnered with Jumia Kenya, an e-commerce platform, to sell baskets of assorted fruits and vegetables directly to consumers. In Brazil, an initiative called Compre Local allows customers to locate and buy items from small businesses in their neighborhoods using a simplified payment solution. It is yet to be seen how many of the several initiatives emerging during this period will consolidate to become viable market solutions in the long-term.

An upward trend with a few questions ahead

But the road ahead is not without challenges. Infrastructure for digital payments—including mobile and bank agent networks—are critical for the expansion of e-commerce toward underserved segments. Most platforms saw a surge in the use of digital payments, notably digital wallet—a payment system that allows consumers to make safe, instant transactions without using cash. In Africa, Jumia enforced the use of digital payments in countries such as Kenya, as it temporarily discontinued cash on delivery. Mercado Pago, in Argentina, saw a strong increase both in terms of penetration of digital payments and volume of transactions.

The advantages of digital payments became evident when compared to countries with low mobile-money penetration and/or not well-established agent networks. For example, in Nigeria, some platforms had to discontinue mobile payments because disruptions to the agent network made it difficult for sellers to cash out their payments.

In addition to inadequate infrastructure, uncertainty about regulatory frameworks for the provision of financial services can represent a key risk for e-commerce platforms and needs to be prioritized by regulators in the short term. Because the segment is evolving rapidly, regulators have not yet developed a coherent and simplified framework for embedded finance solutions to operate. Changing requirements linked to payments and credit licenses as well as know-your-customer requirements for sellers and customers need to be addressed for platforms to expand.

It will also be critical to monitor the expansion of e-commerce, as the rapid market developments may draw new lines of inclusion and exclusion to the digital economy. Several e-commerce platforms registered an increase in first-time users since the onset of the COVID-19 crisis, indicating an expansion of the customer base making online purchases. However, low-income households still seem to be out of reach due to lack of basic digital literacy, high costs to access services, and low levels of financial inclusion. Addressing these barriers should be prioritized to make digital economies more inclusive for smaller companies and low-income households.

Join the Conversation