Flags of emerging markets | © shutterstock.com

Flags of emerging markets | © shutterstock.com

In recent years, benign global liquidity conditions and a low interest rate environment in advanced economies have contributed to increased interest among investors in emerging market sovereign debt markets. Local currency bond markets in emerging markets swelled in size following the global financial crisis, more than doubling in nominal terms between 2011 and 2018 (IMF and World Bank 2020).1 Understanding the factors that determine yields on marketable debt can help shape government policy in important ways, including making improvements to the way sovereign debt is issued and managed. A better functioning and more efficient sovereign debt market can, in turn, lead to lower cost of funding for the sovereign in the long run.

Methodological framework

Our recent paper describes a simple and flexible analytical framework for analyzing the determinants of local currency sovereign borrowing costs of a country relative to comparable peer countries.

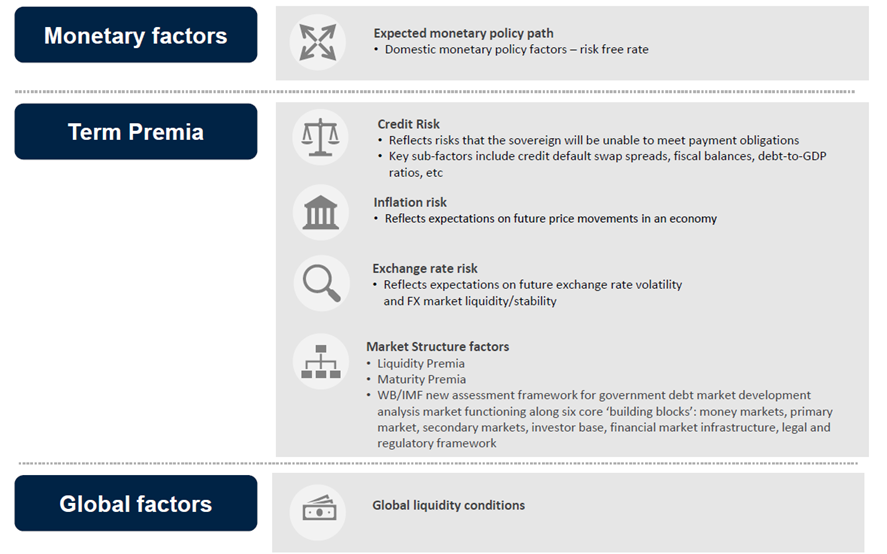

The framework consists of quantitative empirical analysis and qualitative country case studies. The former allows for a quantitative comparison of a country’s sovereign yields with comparable countries in the context of a wide variety of different determinants (figure 1). We explore domestic macroeconomic and financial market factors, external factors, and other political and institutional factors. The latter case studies draw on the reform experiences of selected peer countries in developing their local currency sovereign debt market. The case studies complement the quantitative analysis by looking at important factors that are not easily captured in an empirical analysis for technical reasons.

In our empirical framework, we trace the evolution of excess yields the country of interest pays relative to peers as we consider different specifications/explanatory variables. A panel data set consisting of a reasonably long time-series for all relevant variables for the country of interest and a group of peer countries was assembled.

However, a sizable share of variation in a country’s yields relative to peers may remain unexplained by the quantitative analysis. To address challenges in the domestic government bond market, several emerging markets have undertaken reforms to improve the functioning of their government bond market, aligned with international best practice. These policy experiences and lessons learned offer a variety of different potential policy paths and complement the paper’s empirical analysis.

Figure 1. Potential factors influencing sovereign yields in an emerging market economy

Illustrative example

We present an illustrative application of our analytical framework using Indonesia. Between 2009 and 2019, Indonesia experienced persistently higher yields relative to regional peers and other comparable emerging markets with similar observable market features and credit profiles. We apply this framework to study the possible causes of the excess yields Indonesia pays relative to peers (the “Indonesia premium”) in a panel regression setting using a sample of 11 emerging markets and developing economies (Indonesia and 10 regional (ASEAN-5 and global peers) between 2009Q1 and 2019Q2 and in selected country case studies.

We find that strong macroeconomic fundamentals and a liquid and stable foreign exchange market contribute to lowering the cost of sovereign borrowing. Holding other things constant, a lower policy rate, a perception of lower sovereign default risk (as measured by the sovereign credit default swap spread), and an improvement in the current account balance help reduce the cost of sovereign borrowing. In addition, an improvement in foreign exchange market liquidity and an increase in foreign reserve adequacy are found to help reduce the cost of borrowing.

However, beyond macroeconomic fundamentals, other factors, such as the functioning of the sovereign debt market and its state of development, may also explain part of the “Indonesia premium.” After controlling for all macro-financial variables and foreign currency market variables, the “Indonesia premium” narrows significantly, but it remains positive in most cases (figure 2). This is an indication that other factors could enhance the functioning of government debt markets in Indonesia and contribute to lowering sovereign yields.

Figure 2. The "Indonesia Premium" after controlling for macro and financial market variables

Note: This figure presents the yield premium Indonesia pays relative to peer countries for our sample period before (blue) and after (orange) controlling for potential explanatory factors. A positive number means that Indonesia pays a higher yield. Error bars represent 95% confidence intervals of the point estimates.

We use four qualitative case studies of the experiences of four regional and global peers to complement the quantitative analysis. Previous reform experiences in emerging market peers (Colombia, Hungary, the Philippines, and Turkey in this study) highlight important areas for market development reform, particularly in areas where barriers to progress still remain in the Indonesian government debt market. These include the primary dealers system, issuance policies, competition policies, and depth of the domestic investor base.

Conclusion

Our paper outlines a simple, tractable, and flexible framework for analyzing a country’s local currency sovereign yield relative to a group of peer countries and provides meaningful policy recommendations. This framework allows a country to assess a wide variety of potential determinants of the sovereign cost of borrowing and allows for simple and straightforward comparison with peer countries. The assessment and comparison could point to meaningful policy areas that could be an improvement to support the efficiency and functioning of the local currency sovereign debt market.

We also highlight the importance of combining rigorous empirical analysis with case studies of country-specific experiences. Econometric analysis in a panel setting allows for a rigorous and data-driven assessment of (1) the relevance of a wide variety of potential determinants of sovereign yield, (2) how a country’s yield compares with that of a peer group, and (3) how the determinants and the comparison interact with one other. However, econometric analysis alone is often not enough. This type of analysis is often complicated due to lack of data and identification challenges. Qualitative country case studies provide an invaluable complement to our framework, especially in highlighting factors that are important but not easily captured in an econometric analysis.

Join the Conversation