In January 2019, Olivier Blanchard argued at the annual meeting of the American Economic Association that there were many reasons to doubt the supposed costs of public debt in developed countries, including the United States. Jason Furman and Larry Summers have also stated that it is time to kill off the “debt obsession.” An article in The Economist in May 2019 then questioned whether economists are fundamentally rethinking their ideas about fiscal policy. This debate has had repercussions in resource-rich countries that have suffered from the drop in oil prices since 2017 and are looking for ways to develop their infrastructures and diversify their economies. Many times this is done through expansive fiscal and monetary policies and non-concessional indebtedness in a rather procyclical way. But is this the optimal policy mix for a developing resource-dependent country? We have reasons to believe it is not and offer options to avoid a procyclical bias.

Leaning against the wind is not easy

Designing an optimal monetary and fiscal policy regime for commodity-exporting developing countries is not an easy task. Jeffrey Frankel argues that resource-rich countries should let the currency appreciate in the face of positive terms of trade shocks and depreciate during negative shocks. In addition to that, countries need some sort of nominal anchor and close coordination between monetary and fiscal policies to make sure monetary policy operates around a credible and sustainable fiscal anchor. This kind of coordination is much easier said than done, though, as most often finance ministers and Central Bank governors tend to act in isolation. The main peril resource-rich countries face is that fiscal policy becomes procyclical as this could negatively impact welfare and poverty outcomes.

Recent World Bank reports for the Central African Republic and research papers ( here, here, and here) document the prevalence of procyclical fiscal policies across resource-rich countries, especially in sub-Saharan Africa (SSA). Based on that research, we draw two conclusions and offer an option for countries to avoid the procyclicality trap.

The procyclicality of fiscal policy is high in sub-Saharan Africa

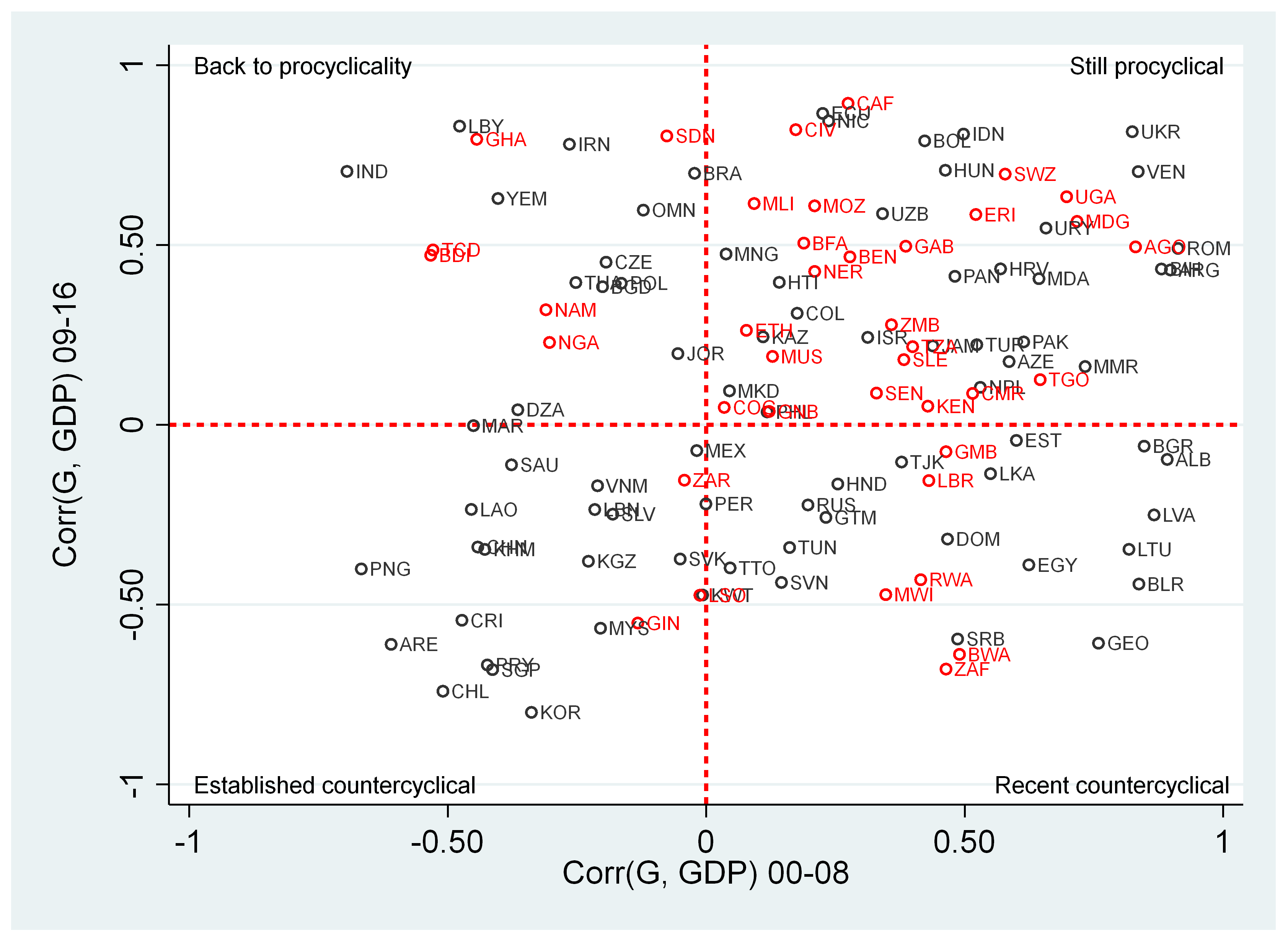

Fiscal policy in developing countries has become slightly less procyclical over the last two decades. Before the 2008-2009 crisis, 64 percent of developing countries had a procyclical fiscal stance, while the proportion fell to 60 percent after the crisis. The procyclicality of fiscal policy is even more pervasive in SSA countries, with only 23 percent of countries (nine out of 39) running a countercyclical fiscal policy. This is relatively low compared to the Latin American countries (LAC) where this proportion is 50 percent. Over time, SSA countries did not change the procyclical nature of their fiscal policy, while Europe and Central Asia (ECA) and LAC reduced their procyclical stance. Countries in the Middle East and North Africa (MENA) region switched from a countercyclical to a procyclical stance, while South and East Asia maintained their countercyclical stance (Figure 1).

Figure 1. Progress in fiscal policy management, 2000-2008 vs. 2009-2016

Source: Herrera, Kouame, and Mandon (2019)

Notes: In red, sub-Saharan African (SSA)

Procyclical fiscal policies are a more common phenomenon in resource-rich countries

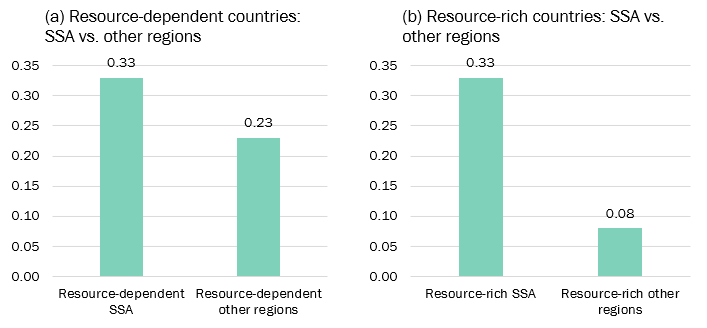

Our research shows that natural resource wealth and dependence limit the likelihood of governments to run countercyclical policy mainly because of low economic diversification and vulnerability to commodity price shocks. However, a countercyclical fiscal policy allows the government to lean against the wind, continue providing goods and services when government revenues drop, guarantee social protection and insurance to citizens, and be more resilient in difficult times. Relatively high fiscal-procyclicality bias in resource-rich countries in SSA adds to the number of challenges facing the continent (Figure 2). For countries such as Angola, the Central African Republic, Nigeria, and the Republic of Congo facing internal security or overhanging debt issues, addressing the procyclicality of the fiscal policy is fundamental, as discussed in our reports.

Figure 2. Procyclicality of fiscal policy in resource-rich and resource-dependent countries

Source: Herrera, Kouame, and Mandon (2019)

Fiscal rules and better transparency can help resource-rich countries avoid procyclical fiscal policies

Our research shows that a combination of top-down and bottom-up approaches might help countries escape the procyclicality bias. Top-down solutions include the adoption of fiscal rules. The use of fiscal rules has increased steadily over time and has been associated with better fiscal/debt outcomes in the countries that have adopted them. There is also evidence that countries that have adopted fiscal rules might experience a positive effect on the risk premia of their sovereign bonds. But of course, the devil is in the details as there are good and not-so-good fiscal rules.

A consensus in the literature is that a good fiscal rule is (a) simple: clearly stated, transparent and with realistic targets for expenditures and debt levels; (b) flexible: it allows for course correction with clear escape clauses and, for resource-rich countries, allows for cyclical adjustments to the business cycle (or booms and busts); and (c) enforceable: there are clear and credible mechanisms to monitor and oversee the implementation of the rule.

Bottom-up solutions are complementary and consist of improving transparency in the implementation of the budget and the fiscal rule. In order to encourage compliance with the fiscal rules, many countries have decided to embed it in the constitution, but that may not be enough. Research by the IMF suggests that formal enforcement mechanisms, such as those that generate sanctions for noncompliance, have also shown limited effectiveness. What seems to work well is to encourage greater transparency in the implementation of the budget and the fiscal rule. This can be done, for example, through the adoption of a truly independent fiscal council that reports annually on the performance of the government in abiding by the fiscal rules. This could provide lawmakers, markets and citizens with the information they need to hold governments accountable.

This article was first published on Brookings.

Join the Conversation