Using smart technology to manage sales: Binta is filling the vegetables she sells on her Weebi tablet. | © Vincent Tremeau / World Bank

Using smart technology to manage sales: Binta is filling the vegetables she sells on her Weebi tablet. | © Vincent Tremeau / World Bank

Having a financial account is essential for adults to save, borrow, make payments, and manage unexpected expenses. However, financial products come with risks, especially for those with limited financial knowledge or living in countries with poor consumer protection systems. Inexperienced account owners are vulnerable to fraud, over-indebtedness, and misunderstandings about account terms and fee structures.

While increasing account ownership among unbanked individuals is a necessary first step towards expanding financial inclusion, it is not enough to ensure they benefit from financial access. They need to be able to use their accounts safely and to their benefit. Unfortunately, many unbanked and underbanked adults lack the education or exposure that gives them financial experience, making the benefits of financial access uncertain.

So, how can policymakers and advocates increase the benefits of financial access? The Global Findex team has answered that question in a recent paper on the role of financial education on financial account adoption and usage. In it, we examined who the unbanked and underbanked are, their barriers to account ownership, and the effect that improving financial ability can have for them. In this blog, we offer an overview of the findings.

The Unbanked are more likely to be women, poor, and less educated adults

On recent trips to multiple countries in Africa and Asia, the Global Findex team conducted qualitative surveys to assess whether people can perform financial transactions independently, without help from a family member, friend, or an agent. Many respondents, particularly women who receive government payments, reported that they rely on family members or friends to help them with financial transactions. Those who sought help from bank agents often had to pay added fees or even side payments (i.e., unofficial fees) to such agents. In Sub-Saharan Africa, mobile money users reported receiving scam calls asking for their account PIN codes. If the recipient shares their account information and is defrauded, they have limited recourse.

While these findings are qualitative and limited in scale, they are consistent with results from the Global Findex 2021. The most recent round of Findex data found that 1.4 billion, or 24 percent of adults worldwide, remained unbanked. This is despite a 50 percent increase in account ownership over the decade.

Most unbanked adults are women, live in the poorest 40% of households by income, and/or have a primary education or less. These factors individually and collectively point to the need for consumer-friendly product design and robust consumer safeguards to ensure that the unbanked benefit from financial access.

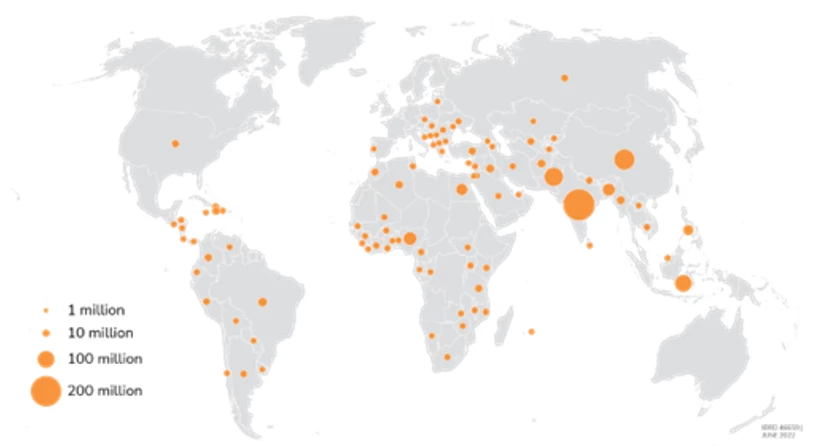

Figure 1: Adults without an account, 2021

Source: Global Findex Database 2021.

Note: Data are not displayed for economies in which the share of adults without an account is 5 percent or less, or for economies in which no data were available.

The Global Findex team found that 64 percent of unbanked adults would not be able to use an account without help if they were to open one. In some countries, such as Pakistan and South Sudan, this number rose to as high as 80 percent. Unbanked women in developing countries were 10 percentage points more likely than unbanked men to say they would need help.

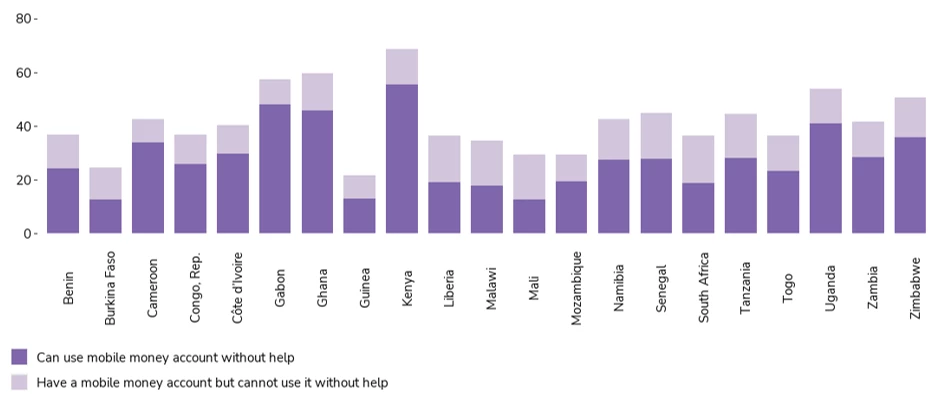

Improved financial literacy and capability could motivate and enable the safe and beneficial use of financial services, not just for unbanked adults but also for some banked adults. In Sub-Saharan Africa, one-third of mobile money account holders need help from a family member or mobile money agent to use their accounts. This lack of independence may make some banked adults more vulnerable to exploitation or to misunderstanding their account rules. It could also explain why one in five wage recipients in developing countries who receive their money into a financial institution account incur unexpected fees.

Figure 2: Adults with a mobile money account, 2021

There are 430 million inactive account holders worldwide, known as the underbanked, who have accounts but do not use them, limiting the benefits they could enjoy. Most inactive account holders live in India, and the top reasons for not using their accounts include distance to financial institutions, lack of trust in financial institutions, and not having a need for an account. This highlights that simply having an account is not enough to encourage use.

How do we address the challenge of financial confidence for banked, unbanked, and underbanked adults?

Without adequate financial education and consumer safeguards, low-income individuals who lack financial experience may be unable to reap the full benefits of owning an account and may become vulnerable to fraud, discrimination, and financial abuse. Financial education can help mitigate some of these potential negative consequences, but consumer safeguards are crucial for ensuring customer safety and fostering confidence in the broader financial system.

‘Mystery shopping’ exercises have revealed that inexperienced customers received less information on account costs and were rarely offered the cheapest product. This is because staff members are incentivized to sell more expensive products, which puts consumers at risk. To mitigate this risk, financial institutions should align employee incentives with consumer protection requirements. Additionally, presenting clear and concise information about credit and savings products can help consumers make effective financial choices. For example, a study conducted in Mexico and Peru, found that when consumers were presented consumers with clear and concise information about financial products, the consumers were more likely to choose a product that was right for their needs. Allowing users to check their account balances in real-time using their phone or the internet also builds trust and increases usage.

Financial regulators can also play a role in creating better conditions for consumers by filling key information gaps and requiring financial institutions to provide customers with complete information about all account options available to them. By ensuring transparency from financial institutions, regulators can help individuals make informed and optimal decisions about their financial accounts and achieve financially inclusion.

Join the Conversation