A female conducting a transaction using her smart phone | © shutterstock.com

A female conducting a transaction using her smart phone | © shutterstock.com

The latest edition of the Global Findex shows that account ownership has grown across the globe and three out of four adults worldwide today have a financial account. Yet 1.4 billion adults remain unbanked. How can policies and products help bring more unbanked adults into the financial system?

Insights from the Global Findex Database 2021 about the ways in which account owners use their account for payments, saving, and borrowing—and how these financial services interact as part of a broader financial ecosystem—reveal a key opportunity for expanding financial inclusion. Namely, by leveraging payments, one of the financial transactions that unbanked adults already make.

Payments into an account serve as a gateway for using other financial services

People who receive payments into an account are more likely than non-recipients to use their accounts to store money for cash management, make payments, and save and borrow formally.

Global Findex 2021 data show that in developing economies, 20 percent of adults received a wage payment—from the private sector or from the government—into an account (figure 1). Almost all (91 percent) of those recipients also made a digital payment from their account. At the same time, about 70 percent of those who received a payment into their account also used their account to store money for cash management, about half used their account to save money and about half to borrow money.

The relationship between receiving a digital payment and the use of other financial services suggests that once money is received into an account, it is becoming easier for account owners to keep the money there until it is needed—and then make a payment from the account. Similarly, we know from behavioral studies that once money is in an account, it is relatively easy to keep it there as savings. Receiving a payment into an account might also make it easier to get approved for formal credit if the payment can be used to document a regular income stream.

Source: Global Findex Database 2021.

Note: Usages are shown as percentages of the 20 percent of adults receiving a private or public sector wage payment into an account.

Digitalizing cash payments is a proven way to increase account ownership

Millions of unbanked adults still receive regular cash payments from employers and the government. Global Findex data suggest that shifting some of these payments into an account could expand financial inclusion among the 1.4 billion unbanked adults—and potentially lead to the broader use of financial services. Digitalizing such payments is a proven way to increase account ownership. In developing economies, 39 percent of adults—or 57 percent of those with a financial institution account—opened their first account at a financial institution specifically to receive a wage payment or to receive money from the government. Researchers also show that digitalizing wage payments can encourage workers to save and improve financial resilience and financial savviness.

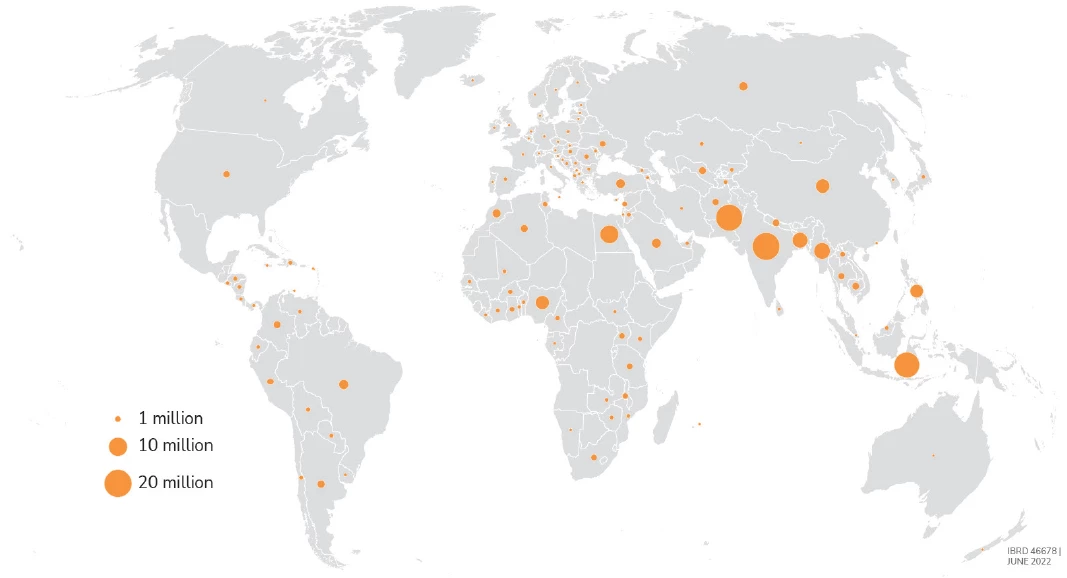

Global Findex 2021 data find that 165 million unbanked adults received private sector wage payments in cash only (map 1). Shifting wage payments and other types of payments (such as payments for the sale of agricultural products) from cash into accounts can serve as an entry point to the formal financial system.

Map: Globally, about 165 million adults received private sector wages in cash

Adults without an account receiving private sector wages in the past year in cash only, 2021

Source: Global Findex Database 2021.

Note: Data are not displayed for economies where the share of adults without an account was 5 percent or less or the share receiving private sector wages was 10 percent or less or for economies for which no data are available.

But Global Findex data also find that one in five adults in developing economies who receive a wage payment into a financial institution account, like a bank or similar institution, paid unexpected fees on the transaction. The challenge for businesses and governments is to ensure that digital payments are safer, more affordable, and more transparent than cash-based alternatives—so that workers can use their accounts to improve their financial wellbeing

Join the Conversation