Prices for industrial commodities are forecast to level off in 2018 after big increases this year, the World Bank’s October

Commodity Markets Outlook says.

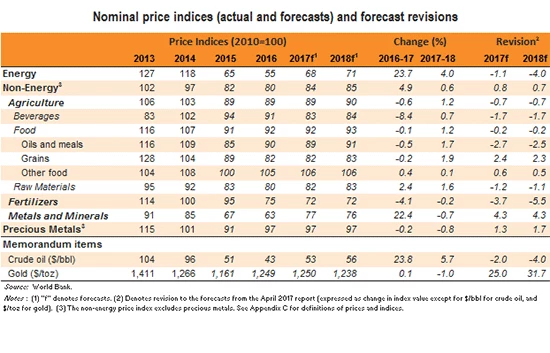

Oil prices are expected to rise to an average of $56 per barrel in the coming year from an average of $53/bbl in 2017 as a result of steadily growing demand, production cuts among oil exporters, and stabilizing U.S. shale oil production.

The oil price forecast is a small downward revision from the April outlook and is subject to risks. Supplies from producers such as Libya, Nigeria, and Venezuela could be volatile. Members of the Organization of the Petroleum Exporting Countries (OPEC) and other producers could follow up their production limiting agreement of last year by deciding to cut production further, maintaining upward pressure on prices. At the same time, failure to renew the existing agreement could drive prices down, as could higher production from the U.S. shale oil industry, which has reduced its operating costs substantially.

More broadly, prices for energy commodities—which also include natural gas and coal—are forecast to climb 4 percent in 2018 after a 28 percent leap this year. Natural gas prices are expected to rise 3 percent in 2018, while coal prices are seen retreating following a spike of nearly 30 percent in 2017. China’s environmental policies are anticipated to be a key factor determining future trends in coal markets.

China will similarly play an important role in the evolution of metals prices, which should stabilize as a group in 2018 as a correction in iron ore prices is offset by gains in other base metals. China consumes more than half of the world’s metals.

Iron ore prices are forecast to tumble 10 percent in the coming year while tight supply should push up prices for base metals including lead, nickel and zinc. Downside risks to the forecast include slower-than-anticipated demand from China, or an easing of production restrictions on China’s heavy industries.

Gold prices are anticipated to ease next year on expectations of higher U.S. interest rates.

Agriculture prices are seen edging up in 2018 due to lower planted area, with grain and oils and meals prices rising marginally. Agricultural commodity markets are well-supplied. Indeed, stocks-to-use ratios, a measure of how well supplied markets are, have reached multi-year highs for some grains.

However, favorable weather patterns, well-supplied global food markets, and relatively low world prices do not necessarily imply ample food availability everywhere. Drought conditions that are by some accounts the worst in 60 years have caused crops failures in parts of Ethiopia, Somalia and Kenya and led to severe food shortages. Conflicts in South Sudan, Yemen and Nigeria have driven millions of people from their homes and left millions more in need of emergency food.

Oil prices are expected to rise to an average of $56 per barrel in the coming year from an average of $53/bbl in 2017 as a result of steadily growing demand, production cuts among oil exporters, and stabilizing U.S. shale oil production.

The oil price forecast is a small downward revision from the April outlook and is subject to risks. Supplies from producers such as Libya, Nigeria, and Venezuela could be volatile. Members of the Organization of the Petroleum Exporting Countries (OPEC) and other producers could follow up their production limiting agreement of last year by deciding to cut production further, maintaining upward pressure on prices. At the same time, failure to renew the existing agreement could drive prices down, as could higher production from the U.S. shale oil industry, which has reduced its operating costs substantially.

Commodity price indexes, monthly

More broadly, prices for energy commodities—which also include natural gas and coal—are forecast to climb 4 percent in 2018 after a 28 percent leap this year. Natural gas prices are expected to rise 3 percent in 2018, while coal prices are seen retreating following a spike of nearly 30 percent in 2017. China’s environmental policies are anticipated to be a key factor determining future trends in coal markets.

China will similarly play an important role in the evolution of metals prices, which should stabilize as a group in 2018 as a correction in iron ore prices is offset by gains in other base metals. China consumes more than half of the world’s metals.

Iron ore prices are forecast to tumble 10 percent in the coming year while tight supply should push up prices for base metals including lead, nickel and zinc. Downside risks to the forecast include slower-than-anticipated demand from China, or an easing of production restrictions on China’s heavy industries.

Gold prices are anticipated to ease next year on expectations of higher U.S. interest rates.

Agriculture prices are seen edging up in 2018 due to lower planted area, with grain and oils and meals prices rising marginally. Agricultural commodity markets are well-supplied. Indeed, stocks-to-use ratios, a measure of how well supplied markets are, have reached multi-year highs for some grains.

However, favorable weather patterns, well-supplied global food markets, and relatively low world prices do not necessarily imply ample food availability everywhere. Drought conditions that are by some accounts the worst in 60 years have caused crops failures in parts of Ethiopia, Somalia and Kenya and led to severe food shortages. Conflicts in South Sudan, Yemen and Nigeria have driven millions of people from their homes and left millions more in need of emergency food.

Join the Conversation