When the Plantagenet kings ruled England (1154-1485), their primary means of securing wealth, prestige, and power was through territorial conquest. Fighting endless wars in France and dispatching armies as far as Jerusalem, the crown often had to finance foreign adventures through taxation -- sometimes crushing taxation – of subjects. The illegitimacy of such taxation only intensified the recurrent threat of domestic revolt. And through their demands for more accountable and inclusive governance, the English nobility succeeded, albeit with much blood shed over a span of centuries, to establish institutions and public policies conducive to economic development.

This history illustrates a fact relevant to today’s efforts to reduce poverty: tax policies can act as a form of “extraction,” which – like all extractive policies and institutions – severely inhibits inclusive economic growth (see Acemoglu and Robinson 2012). Particularly if fiscal management is weak or corrupt and public accountability low, such policies can be a tool through which unaccountable interests appropriate the gains from others’ economic activity. And even where fiscal governance is strong, if onerous, taxation can make it extremely difficult for a country’s entrepreneurs to create value – invest, innovative, and create jobs – and for its citizens to prosper.

Take the case of Sub-Saharan Africa, where the tax burden on businesses is high compared to other regions of the world. According to Doing Business’s Paying Taxes, the direct tax burden on businesses in Sub-Saharan Africa (SSA) is 47 percent of profits versus 40 percent for the world as a whole. And the small West African nation of Togo is no exception. A recent Systematic Country Diagnostic (SCD) found that Togo’s taxation of businesses (including agriculture) is among the most binding constraints to poverty reduction, along with weak governance and poor health care, given the high toll it exacts on private investment, entrepreneurship, agricultural productivity, and job creation.

Not all of the Sub-Saharan African countries levy high taxes on businesses, however, with countries such as Lesotho, Mauritius, Seychelles, and Botswana showing much lower levels. Although an imperfect indicator, Paying Taxes suggests that direct taxation of business activity is particularly high in former French colonies in Sub-Saharan Africa -- 64 percent of profits. Comoros, Cote d’Ivoire, Benin, Cameroon, the Republic of Congo, Senegal, Guinea, Chad, Central African Republic, and Mauritania all rank worse than Togo on this indicator. Taxation is also high in Algeria (at 72.7 percent of profits) and Tunisia (59.9 per cent). France itself sets a tax burden of 62 percent, suggesting that there may be some process of policy transmission between countries with historical or language ties.

To be sure, public revenues are fundamentally important for economic development, and taxes are needed to fund basic services such as education, healthcare, and road construction. In some countries, high rates of taxation of business may simply reflect the populations’ demand for more public investments, services, and transfers.

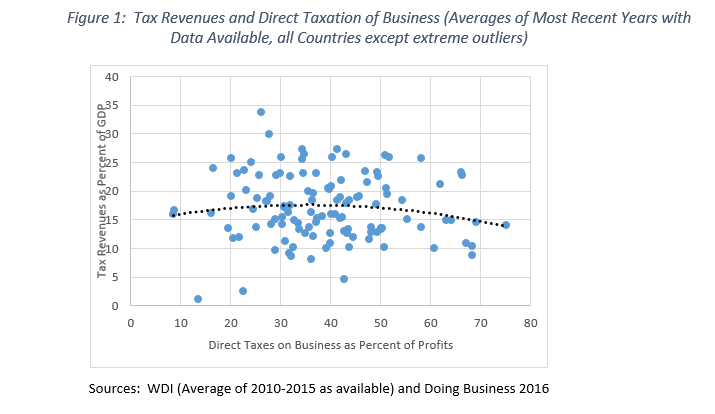

But the available indicators suggest that higher taxation of business does not tend to translate into greater fiscal resources to fund such public goods. As shown in Figure 1, for the world as a whole (including rich countries) direct taxation of business exceeding 35 percent of profits is associated with lower tax revenues as a percent of GDP. Moreover, when one excludes the world’s rich countries (where taxes are more difficult to evade) the relationship between tax rates and revenues is negative (Figure 2.) While this relationship does not demonstrate causality, the cross country data are not consistent with high tax rates representing the mere translation into policy of citizen preferences. Just as in Plantagenet England, high taxation can be a form of extraction, but carries no guarantee of improving governance over time (the topic of my next blog post).

What does this mean for developing poverty reduction strategies? First, policy analysts should look objectively at the relationships between governance, taxation, and economic outcomes. Personal views, possibly shaped by the experience of rich countries with more accountable governance, may create blind spots. Taxation of businesses seems especially ripe for ideological or cultural biases. Instead, policy advisors should consider how public expenditures would be financed before advocating increasing them. They should investigate tax policies as part of any attempt to diagnose key constraints to poverty reduction. And they should ask how likely it is that increased fiscal resources will be well spent in the governance context of the country, whether citizens and entrepreneurs have a voice in setting tax and expenditure policies, and whether taxes are choking off private investment and productivity growth – thereby hampering progress toward the goals of ending extreme poverty and boosting the incomes of the bottom 40 percent.

Join the Conversation