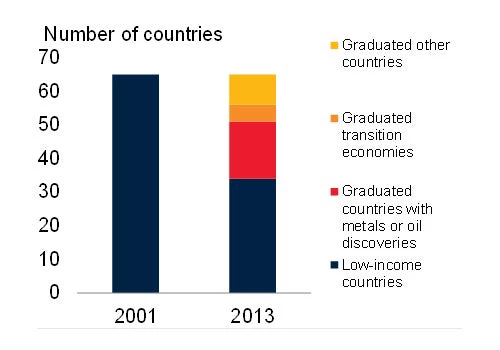

The number of low-income countries has dropped by nearly half since 2001, following the graduation of mainly mineral exporting and transition economies in Sub-Saharan Africa and Europe and Central Asia to middle-income status.

Much has recently been written about “

middle-income traps”. However, the fact that many

low-income countries have joined the ranks of middle-income ones has garnered less attention. Since 2001, the total number of low-income countries has nearly halved to 34, as some 31 “graduated” to middle-income status (Figure 1).

Figure 1. Graduation to middle-income status, 2001-2013

Source: World Bank.

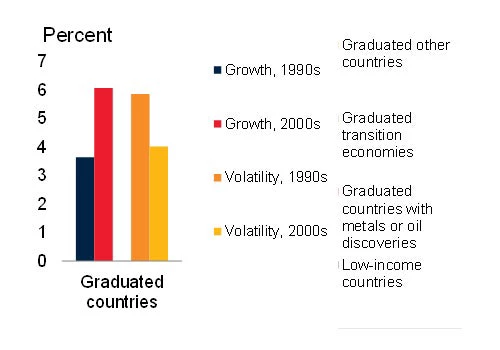

Moreover, as the January 2015 edition of

Global Economic Prospects documents, graduation has been accompanied by a marked acceleration in growth, and also a decline in volatility (Figure 2) that has coincided with a decline in the

frequency of growth collapses that had undermined poverty reduction in earlier decades. Average headcount poverty ratios ($1.25 PPP basis) meanwhile have fallen from just under 40 percent in 2000 to about 23 percent by the latest count.

Figure 2. Growth and volatility

Source: World Bank. IMF. Growth is calculated as the average for the period.

Volatility refers to the standard deviation of GDP growth over the period.

What are the factors that have underpinned this move into middle-income categories?

In more than half of graduating countries, graduation followed new discoveries or intensified exploitation of metal and oil reserves. Rising demand from China and strong global growth supported high commodity prices and spurred greater exploration for energy and metal resources and investment in the natural resource sector. This, in turn, supported graduation to middle-income status in countries such as Mongolia, Timor Leste, Indonesia, Ghana, Cameroon and Mauritania.

In addition, several economies in Europe and Central Asia had seen per capita incomes fall precipitously in the 1990s during deep “transition” recessions. However, the subsequent rebound in growth helped push per capita income levels back above middle-income thresholds in Armenia, Kyrgyz Republic, Moldova and Azerbaijan.

Finally, some countries reaped growth dividends from earlier structural reforms (India, Indonesia), and political and economic reforms (Vietnam). Several also benefited from greater political stability or an easing of conflict that allowed faster growth during the 2000s (Pakistan, Solomon Islands).

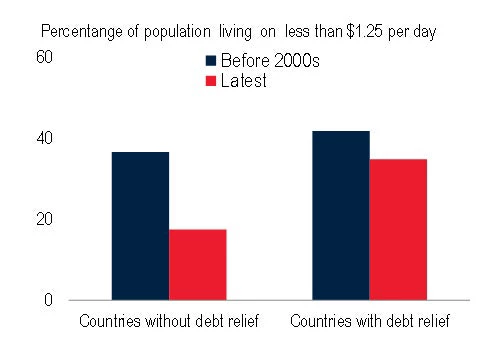

One-third of graduating countries received debt relief between 2000 and 2014 under the Heavily Indebted Poor Countries (HIPC) Initiative, Multilateral Debt Relief Initiative (MDRI), or bilateral initiatives. Although it is unclear to what extent falling debt burdens were a contributing factor in graduation, many have managed to put the increased fiscal space to good use. On average, expenditures allocated for poverty reduction have increased by 3.9 percent of GDP, although as the

Global Economic Prospects report shows, poverty has been slower to decline in graduating countries with debt relief compared to those without (Figure 3).

Figure 3. Decline in poverty ratios after graduation

Source: World Bank. IMF

Not all graduating countries have seen improvements across the board. While per capita incomes may be higher, a key stylized fact documented in the

Global Economic Prospects report is that governance in graduating countries with new resource discoveries or exploitation, was on average substantially weaker than in those without natural resources and remained broadly on par with low-income countries that did not graduate.

Who got left behind and what is their outlook?

Today’s low-income countries are typically agricultural economies. Three-quarters are in Sub-Saharan Africa, where challenging climatic conditions at times strain activity in predominantly subsistence economies. On average, agriculture accounts for about 25 percent of GDP in low-income countries. In many cases, exports are dominated by agricultural commodities, especially coffee and tea.

Many low-income countries are also heavily dependent on remittances to support consumption and investment. On average, remittances accounted for almost 6 percent of GDP in low-income countries in 2013, significantly more than FDI. About half of low-income countries are fragile, and in some – Guinea, Liberia, and Sierra Leone – lack of adequate public health care services has facilitated the spread of

Ebola.

This has taken a heavy human toll, disrupted activity and trade, and shaved 1-3 percentage points off growth in these countries.

In contrast to middle-income countries, economic activity in low-income countries strengthened in 2014 on the back of rising public investment, significant expansion of service sectors and solid harvests. Improving security or political conditions in a number of conflict countries, e.g. in Myanmar, Central African Republic and Mali have also helped. Several countries have taken advantage of benign international financing conditions to issue sovereign bonds in international markets—for some such as Kenya, the first issuance in many years.

For low-income countries as a whole, growth is expected to remain robust, around 6 percent, in 2015-17 supported by strong government consumption and investment growth. East Africa is emerging as the “new frontier” for oil and gas discoveries. Despite soft commodity prices in the near-term, these new discoveries and/or intensified mineral exploitation could help several (Tanzania, Kenya, Mozambique, Uganda) graduate in the medium term, as has happened in other resource rich low-income countries before.

That said, continued growth in today’s low-income countries is contingent upon improvement in institutions and public financial management and increased investment in education and infrastructure, which will expand supply potential and help diversify economies.

Get updates from Let's Talk Development

Thank you for choosing to be part of the Let's Talk Development community!

Your subscription is now active. The latest blog posts and blog-related announcements will be delivered directly to your email inbox. You may unsubscribe at any time.

The e-mail address: [email] is already subscribed for newsletters.

Join the Conversation