International trade has undergone a radical transformation in the past decades as production processes have fragmented along cross-border value chains. The Brazilian economy has remained on the fringes of this production revolution, maintaining a very high density of local supply chains. This article calls attention to the rising opportunity costs incurred by such option taken by the country.

Moving Tectonic Plates under the Global Economic Geography

In recent decades, international trade has gone through a revolution, with the wide extension of the organization of production in the form of cross-border value chains. This extension was a result of the reduction of tariff and non-tariff barriers, the incorporation of large swaths of workers in the global market economy in Asia and Central Europe, and technological innovations that allowed modularization and geographic distribution of production stages in a growing universe of activities. International trade has grown faster than world GDP and, within the former, the sales of intermediate products has risen faster than the sale of final goods.

The geography of industrial production has changed dramatically, with unskilled labor-intensive sectors moving out of advanced economies rapidly. Although the "hollowing out" of such jobs in advanced economies may have been, to a greater or lesser extent, determined by biases in trends of technological progress, the transfer of unskilled labor-intensive segments of supply chains has been part of the explanation. On the other side of such transfers, low-income countries have experienced rapid economic growth processes stemming from the structural transformation that has resulted from the large-scale migration of workers from subsistence to modern tradable activities.

Sharp changes in relative prices in the global economy have accompanied this process. While labor prices fell – as well as prices of manufactured products, according to their labor intensiveness - prices rose for natural resource-intensive goods, following an increase in demand coming from economically-growing low-income areas.

The logic of value chains was also extended to other sectors beyond manufacturing. Producers are opting for less self-sufficient, in-house capacities, choosing to sub-contract activities that are not essential to their business. This is also one reason for the expansion of services in GDP accounting in recent decades. Commodity chains have increasingly relied on sophisticated services both upstream and downstream. The content of services embedded in industrial products has also increased. Additionally, technological innovations have increased the marketability of various services, as expressed in the growth of international trade in services.

The opportunities and challenges of the international industrial division of labor are reconfigured in this new world of cross-border value chains. For low-income economies, one can say that it has become relatively easier - especially for small countries – to increase their local industrial production, since joining the market through labor-intensive segments of existing chains allows them to circumvent the limits of (a lack of) scale and sophistication in local markets. Nevertheless, such entry is volatile and can easily be undone and relocated soon after any adverse signal comes out. This process of entry – with easy exit - corresponds to a window of opportunity for local accumulation of skills and a leap forward.

For high- and middle-income economies, in turn, it has become increasingly difficult to maintain competitiveness in those segments. It should also be noted though that some technological trajectories currently in early stage – such as 3D printing - may require the substitution of qualified for unqualified labor in a wide range of segments of existing chains, partly reversing the spatial dynamics described above.

Middle-income economies are also facing a new landscape in other aspects. On the one hand, technological spillovers, productivity increases, and wider market access are now facilitated via entry at points that require intermediate sophistication levels within existing value chains. On the other, the consolidation of existing value chains raises the stakes in terms of the competition for core positions. For consolidated and mature branches, creating new chains and challenging established ones is the only alternative.

Foreign Trade Statistics and Value-Added Trade

The statistics of exports and imports no longer serve as a gauge of how countries’ foreign trade affects their allocation of factors of production. With the fragmentation of production systems and the back-and-forth cross-border movement of products at intermediate stages, one cannot ignore multiple accounting, either within a sector or in other branch in which they serve as inputs.

Only recently have data on sector-specific added-value country exports started to become available, thanks to a joint OECD-WTO initiative, (OECD/WTO, 2013) where one can find information on sector-specific gross exports minus imports in the same industry and from other lines of the input-output matrix of a country. Results are often very different from those visualized with statistics of gross exports and imports (Canuto, 2013).

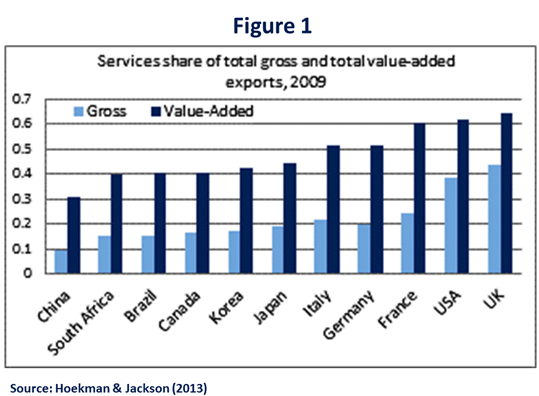

For example, the database of trade in added value of OECD/WTO reveals that once the content of services embedded in other branches is taken into account, international trade volumes are much larger than the 25% suggested by gross trade figures - see Figure 1. They account for over fifty percent of total exports in countries like the US, UK, France, Germany and Italy and, perhaps surprisingly, almost a third in China. In fact, as shown in Hoekman & Jackson (2013), domestic and imported services appear embedded in the various branches of manufacturing, mining and agricultural sectors. It follows that the quality of services available to a country’s industrial sector, whether domestic or imported, greatly affects the country’s competitiveness.

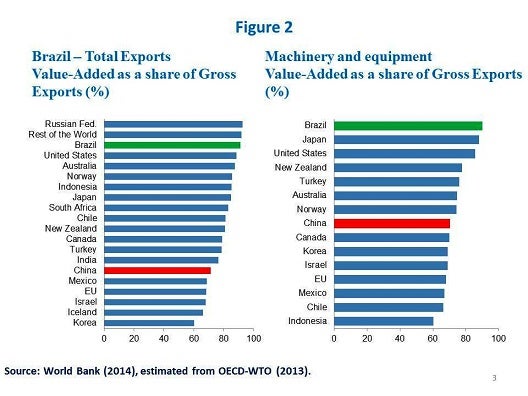

Value-added trade statistics also give a view of how Brazil maintains a level of density in its chains of domestic industrial production above what one would expect in the case of a middle-income country. Figure 2 shows ratios of value added (VA) relative to gross exports (X) in various countries. China provides a particularly telling comparison point against Brazil. While the weight of commodities partly explains why the ratio is so high in the case of the total export bill (left side), the index is also very high in most manufacturing branches, as illustrated on the right side of Figure 2 in the case of machinery and equipment (World Bank, 2014).

Brazil has remained outside the process of cross-border production fragmentation. There are few exceptions, like Embraer, which operates in the center of its own global value chain. The automotive Mercosur regional network also seems to escape the rule, but it is in fact the extension of a chain with a low degree of integration with the rest of the world. High coefficients of VA to X demonstrate local levels of production far above what one would expect for a middle-income economy with average levels of technological sophistication.

Opportunity Costs of the High Density of Brazilian Production Chains

Geographic distances from advanced economies - reduced but not completely annulled by revolutions in transport and communications - partially explain why Brazil's production-chain density remains well above its notional counterfactual. After all, in many branches, cross-border production chains are regional and focus on dynamic markets of high-income countries (Asia, Europe and North America).

However, the Brazilian deviation from its notional density levels also reflects trade and local-content policies, which have remained more prevalent than in most of Brazil’s peer countries including China (World Bank, 2014). Likewise, Brazil’s precarious logistics and high transaction costs in trading across borders are incompatible with the logic of cross-border value chains.

Eliminating these factors would reduce the deviation between actual and notional densities, leading to a corresponding closure of less competitive production chain segments and a rise in import substitution. On the other hand, the businesses left standing would be more competitive and final products would have lower production costs and/or higher quality. Furthermore, in dynamic terms, such as when the adjustment implications of changing chain densities unfold, gains would increase by dint of greater technological spillovers and market extension relative to the current scenario.

The technological dynamics and cost reductions in the global economy due to the increase in value-chain fragmentation have been significant, increasing the opportunity cost of the ongoing gap between actual and notional production densities. For example, despite rising trade barriers, Mercosur’s coefficient of imports from China keeps moving up. Private investors, in turn, tend to shun commitment to production lines that they see as survivors only in conditions of permanent protection.

In an economy with labor shortages and aspirations of rising worker purchasing power, productive activities would be strengthened by the availability of cheaper local consumer goods and equipment, as wage and investment costs would be lower. That would facilitate the creation of global value chains with a core in the country in natural resource-associated industries, where there clearly exists a greater scope.

Of course, public policy support remains essential. However, this support should be more horizontal in nature, rather than further encouraging the ongoing high density of production chains

Join the Conversation