នៅក្នុងប្រទេសកម្ពុជា មនុស្សពេញវ័យត្រឹមតែ 18% ប៉ុណ្ណោះដែលមានគណនីធនាគារ ចំណែកឯ 85% នៃ កម្មករកាត់ដេរជាស្ត្រី ប្រាក់ឈ្នួលក្នុងវិស័យកាត់ដេរភាគច្រើននៅតែបន្តទូទាត់ជាសាច់ប្រាក់។

នៅក្នុងប្រទេសកម្ពុជា មនុស្សពេញវ័យត្រឹមតែ 18% ប៉ុណ្ណោះដែលមានគណនីធនាគារ ចំណែកឯ 85% នៃ កម្មករកាត់ដេរជាស្ត្រី ប្រាក់ឈ្នួលក្នុងវិស័យកាត់ដេរភាគច្រើននៅតែបន្តទូទាត់ជាសាច់ប្រាក់។

The world is moving to digital payments. They are faster, more secure, more transparent and more efficient than cash. Digital payments can support small and medium enterprises (SMEs) and empower women and youth. The COVID-19 pandemic has accelerated the shift toward paying digitally and demonstrated clear benefits beyond cost and efficiency: by minimizing human interactions during money exchanges, reducing travel and keeping commercial establishments less crowded, and managing health risks.

The case for digital payment of wages in the workplace is strong. For example, Bangladesh’s ready-made garment sector increased its adoption of wage digitization over the last decade and the business benefits of digital payments were clearly demonstrated, including lowering the costs and security risks of disbursing cash on payday. Adopting digital wage payments also expanded access to formal financial services for workers, especially women, and increased the use of accounts for savings and sending remittances, especially when partnered with financial capability training and ongoing support.

In Cambodia, where only 18% of adults have a bank account and 85% of garment workers are women, most garment sector wages continue to be paid in cash. To better understand the opportunity for wage digitization in Cambodia, IFC partnered with Business for Social Responsibility’s (BSR) HERproject, under the IFC/ILO Better Work partnership, and in collaboration with Microfinance Opportunities. Starting in November 2020, we studied the opportunities and challenges to digitize Cambodia’s garment factory wages through interviews and surveys with over 400 workers and managers from more than 100 factories. Half of the factories we selected to interview pay workers digitally and the other half pay workers in cash.

The findings were clear. Digital wages can bring efficiencies in the garment supply chain that benefit both employers and workers : (i) Digital payments can lower costs for factory owners; (ii) Workers, especially women, benefit from an increased use of digital financial services; and (iii) Cambodia has a solid technological infrastructure base for financial service providers to offer digital wages.

More specifically, the study found that:

i. Digital payments can lower costs for factory owners

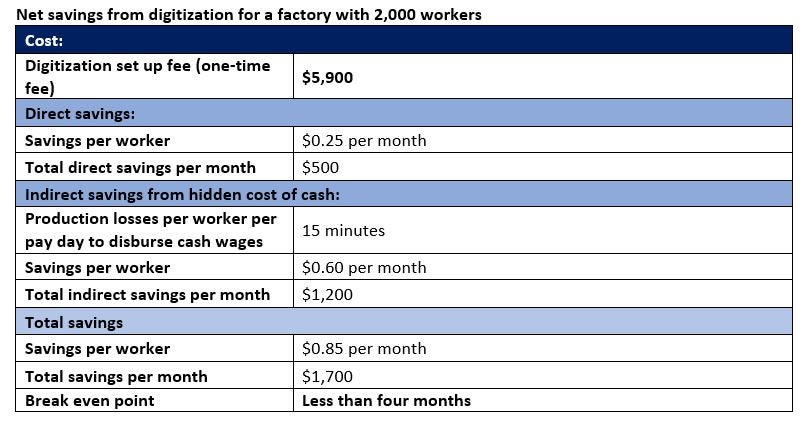

Cash wage payments are time-consuming and more expensive: payroll staff and workers need to leave the production floor to collect their pay (which in Cambodia is twice a month). Even when factoring in the costs of digitization—like setup expenses and transaction fees—we estimate that digital wage payments can save large factories at least $1,700 per month (see table).

Digital factory representatives reported an overall satisfaction with the ease of administering digital payrolls. Despite some frustration with technical issues that may occur once a year at most, most factory managers believed that the shift from cash to digital wage payments was convenient for both the factory and the workers.

ii. Workers can benefit from an increased use of digital financial services

Workers who started using digital transfers for person-to-person payments, such as remittances to rural areas, are saving money compared to cash payments. Such transfers can have significant development benefits for the recipients, especially women from rural areas who often otherwise face the cost and travel time to bring home money in person. Workers who receive digital wage payments should ideally begin to use their financial accounts for other digital transactions such as rent and utilities. In addition, if accounts are designed to facilitate convenient and affordable withdrawals, workers who have a bank account are likely to save their money there, which could help them accumulate savings in the long run through a default effect.

Access to technology is the foundation of digital development and digital financial services. The financial infrastructure surrounding Cambodia's garment sector is ripe for digitization. Almost all workers we interviewed have a smartphone and ATMs and mobile agents are mostly accessible - although some factories are still a few kilometers away from the nearest ATM machine.

Digital wage payments in the factories we studied are handled by both bank and Fintech (mobile) providers. All payroll products are interoperable so that users can freely send money to friends and family on different platforms. However, different providers offer workers a wide range of digital payment services, as well as different business models and incentives. For example, bank products typically offer free withdrawals at its ATMs. In contrast, mobile products typically offer workers one free withdrawal per pay period—which creates an incentive for workers to cash out their entire salary on payday.

To accelerate digital wage payments in Cambodia, stakeholders should focus their efforts on four areas

Although Cambodia is well-positioned to expand digital wage payments in the garment industry, challenges remain. They include the perceived cost of wage digitization by employers, workers’ limited experience with financial products and services, especially women, and the dominance of the cash ecosystem. To address these barriers, stakeholders should focus their efforts on four areas:

- Ensure responsible digital wage payments. In September 2021, the UN released the “UN Principles for Responsible Digital Payments” which outlines nine principles that define who needs to be responsible, what it means to be responsible and how to be responsible.

In line with the new UN Principles, workers should have access to appropriate payroll tools, product and fee transparency, and a fair recourse system for dealing with complaints about digital payments. Factories and Financial Service Providers (FSPs) should also ensure the protection of workers’ identity, payroll, and financial data. Payment information is increasingly being used for marketing and credit scoring, and while data has the potential to offer workers access to formal credit and other financial services, it also raises cybersecurity concerns.

- Provide support for workers to gain full benefits from wage digitization: The most immediate challenge will be to train workers and help them gain knowledge and confidence about digital financial transactions. The experience in Bangladesh has demonstrated that wage digitization alone is not enough for workers to benefit from digital payroll. Women have unique needs that must be considered when designing interventions. For example, ensuring women receive wages in their own accounts, giving them time on payday to visit cash-out points, and organizing group visits to cash-out points would help them feel secure.

HERproject has already developed a wide range of open-source materials, including posters, videos and tech tools in Khmer, to support garment sector managers and workers, including women’s specific needs, move to digital wages. More training and support to workers is needed to help them open and use financial accounts, and train them on savings, budgeting and wage spending.

- Encourage and enable merchant payment digitization to support the commercial viability of payroll accounts: The current business model of FSPs is to earn money through fees charged for cash-out transactions. But this model needs to evolve to encourage financial transactions to remain digital and for workers to make many transactions during the month, including for purchases. For example, FSPs could make money through fees paid by merchants and banking partners for the service without transferring the costs to low-income workers. Our study shows that most businesses that serve garment workers currently receive customer payments in cash because merchants still need to pay their suppliers in cash. A wider acceptance of digital payments will require a supply chain approach.

- Foster competition among FSPs: Factories in Cambodia do not allow workers to choose their payroll account provider—they receive their salary into an account chosen by the factory. In the long run, competition for workers as customers will encourage FSPs to design better products and maintain lower prices. Therefore, factories should aim to move beyond direct contracts with FSPs and towards working with a digital payroll service that can deposit workers’ wages in any bank or Fintech account.

Efforts to promote the transition from cash to responsible digital wage payments for the garment sector in Cambodia are already underway. One example is ILO’s Global Centre on Digital Wages for Decent Work, which will build on the results of this study to engage in Cambodia later this year. As the shift towards digitization continues in Cambodia, there are opportunities to collaborate across organizations to collectively advance digital payments and to move further and faster.

This research has been conducted by BSR’s HERproject and IFC, under the ILO/IFC Better Work partnership, in close collaboration with Better Factories Cambodia. The Walt Disney Company (BSR) and the European Union (IFC under ILO/IFC Better Work partnership) funded the work and Microfinance Opportunities assisted in the development of this research.

Join the Conversation