A farm in Bicol Region, Philippines. ©World Bank

A farm in Bicol Region, Philippines. ©World Bank

Sitting down with farmers in Bicol early this year, we heard a clear message: "We suffer many losses after disasters; reliable agricultural insurance could be our financial safety net,” they say. In 2023, the region experienced devastating floods and landslides.

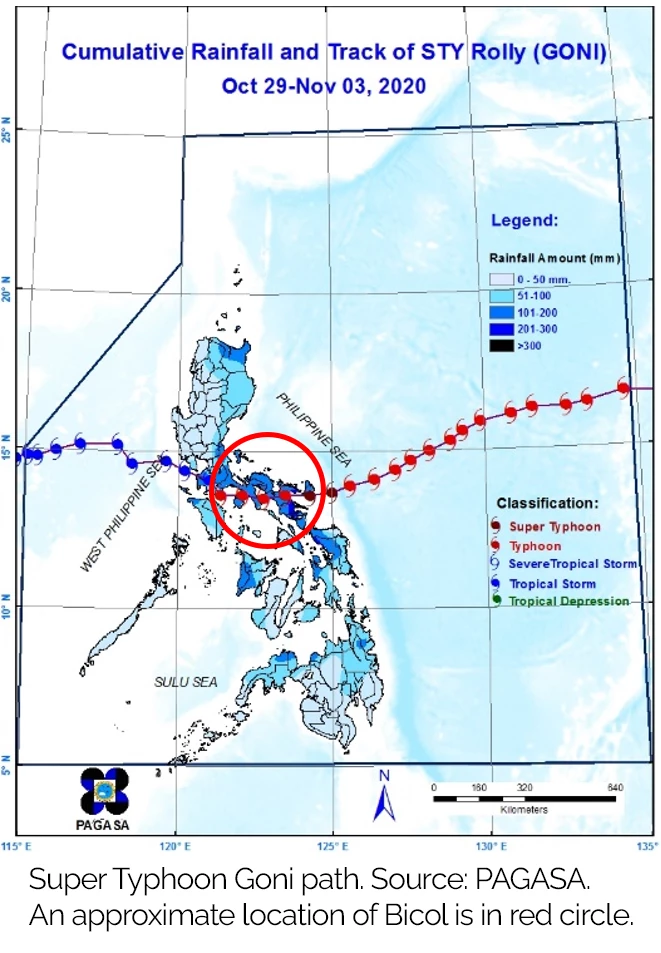

A few years earlier, Super Typhoon Goni tore through Bicol region, destroying crops and livestock. Such events are commonplace in the Philippines with an average of 20 typhoons occurring annually, and 8 to 9 of these making landfall.1 Agriculture is the sector that suffers the most significant losses following disasters in the Philippines,2 and climate disasters are responsible for most of the damage to farmers.3

After these shocks farmers need finance to get back on their feet. Farmers can use savings and credit, alongside insurance, to manage these shocks. However, less than 3 out of every 10 farmers in the Philippines have access to savings accounts or formal credit. The agricultural sector received only 2.6 percent of total loans outstanding in the Philippines banking sector in 2022 despite representing 8.9 percent of GDP and almost one quarter of total employment in the country.

Super Typhoon Goni path. Source: PAGASA. An approximate location of Bicol is in red circle.

Furthermore, insurance payouts, where farmers are insured at all, are insufficient and don’t cover even the cost of new seeds and fertilizers. In the absence of access to formal credit (exacerbated by lack of adequate insurance to use as a form of collateral), farmers told us how they sometimes must rely on informal loan sharks, with very high interest rates, often giving up their entire harvest as a loan repayment. This perpetuates a vicious cycle of poverty that is difficult to break free from.

Findings of a World Bank study

In the Philippines, the provision of agricultural insurance faces major challenges, according to a World Bank study. These challenges are found in various areas, including:

- Products: Existing insurance products are not suitable for most farmers, as they are expensive to administer and do not reflect losses suffered by farmers. New products are needed for the vulnerable smallholder farmers in the Philippines (more than half of Filipino farmers own less than 1 hectare of land).

- Operations: The Philippine Crop Insurance Corporation (PCIC) has worked hard on achieving better results for farmers, but it faces critical operational challenges. For the past 40 years, PCIC has been effectively the sole provider of agricultural insurance (as the only entity that could avail of government premium subsidies). Many of its operations are still paper based and claims management does not deliver value for money to farmers. The PCIC lacks the tools to effectively manage its significant risks. Without reinsurance, for instance, PCIC could face solvency challenges in the event of a major catastrophe. This will leave farmers and the government vulnerable and exposed to the financial consequences of such catastrophe.

- Public support: The government allocates a substantial and growing budget for premium subsidies to safeguard farmers from unexpected events. Agricultural insurance in the Philippines is, in fact, one of the most heavily subsidized programs globally. However, the subsidies lack proper targeting; only one third of farmers in the country are insured, and these may not always be those who are most in need of support.

For the government and the PCIC, like many countries in the region, improving the protection of farmers in the Philippines is a priority. Reforms are already underway to improve agricultural insurance provision, spearheaded by the Department of Finance (DOF) and Department of Agriculture (DA). As one of the initial reforms, the DOF has directed the Insurance Commission to oversee the financial well-being of the PCIC. This reform is crucial in ensuring consumer protection and effectively managing the risk that the PCIC presents to the government. The PCIC Board under the leadership of the DOF is preparing revisions to the PCIC Charter to improve premium subsidy targeting, provide for public-private partnerships in agricultural insurance, facilitate new products, and improve operations of the PCIC. The DOF has also put in place a technical working group to oversee reforms to improve the provision of agricultural insurance.

Essential reforms in agricultural insurance

So, what are the reforms that are most needed? There are three essential reform areas, including:

- Reform area 1: Better products will protect farmers and help them recover after climate disasters: The government should work with PCIC on the development of new agricultural insurance products specific for different types of farmers, ranging from smallholders to commercial farming enterprises. Adoption of technology will be critical, for example using satellite data to assess losses or determine insurance payouts cheaply, transparently, and quickly.

- Reform area 2: Reforming PCIC, whilst mobilizing the private sector, will increase effectiveness and efficiency of the provision of agricultural insurance to farmers: Mobilizing the private sector for the provision of agricultural insurance is critical. The private sector can bring expertise, innovations, and efficiency. Experience from around the world - such as in Spain, Thailand, and Türkiye - show that public-private partnership can help the development of an effective and large-scale agricultural insurance market. At the same time, the PCIC needs to undertake reforms in its core functions to establish a strong foundation for collaboration with the private sector.

- Reform area 3: Adequate regulations will facilitate the reforms and increase likelihood of their success: Agricultural insurance markets require a strong enabling environment. This entails establishing a new legal framework and simultaneously reforming the targeting of subsidies to ensure that support reaches those who are most in need.

With these improvements, agricultural insurance can serve as an essential tool for Filipino farmers to effectively manage climate shocks. It can safeguard their livelihoods, protect them from falling into poverty traps, enhance their productivity and innovation, and contribute to the overall enhancement of food security in the Philippines.

To learn more, see Reforming Agricultural Insurance in the Philippines - Technical Report and Recommendations and its Policy Summary.

[1] https://www.pagasa.dost.gov.ph/climate/tropical-cyclone-information

[2] https://psa.gov.ph/content/damages-due-natural-extreme-events-and-disasters-amounted-php-463-billion

[3] Department of Agriculture. 2022. Annual Report. https://www.da.gov.ph/media-resources/da-annual-reports/

Join the Conversation