There are few better ways to reveal whether a government’s rhetoric matches reality than examining how it raises and spends public money. Are funds being spent on the things it said they would be? Are these investments achieving the outcomes that were intended? In short, are government budgets accountable?

The traditional model for how accountability functions is rather simple. "Horizontal accountability" describes the oversight exerted over the executive arm of government by independent state bodies such as parliaments and supreme audit institutions. "Vertical accountability" describes the influence citizens hold through the ballot box.

Between elections and outside of formal institutions, however, opportunities for influencing how governments manage public resources are limited. As a consequence, this simple vertical/horizontal model has proved increasingly inadequate for capturing how budget accountability works (or doesn’t) in the real world; this is especially true in developing countries, where democratic processes and formal oversight institutions can be somewhat fragile and ineffective.

A recent paper by the International Budget Partnership (IBP) and the Deutsche Gesellschaft für Internationale Zusammenarbeit GmbH (GIZ) critically examines how budget accountability operates, based on evidence from six countries where both the IBP and GIZ are actively engaged. The findings reveal a complex web of interactions between actors, both within and outside government, that together influence how public money is managed. Rather than the simple vertical/horizontal model, the sum of these interactions amounts to a whole ecosystem of potential entry points for improving accountability.

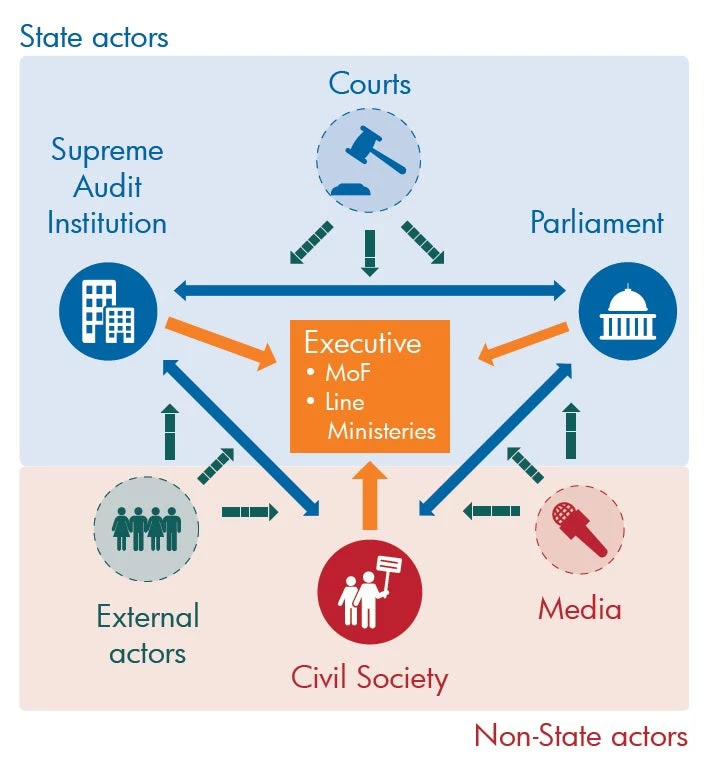

What is the budget accountability ecosystem?

The model envisages the budget system as akin to a biological ecosystem. Various organisms (or institutions) depend on each other to carry out their vital functions, and all are needed to maintain health and balance in the system as a whole.

The figure below sketches some of these vital functions: the executive relies on the legislature to assess and approve its budget proposal; the legislature depends on the supreme audit institution to independently assess actual government spending; and civil society and the media keep a watchful eye to ensure that formal institutions play their role effectively and respond to people’s needs.

The Budget Accountability Ecosystem

The budget accountability ecosystem in action

There are a number of emerging practices in different parts of the world which demonstrate how collaboration between and among different actors within the ecosystem have driven greater accountability.

In Tanzania, a local CSO helped establish an education caucus in parliament, providing budget training to parliamentarians and improving how the education budget was formulated. External audit agencies in South Korea and Chile invited citizens to point out problems in how public resources were being used, improving the targeting of their audits. While in the Philippines and Argentina, citizens participate in actual audit processes, enhancing audit quality and impact. Such examples highlight the potential that an ecosystem approach may hold if collaborative spaces and organizations are properly supported and nurtured.

At the same time, evidence from the six case studies highlights how challenging collaboration among different actors can be, especially when legal frameworks or technical capacities are weak, or when entrenched practices and interests get in the way.

Supporting an ecosystems approach

Promoting a healthy budget accountability ecosystem depends on a number of actors , both domestic and external. As far as what domestic actors can do at the country level, the paper highlights some areas for improvement:

- Introduce legal and institutional changes that improve the framework for budget accountability and provide better incentives for collaboration among different actors.

- Promote more and better quality opportunities for dialogue and exchange between state and non-state actors.

- Strengthen the capacities of all actors.

The paper also documents the variety of initiatives that external actors support, while noting their overly technical focus and limited coordination. Three areas for improvement were identified:

- All external actors should improve their understanding of the country context – for example, through political economy analysis – and shape their interventions accordingly, responding to local problems.

- Coordination mechanisms should be improved by, for example, promoting joint analyses, strengthening existing coordination mechanisms around budget reforms, and ensuring that official and non-official external actors share information and work together where possible.

- External actors should step out of comfort zones, focusing more on brokering contacts and building trust among different budget accountability actors, highlighting the mutual benefits of collaboration, and increasingly look for ways to link up country-specific activities with regional and international ones.

Join the Conversation