Coffee producers in Mexico. Photo: World Bank

Coffee producers in Mexico. Photo: World Bank

This blog was first published on the WEF Agenda website

At the end of 2023, at a meeting with Latin American heads of state, US Treasury Secretary Janet Yellen laid out once again her vision for “friendshoring” – “diversifying our supply chains across a wide range of trusted partners and allies” – a prospect that she argued has “tremendous potential benefits for fueling growth in Latin America and the Caribbean.”

However, countries in Latin America and the Caribbean have been slow to board the nearshoring boat and, more generally, to develop strategies to leverage the maximum development impact from its foreign direct investment. Both are key to ensuring that they do not miss out on these opportunities.

Strategic positioning

The stars seem to increasingly align for the region to capture more foreign direct investment and parts of the global value chains. If the appeal of China’s low wages once trumped Latin America and the Caribbean’s proximity in terms of language, culture and timezone, those wages are now higher than those in Brazil and Mexico. The vulnerabilities of the supply chain during the COVID-19 pandemic and the intensifying Sino-Western geo-strategic tensions have investors looking to diversify their risk geographically, which is expected to persist.

Further, the region’s incredibly green energy grid – 50% of its energy is produced by renewable sources – positions it well to compete with coal-intensive Asian exports in the face of potential carbon border adjustment mechanisms from the European Union.

The region certainly needs the infusion of capital and technology. Its modest growth rates at 2-2.5%, roughly half that of other emerging markets, are driven by correspondingly humble investment in plant and machinery and the innovation that drives productivity. Public investment, including infrastructure, is half of what it is in Asia or Africa as a share of gross domestic product (GDP). The debt accumulated during COVID-19 complicates the fiscal space for any new projects in the foreseeable future. Boosting the roughly 3-4% of GDP that foreign direct investments have constituted in the past would be an important contribution.

Navigating barriers

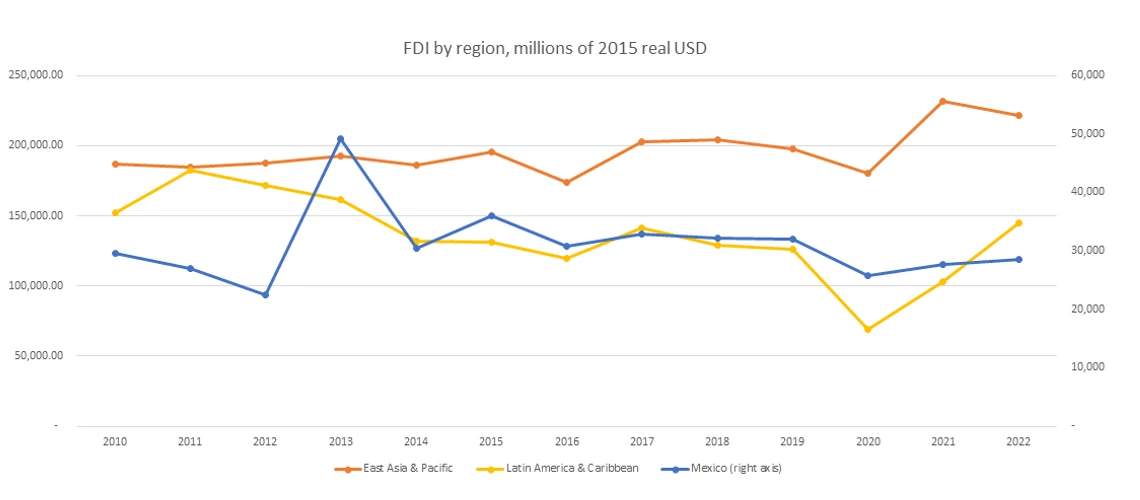

But stellar alignment or not, it’s not clear that countries in Latin America and the Caribbean are aboard the nearshoring boat. Despite the inexorable rise in Chinese wages, the 2018 Trump tariffs on China and the de-risking momentum, the 2022 post-COVID-19 uptick in foreign direct investment flows to the region comes after a decade of decline and is still substantially below 2010 levels. Further, foreign direct investment seems to have followed countries in Asia, for instance, Vietnam, whose wages remain competitive.

Source: Author’s calculation using UNCTAD FDI database and FRED CPI

Source: Author’s calculation using UNCTAD FDI database and FRED CPI

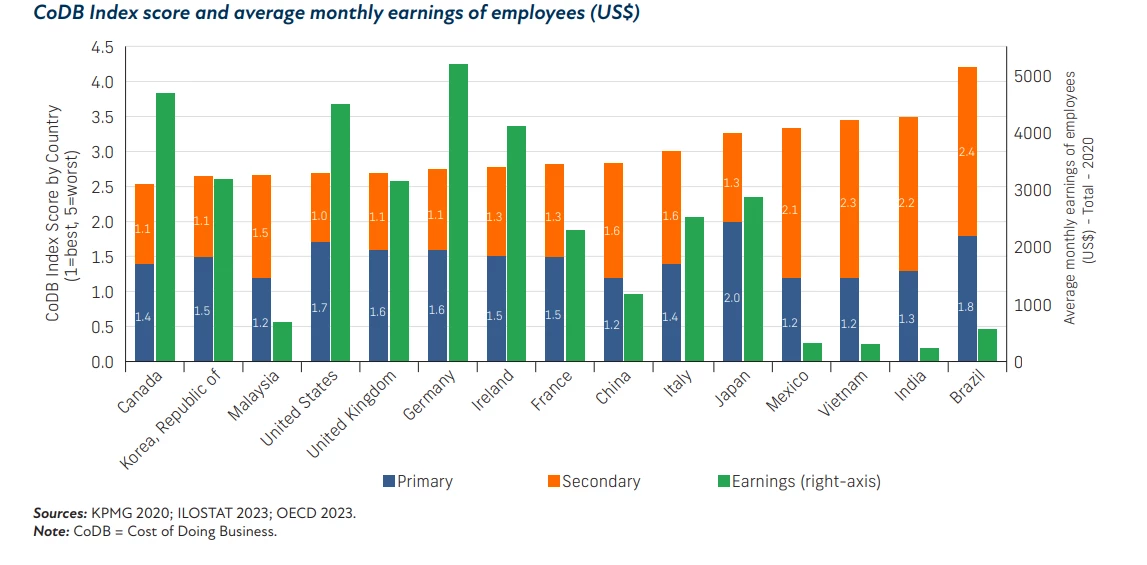

Aside from wages, higher costs in other dimensions dent the region’s competitiveness. A recent study by KMPG and the Manufacturing Institute suggests other high primary costs, such as taxes and financing. Further, when secondary costs, such as infrastructure, logistics, workforce quality and policy stability, are factored in, Canada, Korea, the United States and even Germany have an advantage over, for example, Brazil.

Other World Bank studies confirm that Latin America and the Caribbean could increase competitiveness. The World Bank Logistics Performance Index puts Latin America and the Caribbean squarely in the middle of the 139 countries ranked. Among developing regions, Latin America and the Caribbean invest among the least in infrastructure as a share of GDP – roughly a third of East Asia – and this spending needs to be more efficient.

World Bank enterprise surveys show that 29% of firms report a lack of qualified labour as an obstacle to growth compared with 15% in Asia. Even many years after the North American Free Trade Agreement, industrial parks in the north of Mexico complain of electricity and water shortages as major bottlenecks.

Policy pathways

Such challenges need not be game-enders and can be targeted by policies. In China, pro-active policies of local governments were employed to attract foreign direct investment and facilitate its success by, for instance, helping firms navigate the local system and resolving bottlenecks.

Similarly, Singapore’s Economic Development Board is seen as a critical ingredient, even in a highly welcoming business environment, to wooing foreign direct investment and encouraging it to engage in progressively more sophisticated tasks, which countries in Latin America and the Caribbean could benefit from.

Singapore and the Asian Tigers (Hong Kong, Singapore, South Korea and Taiwan), more generally, aggressively work to upgrade local firm capabilities and local innovation systems so that progressively more sophisticated tasks are onshored and supplier networks can emerge organically and efficiently.

Diverse approaches

Plans to seize the current opportunity are yet to emerge in any committed way in Latin America and the Caribbean. Mexico has taken an ambivalent stance, including disbanding its foreign direct investment promotion authority and observers worry that it is foregoing multiples of current foreign direct investment arrivals.

On the other hand, Costa Rica, working with the United States to take advantage of the 2022 Chips and Science Act, has leveraged its engineering capabilities and skilled workforce to attract $1.2 billion in new INTEL investments over the next two years. Colombia has taken tentative positive steps, recently bringing US CEOs to the cities of Cali and Quibdo. However, such efforts could be ramped up.

The country has ports on both coasts, established manufacturing centres such as Medellin and Bogota and cities in the relatively tranquil Coffee Axis with good infrastructure and education, including some like Manizales in Caldas that are working aggressively with the Massachusetts Institute of Technology to improve their entrepreneurial environment. A Singapore-style effort could help match these regions with potential partners.

Opportunity into investment

Proximity alone cannot guarantee foreign direct investment or ensure a more dynamic development impact than in previous eras. A more deliberate and energetic effort and vision could help shift the region out of its growth doldrums.

If Latin America and the Caribbean embrace nearshoring and green transition-related foreign direct investment, including in commodities, less as a source of employment and taxes and more as a fulcrum for national learning, both movements could prove transformational.

It will require trade facilitation and port efficiency improvements, help navigating local conditions and deeper trade agreements. But it will also require developing the capabilities – basic and technical education, managerial and engineering capabilities – that have been integral to the success seen in Asia.

This blog was originally published on World Economic Forum on February 19, 2024.

Join the Conversation