The Uganda Bureau of Statistics (UBOS) continues to monitor the impact of COVID-19 on the socio-economic wellbeing of the national population through the Uganda High-Frequency Phone Survey (UHFPS). The financing for data collection and technical assistance has been provided by the World Bank and the United States Agency for International Development (USAID). The survey recontacts households that had phone numbers for at least one household member or a reference individual from the Uganda National Panel Survey (UNPS) 2019/20. The first round of the survey was conducted in June 2020, while the latest seventh round was conducted in October/November 2021 after the second lockdown was introduced in June 2021. This blog highlights selected findings on the economic impacts of the COVID-19 related measures from the latest round. Where possible we also compare the impacts from two different lockdowns introduced in March 2020 and June 2021 by using the data from rounds 1 and 7 conducted after the lockdowns.

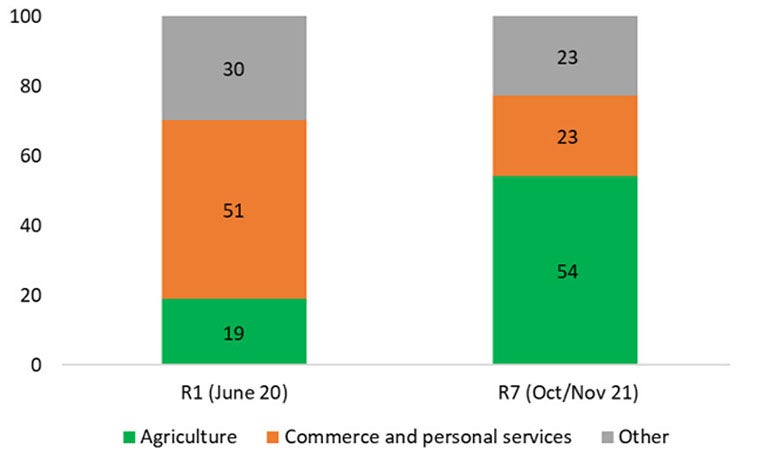

The first most important indicator we looked at was employment. Employment rates among respondents dropped from 92% in March/April 2021 to 81% in October/November 2021, falling below the pre-March 2020 level used as a pre-pandemic baseline number (87%). This is likely due, at least in part, to the economic consequences of the lockdown imposed in June 2021 during the second COVID-19 wave. However, this decline was less pronounced relative to the drop in June 2020 after the first lockdown in June 2020 (figure 1). The incidence of work stoppages reported in October/November 2021 were also more universally distributed compared to June 2020 when work stoppages concentrated in urban areas and in the services sector. As shown in figure 2, most work stoppages after the first lockdown were in non-agriculture sectors, while more than 50% of work stoppages after the second lockdown occurred in the agriculture sector. We have also found that work stoppages in October/November 2021 were to a less extent associated with COVID-19 related restrictions compared to stoppages in June 2020. It may be related to the strictness of the first lockdown which was shorter, but tighter than the second one. In addition, higher work stoppages in the agricultural sector can be related to seasonality and prolonged dry spells observed in different parts of the country in 2021.

Figure 1. Respondents working during last seven days across rounds, % of all respondents

Note: Figures are based on the same respondents across rounds.

Figure 2. Work stoppages by economic sector, % of respondents who stopped working

Note: Figures are based on the same respondents across rounds.

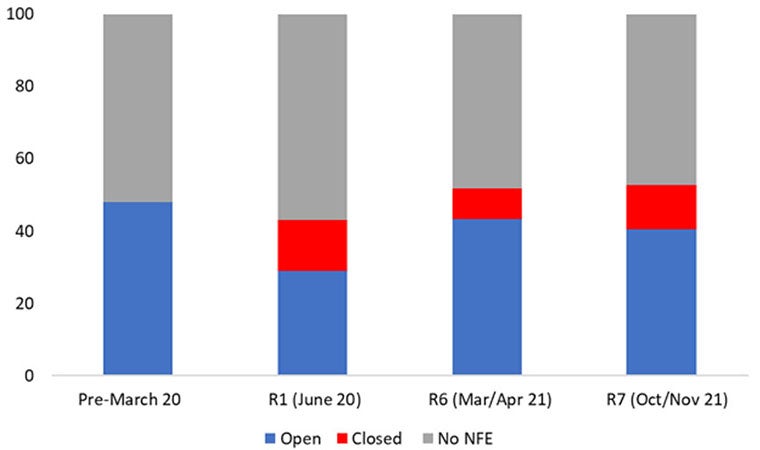

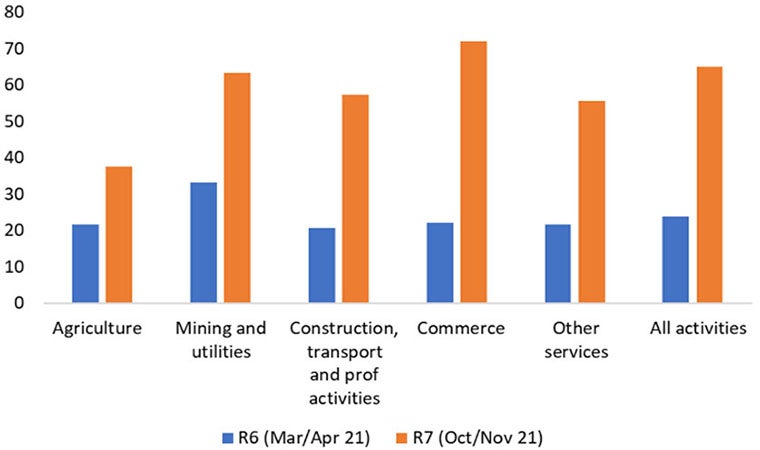

Non-farm family business closures were less frequent in October/November 2021, but almost two-thirds of businesses reported less revenue compared to the previous round in March/April 2021. As shown in figure 3, the share of households with non-farm family businesses that were open declined from 43% to 41%, reversing the positive trend observed in previous rounds. The magnitude of closures was much smaller than in June 2020 after the first lockdown. However, many operating businesses reported less revenues in October/November 2021 compared to the previous round (figure 4). Specifically, family business revenues were lower for 65% of households compared to revenues in March/April 2021. Revenue losses were particularly pronounced in businesses operating in the services sectors.

Figure 3. Status of non-farm family business across rounds, % of households

Note: Figures are based on the same respondents across rounds.

Figure 4. Family non-farm businesses reporting less revenues compared to previous round, % of households with family non-farm businesses

Note: Figures are based on the same respondents across rounds.

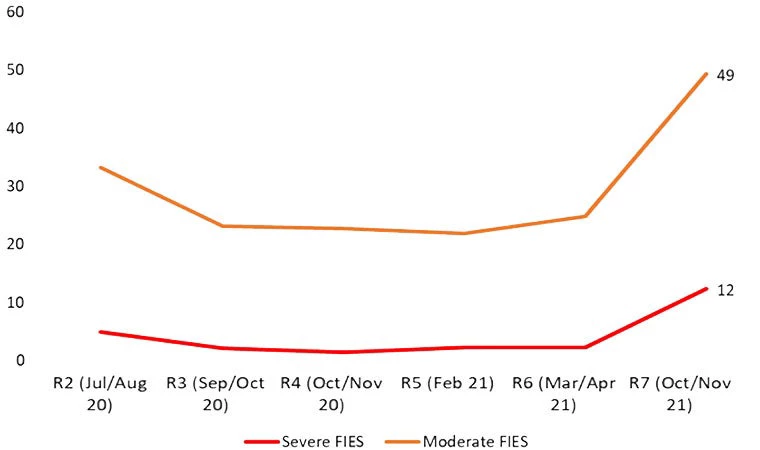

Consistent with the negative trends observed in the labor market in October/November 2021, food security in Uganda deteriorated notably in this period as well. Figure 5 presents the dynamics of the Food Insecurity Experience Scale (FIES) indices across different rounds of the UHFPS. After a long period of relatively low food insecurity between September/October 2020 and March/ April 2021, the situation has drastically changed in recent months.

Food insecurity increased dramatically in October/November 2021 in all regions, with almost half of households reporting that their family members were moderately insecure and 12% reporting family members being severely food insecure at the national level.

In the first round of the UHFPS, food security was measured only for adult members of the household. Comparable FIES indices were constructed for the seventh round. It turns out that food insecurity was higher in October/November 2021 compared to June 2020. This could be related to higher work stoppages in the agriculture sector and rural areas associated with floods and dry spells recorded in the second season of 2020 and the first season of 2021.

Figure 5. Evolution of severe and moderate composite FIES index across all rounds, % of household members

Note: Figures are based on the same households across rounds.

If you are interested to learn more about findings from the seventh round of the UHFPS please check the brief here, while the microdata and related documentation are freely accessible at the World Bank’s Microdata Catalog here.

The members of the team working on the Uganda High-Frequency Phone Survey on COVID-19 (listed in alphabetical order for each institution) are: UBOS: Henry Mubiru, Andrew Mupere, Vincent Ssennono; World Bank: Aziz Atamanov (Poverty and Equity GP), Frederic Cochinard (LSMS), John Ilukor (LSMS), Talip Kilic (LSMS), and Giulia Ponzini (LSMS).

Join the Conversation