In today's rapidly digitalizing world, a growing number of new tools are available to increase access to the financial services that people need to save, invest, and conduct daily business activities. These tools drive efficiency and reduce costs, stimulating gains in financial inclusion, fostering economic growth, and reducing income disparity, especially for women. However, to fully harness the benefits of these digital financial services (DFS) to close gaps in gender equality, policymakers must consider the unique challenges women face in accessing formal financial services.

Barriers to women's digital financial inclusion

Women face several barriers that impede their access to financial services. Factors such as limited financial literacy, lack of formal identification documents, societal norms, and cultural constraints often discourage women from utilizing financial products. Unequal access to technology exacerbates demand-side barriers for women in accessing financial services. Limited ownership of smartphones, digital illiteracy, and restricted internet access disproportionately affect women, hindering their ability to engage with modern financial tools.

Supply-side obstacles further reinforce these barriers. The lack of supply-side gender-disaggregated data, limited agent networks, and inappropriate products & services design stifles progress. Financial institutions inadvertently perpetuate gender disparities by offering generic financial products that inadequately address the unique needs of women. Additionally, regulatory hurdles and discriminatory laws, impede women's access to financial services. Globally, on average, women enjoy only 77 percent of the legal rights that men do. Moreover, in 2022, the global pace of reforms toward equal treatment of women under the law has slumped to a 20-year low.

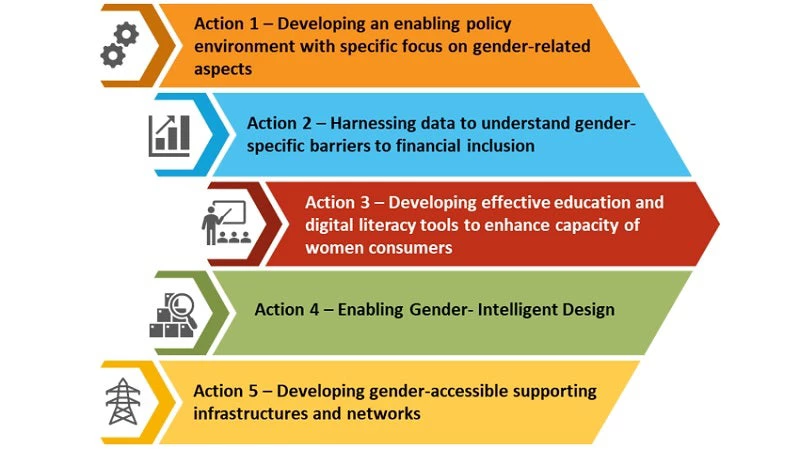

Figure 1: Action areas to advance women’s digital financial inclusion

What financial sector authorities need to do

In an upcoming World Bank paper, we recommend ways to dismantle barriers to women’s access to formal financial services . Some key potential areas for financial sector authorities, and examples of where countries have advanced on these include:

- Moving beyond gender-neutral to gender-intentional policies: Gender-intelligent regulatory frameworks and policy measures could address the unique challenges women face in accessing and using DFS. Implementing tiered customer due diligence (CDD) regulations based on risk profiles, recognizing alternative identification documents, and introducing a vulnerability lens in consumer-protection regulations are essential to bridge this divide. By incorporating a vulnerability lens into regulations, policymakers can proactively address and mitigate the negative experiences that women have with DFS. Mexico’s tiered account-opening requirements is an example of gender-intentional policy intervention that provides practical lessons on developing policies to extend financial services to women and other underserved populations.

- Illuminating the path forward with sex-disaggregated data (SDD): Better data offers better insights into the financial behaviors of different groups. Financial sector players need disaggregated demand-side and supply-side data to inform policies and regulations. Bank Negara Malaysia’s commitment to collecting SDD served as a starting point for a framework that recognizes specific challenges and interventions, such as gender-smart products and financial education for women.

- Igniting change through education and empowerment: Developing effective digital financial literacy (DFL) initiatives is crucial. A national financial inclusion strategy could help coordination between key stakeholders to prioritize DFL. Context-sensitive approaches, multi-pronged learning methods, and gender-specific targets are essential to enhance women's capacities to utilize DFS. Community-based initiatives can serve as platforms for digital literacy education and resources for women and marginalized groups. Indonesia’s women digital ambassadors leverage community connections through women’s cooperatives and trained ambassadors. They mentor women to access and use DFS offered through Laku Pandai (branchless financial services) agents.

- Designing for equality: Establishing a common understanding of gender-intelligent design, incentivizing research, and incorporating gender-sensitive procurement processes are key steps, along with including gender-intelligent indicators in monitoring and evaluation frameworks. Pakistan’s Asaan Mobile Account (AMA) is an example of an innovative product that allows individuals to access mobile payments without smartphones or internet connectivity. With its simplified account opening procedures AMAs cater to people without bank accounts, such as women, youth, and low-income individuals. In 2023, the initiative successfully opened over 7 million AMA accounts, contributing towards the financial inclusion agenda.

- Building infrastructure for all: Regulators should build bridges that connect women to the financial tools they need. Accessible infrastructures, such as interoperable digital payment systems and collateral registries, make it easier for women to participate. Policymakers should ensure gender-inclusive design for infrastructure and encourage collaboration among financial service providers to enhance interoperability. Lessons for authorities can be learned from Senegal's ID reforms, which eliminated additional documentation requirements for married women applying for ID cards. Such ID reforms simplify acquisition of ID for women. Tanzania's experience with mobile money interoperability simplified procedural requirements, improving convenience, lowering costs, and increasing competition.

Facilitating women's digital financial inclusion is a crucial move for achieving gender equality. Let's work together to remove obstacles, leverage technology's potential, and establish a digital landscape that is inclusive and empowering. More guidance to regulators on gender interventions can also be found at the DFS Reference Guide.

Join the Conversation