boy and older woman looking out the window

boy and older woman looking out the window

Since the 2015 Paris Agreement, there has been a groundswell in city-level commitment to climate action: almost 9,400 cities around the world have committed to over 20,000 individual and cooperative actions to address climate change. Having erred on the side of caution for years, financial institutions are beginning to lend to green cities. Here are three factors for them to consider in the process.

1. Green and climate-smart city investments make good business sense

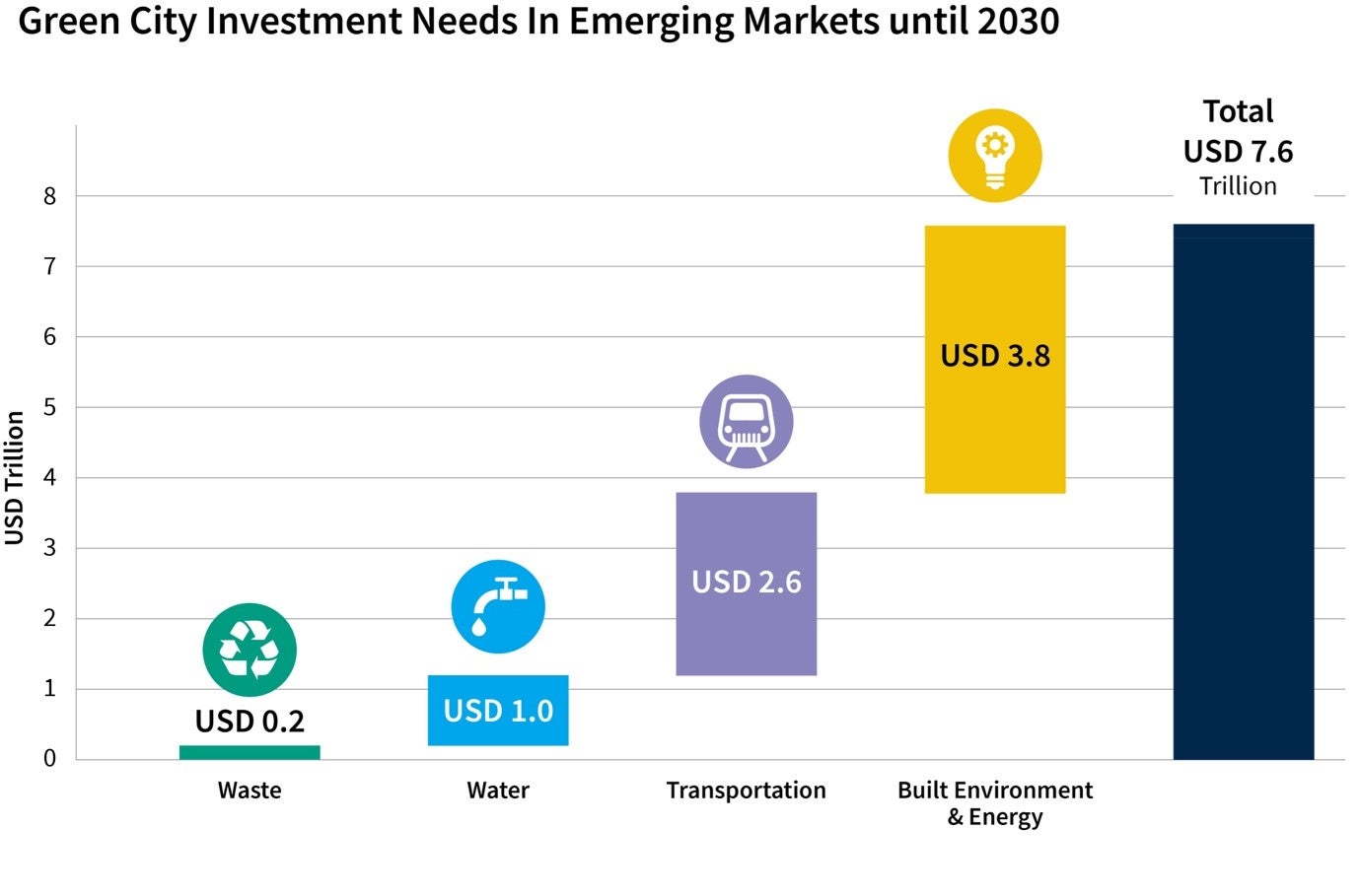

Climate-smart growth presents a tremendous investment opportunity. IFC, the private sector arm of the World Bank, estimates that cities in emerging markets represent a USD 7.6 trillion green investment need between 2023 and 2030.

To reach net zero emissions by 2050, global investments of between USD 5.2 and 5.4 trillion will be required to decarbonize existing buildings alone.

Green municipalities have the potential to improve their creditworthiness across a wide number of sectors for the following reasons: First, green cities are more resilient to environmental crises because they are better equipped to cope with energy and water shortages. Second, cities can leverage new policies to generate superior tax revenue – including congestion charges and on-site renewables. And third, greener cities can run on lower costs, thanks to better urban planning and more efficient management of activities such as waste collection, transportation, and energy use.

Lastly, while cities need to make upfront capital investments to implement climate-smart initiatives, often using debt, a city’s financial position improves when returns outweigh the cost of finance, making this a win-win for all.

2. Cities in emerging markets have a significant untapped borrowing capacity

Even in markets where subnational entities are in a position to borrow, creditworthy cities are sometimes reticent to borrow due to economic uncertainty and a lack of available finance - including the sparse municipal bond markets in emerging economies.

Borrowing from banks can provide cities with immediate access to a significant amount of capital, contribute to diversifying their funding, and enable them to invest in infrastructure projects that can dramatically reduce their carbon footprint.

Borrowing from private lenders can also increase scrutiny of municipal budgets, maximizing transparency and accountability, while triggering more flexible management of funds – for instance through moving expenses from off-balance sheets to on-balance sheets.

For example, in January 2022, Helsingborg, Sweden, became the first city worldwide to issue a sustainability-linked bond to attract capital in pursuit of its ambitious net-zero goals. Under this performance-based bond, the city’s emission reduction rate is used as a Key Performance Indicator (KPI). Greenhouse gas (GHG) emissions are publicly tracked, increasing transparency and allowing investors to monitor progress against a city’s stated objective.

3. Banks and cities can work together to aggregate green investments and generate more business

An innovation of IFC, APEX (Advanced Practices for Environmental Excellence in Cities) allows cities and banks to collaborate and scale up urban infrastructure projects. The platform leverages IFC’s well-established Cities Initiative, which combines investment and advisory services for cities, including through the provision of direct municipal financing. This, in essence, allows commercial banks to grow and green their investments.

The APEX Green Cities Program helps cities in emerging economies to identify, prioritize and finance high-impact carbon-reduction policies and green infrastructure projects as identified in their Climate Action Plans and Green City Action Plans. APEX helps bridge the gap between banks and cities by identifying eligible investment pipelines and creating Key Performance Indicators underpinning sustainability-linked loans or bonds.

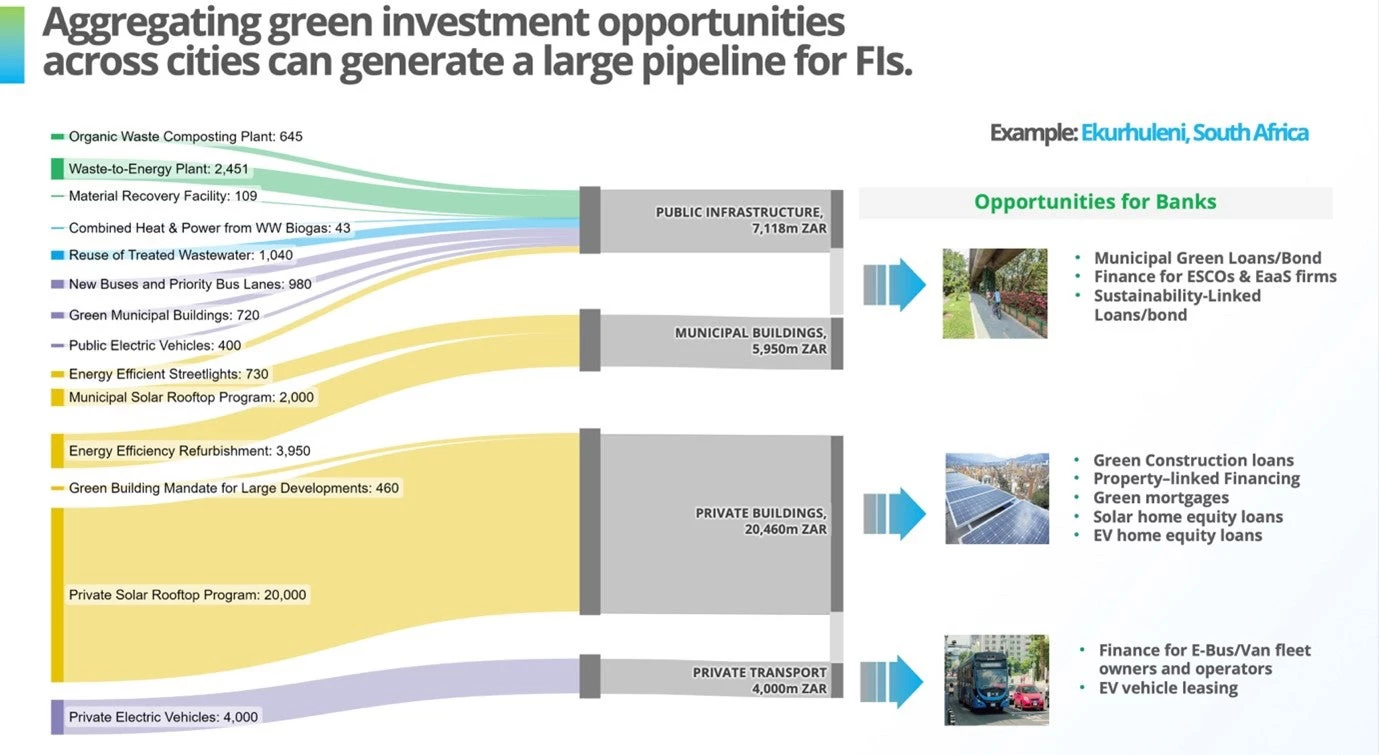

An example from Ekurhuleni, South Africa, demonstrates how banks can work with cities to aggregate green investment opportunities by creating a significant pipeline for lenders.

The Ekurhuleni example also shows how banks can move away from financing isolated projects, and begin to finance large thematic portfolios, including public infrastructure, municipal and private buildings, and private transport. This allows banks to develop new products and grow their portfolios by:

- Indirectly supporting energy efficiency upgrades for existing buildings by providing finance for Energy-as-a-Service (EaaS) firms,

- Providing performance-based financing such as Sustainability-Linked Loans or Bonds, and

- Partnering with municipalities to offer energy-efficient and renewable energy upgrades for home and property owners via Property-Linked Financing, an approach through which monthly repayments are collected via small property tax increments.

Through the APEX Green Cities Program, which is now expanding to cities in Colombia, South Africa, India, the Philippines, Vietnam, and Indonesia, financial institutions can build subnational partnerships and expand their green portfolios while supporting local, national, and global climate ambitions.

Financing municipal initiatives to fight climate change can help commercial banks diversify their lending portfolios, tap into growing demand, and secure new business opportunities. If private financial institutions are able to tap into this new opportunity, they could play a unique role in helping shape the cities of tomorrow.

Join the Conversation