Bangladesh photo

Bangladesh photo

South Asia, battered by three years of upheaval from the COVID-19 pandemic and spillovers from Russia’s invasion of Ukraine, faces a combination of good and bad news for its economies. On the positive side, global energy and fertilizer prices are down, both tourism and business services continue to recover strongly, and the reopening of China’s economy is relaxing supply bottlenecks. However, rising interest rates and risks in the banking sector in the United States and Europe have increased uncertainties in South Asia’s outlook, given their significant impact on balance of payments, exchange rates, and financial markets

Therefore, growth in South Asia is expected to slow down in 2023, according to our latest South Asia Economic Focus (SAEF) , Expanding Opportunities: Toward Inclusive Growth. In this blog, we discuss the challenges and opportunities the region faces, and highlight expert opinions from the bi-annual survey of the South Asia Economic Policy Network (SAEPN)—a group of policy makers, academics, and macroeconomists across the region.

Experts predict dimmed growth

The bi-annual survey of the SAEPN reveals a more bearish outlook for the region compared to last fall, reflecting the slowdown in economic growth and shift in risks for the economy:

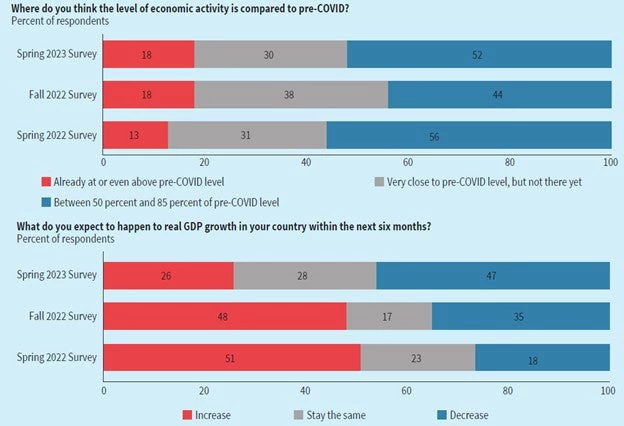

- Forty-eight percent of the respondents—as opposed to 56 percent in the fall of 2022—believe that economic activity has recovered to at least 85 percent of the pre-COVID-19 level.

- Only 26 percent believe that real GDP growth will increase in the next six months, a large drop from 48 percent last fall.

- While inflation continues to be the top perceived risk to recovery (31 percent of respondents), concerns have increased over financial sector stress (23 percent), sluggish consumption (23 percent), and increasing budget deficits (13 percent).

Challenges from balance of payment pressures

Tensions in the external sector continue despite the improving trade balances. Falling global energy and fertilizer prices have eased inflationary pressures and have also improved terms of trade of South Asian countries—most of whom are net energy importers. In turn, countries’ import bills fell.

However, as countries including the U.S. continue to tighten monetary policy to fight inflation, investors have pulled funds out of South Asia. This outflow of capital has increased pressures on balance of payments facing South Asian countries, and this in turn, translates into currency depreciation pressures. Policy makers in South Asia face difficult tradeoffs as they respond to these pressures.

New! Access our macro dashboard with high-frequency indicators such as GDP nowcasting and economic activity indicators

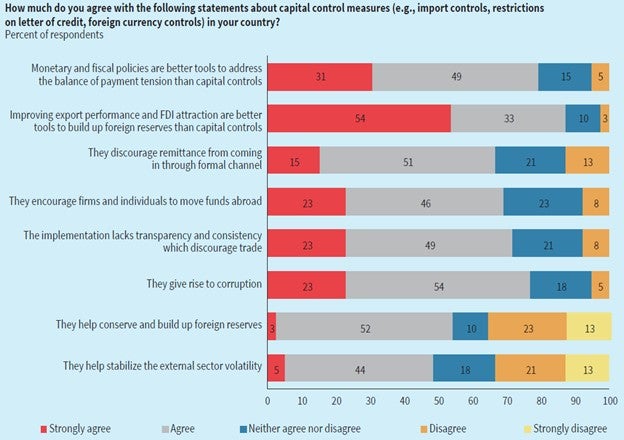

Several countries have used capital control measures such as restricting imports and tightening import financing (see our blog last fall). These measures may temporarily help countries reduce the balance of payment pressures, but they negatively affect output and investment by limiting imports. Further, as Expanding Opportunities demonstrates, the measures can be circumvented and can even backfire. For example, foreign exchange inflows can be diverted to the informal channels, reducing official foreign reserves . Survey responses support this generally negative view of capital controls:

- Majority believe that these measures can discourage overseas migrant workers from sending remittances through the formal channel (66 percent of respondents) or encourage firms and individuals to move funds abroad (69 percent), both of which would lead to a loss in the country’s official foreign reserves.

- Eighty percent of respondents agree that monetary and fiscal policies are better tools than capital controls for addressing balance of payment tensions.

- Eighty-seven percent of the respondents believe improving export performance and attracting foreign direct investment are better ways for building up foreign reserves.

Challenges from intensifying financial sector risks

Significant uncertainty in the global financial markets presents challenges for South Asia:

- The recent banking turmoil in the U.S. and Europe reveals potential challenges when interest rates rise rapidly, especially given the buildup in financial vulnerabilities since the global financial crisis.

- Banks in South Asia could also face liquidity problems if there are sudden deposit withdrawals, for example. Some countries like Sri Lanka and Bangladesh are especially vulnerable, given rising non-performing loan ratios—a key indicator of worsening asset quality—in the banking sector as well as non-bank financial institutions.

- A weak domestic banking sector increases the probability of runs and other stress events on banks, and South Asian countries are particularly vulnerable to contagion from volatile global financial markets.

Other domestic macro challenges in the financial sector are also evident in South Asia:

- Elevated inflation and negative shocks such as the severe floods in Pakistan last year continue to pressure banks’ balance sheets as many distressed loans are concentrated on firms suffering losses from these shocks.

- Private sector credit growth has accelerated, as in Bangladesh, Bhutan, and India, while deposit growth has declined and has fallen behind credit growth. The widening gap between credit growth and deposit growth could limit the ability of banks to lend.

- Governments increased borrowing from domestic banks to finance their record debt, and as a result, sovereign-bank nexus increased, heightening the financial sector’s vulnerability, especially in Maldives, Pakistan, and Sri Lanka.

Again, SAEPN survey respondents agree with this assessment:

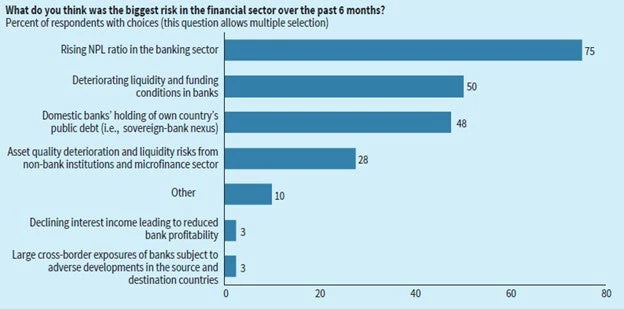

- Seventy-five percent of survey respondents agree that rising non-performing loan ratios in the banking sector was the biggest risk in their countries’ financial sector.

- Half of the respondents believe deteriorating liquidity and funding conditions in banks were the biggest risk.

- Forty-eight percent of respondents believe increased sovereign-bank nexus was the biggest risk.

Opportunities for broad reforms and inclusive growth

First, countries should use opportunities to improve trade balance and lower energy prices to move away from ad hoc measures such as fuel subsidies and import restrictions.

Second, fiscal sustainability must be at the center of broad reform programs, and to achieve this, countries will need to reduce subsidies and increase revenues. One way the latter can be accomplished is to use the present crisis as an opportunity to broaden the tax base by reducing inequality of opportunity—significantly larger in South Asia than in other regions—and giving more people an opportunity to participate in the economy. For example, increase female labor force participation, move workers out of the unproductive informal sectors via reforms in inclusive education policy, match education to earning ability, implement affirmative action for disadvantaged groups, and improve geographical mobility of workers across the region.

Despite the many challenges facing South Asia, the region has one of the highest potential growth. However, to achieve this potential, South Asia needs to eliminate external and inherent obstacles and turn them into opportunities to forge inclusive and productive economies.

This blog is part of a series on the Spring 2023 South Asia Economic Focus - Expanding Opportunities: Toward Inclusive Growth

Join the Conversation