On 7 July 2023, after two weeks of intense negotiations, the member states of the International Maritime Organization (IMO) unanimously adopted the 2023 IMO Greenhouse Gas Strategy. This landmark agreement replaces the 2018 Initial Strategy and significantly strengthens shipping’s greenhouse gas (GHG) reduction targets. Concretely, IMO member states agreed:

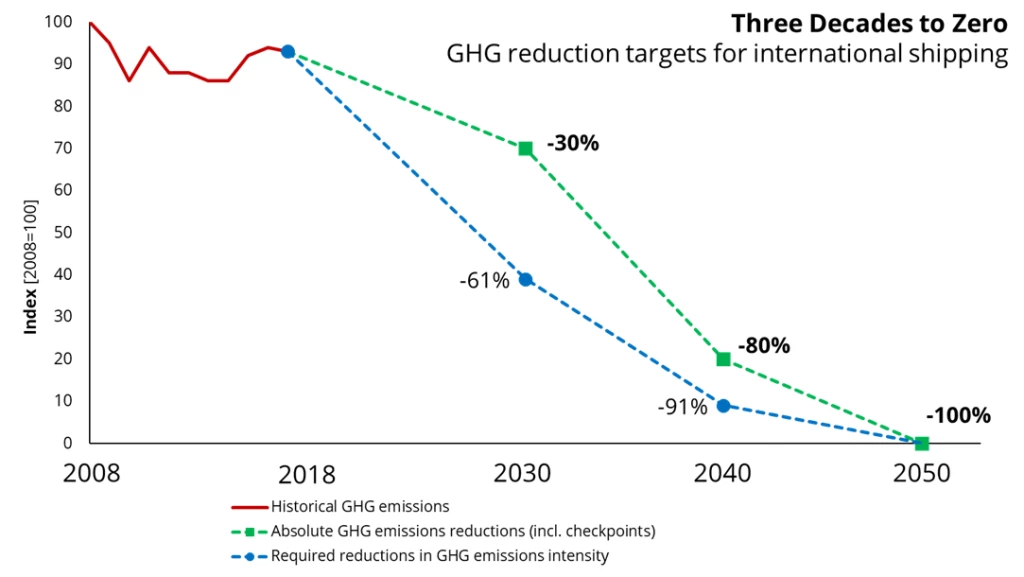

- to reach net-zero GHG emissions from international shipping by around 2050, with interim checkpoints of 20-30 percent by 2030 and 70-80 percent by 2040;

- to make zero- or near-zero GHG energy, fuels, and technologies 5-10 percent of shipping’s energy mix by 2030; and

- to develop a marine GHG fuel standard and a maritime GHG emissions pricing mechanism, which are expected to be adopted in 2025 and could enter into force in 2027.

While these targets are not entirely 1.5°C aligned—a key point of critique, the political agreement still represents an important step forward for global climate action. Eventually, it was achieved based on consensus among all 175 IMO member states.

What do these new climate targets mean in practice?

In general, maritime transport strongly correlates with global trade. The more goods are traded, the more transport service by ships is needed. Hence, the sector’s new climate ambition levels should be analyzed in this context. Historically, shipping activity has rarely remained constant. From 2008 to 2018, for instance, the size of the fleet increased by +73 percent, and the sector’s transport work (measured in ton-nautical miles) grew by +36 percent. With any further increase in global trade, the demand for maritime transport is projected to grow, too.

Despite continuous energy efficiency efforts, such growth in seaborne trade will likely result in more energy demand from ships. Since the sector nowadays relies almost entirely on fossil fuels—mostly oil, with a little bit of natural gas, GHG emissions from ships are expected to grow accordingly. To meet the recently adopted absolute GHG emissions reduction targets in a growing sector, GHG emissions intensity (emissions per transport work) across the fleet needs to decrease more than the numbers of the absolute targets suggest. What does this mean?

Shipping will need to reduce its GHG emissions intensity—as opposed to absolute GHG emissions–beyond the 20-30 percent by 2030 or the 70-80 percent by 2040. For the upper bound of these absolute targets, initial estimates suggest that GHG emissions intensity would need to decrease by around 61 percent by 2030 and 91 percent by 2040.

Historical emissions data from Climate Action Tracker; linear reduction paths assumed for simplicity; GHG emissions intensity in tCO2e per ton-miles based on a medium trade growth scenario (OECD RCP2.6 L) of roughly 2% growth per year, as used in the 4th IMO GHG Study.

Given the long lifetime of ships of 20-25 years, this implies that ships recently put into service or being ordered now ought to plan for being able to run on zero- or near-zero GHG fuels in the not-so-distant future. Otherwise, they risk ending up as stranded assets. In this policy context, environmental, economic, and financial reasons also rule out a major role for liquefied natural gas (LNG) in shipping’s decarbonization.

What does this mean for developing countries?

Adopting these more stringent targets creates unique business and development opportunities in developing countries. For instance, many of them have significant potential to produce zero- or near-zero GHG marine fuels such as green hydrogen, green ammonia, or green methanol needed to achieve these targets. The 2023 IMO GHG Strategy explicitly highlights these opportunities in developing countries. Achieving the 2040 target—which cannot be reached through energy efficiency alone—implies that several trillion dollars in investments must be mobilized to needed to produce such green fuels and develop the associated bunkering infrastructure at scale.

On top of this, the IMO also agreed that shipping’s energy transition should be just and equitable. Many countries have expressed concern about being left behind in this transition. Instead of exempting these countries and risking serious market distortions, recent World Bank research shows that potential carbon revenues from shipping appear more favorable to address these equity concerns.

What is the policy to drive shipping’s energy transition?

The IMO plans to develop a basket of policy measures consisting of both technical and economic elements:

- The technical element will be a marine fuel standard mandating the phased reduction of the GHG intensity of the energy used on board ships. This standard is expected to be key to driving the effective uptake of zero- and near-zero GHG fuels in a timely manner.

- The specific nature of the economic element still needs to be defined. Yet, it will be based on GHG emissions pricing—simply put, a carbon price on maritime emissions. Many IMO member states highlight that carbon pricing will not only reduce GHG emissions but can also make shipping’s energy transition more equitable. This is the case when revenues are strategically channeled back to those countries which may struggle the most with shipping’s decarbonization and/or climate change—most often developing countries, specifically small island developing states and least developed countries.

These measures are to be adopted in 2025, with an envisaged entry into force in 2027.

What are the next steps in the policymaking process?

In London, IMO member states also initiated an impact assessment to assess the policy measures’ socio-economic impacts, such as impacts on food security, and their ability to reach the agreed GHG reduction targets. This assessment will also consider the implications of using potential carbon revenues for specific purposes, including many of those suggested in the most recent World Bank report on distributing carbon revenues from shipping.

In parallel, IMO member states will deliberate on the details of the marine fuel standard and the design of the GHG emissions pricing mechanism. The latter would represent the very first carbon pricing instrument covering all GHG emissions of an entire sector globally. In the case of international shipping, these are almost 3% of the world’s annual GHG emissions. If shipping was a country, this would make the sector one of the world’s top 10 emitters.

Join the Conversation