Estimates of the financing gap for emerging market infrastructure range from nearly half a trillion USD to more than US$1 trillion a year over the next decade. The range reflects the difference between the estimated level of infrastructure needed to sustain growth across emerging markets and the actual level of such investment.

The challenges are immense, and resources are scarce. Of the financing that does exist, more than 70% comes from national government budgets; the second largest source (roughly 20%) is the private sector; and remaining resources come from overseas development assistance or aid from developed economies1. Given the overstretched demands of public sector budgets in developed and developing countries alike, any increase is likely to come through more partnership and co-financing from the private sector.

There are many reasons that might compel investors to take another look at emerging market infrastructure. Low growth and low interest rates in advanced economies are an unattractive environment for investors chasing higher returns. But populations in developed economies are aging, and savings are rising. This combination of persistent low returns and rising savings may compel investors and asset managers in these economies to turn to emerging markets for potential higher returns.

And infrastructure is a particularly good investment, as building good roads and bridges, and developing better access to clean energy creates a virtuous circle that promotes consumption growth and a larger market where the private sector can thrive. This is great for people and governments in emerging markets, and also for savers and investors in developed countries.

But how can the private sector learn more about investment opportunities to finance infrastructure in emerging markets?

There are several commercial databases that attempt to “map” proposed infrastructure projects by country, sector, and size, among other characteristics, to match investors to opportunities. Infrastructure Journal (IJ), for example, has a large and well-regarded database of more than 7,500 projects worldwide that span an array of sectors2. But less than half are in East Asia and the Pacific, the Middle East and North Africa, Sub-Saharan Africa, or Latin America. The total value of projects based in these regions amounts to roughly US$2.9 trillion, although just four countries (Australia, China, India and Japan) account more than a quarter of this total.

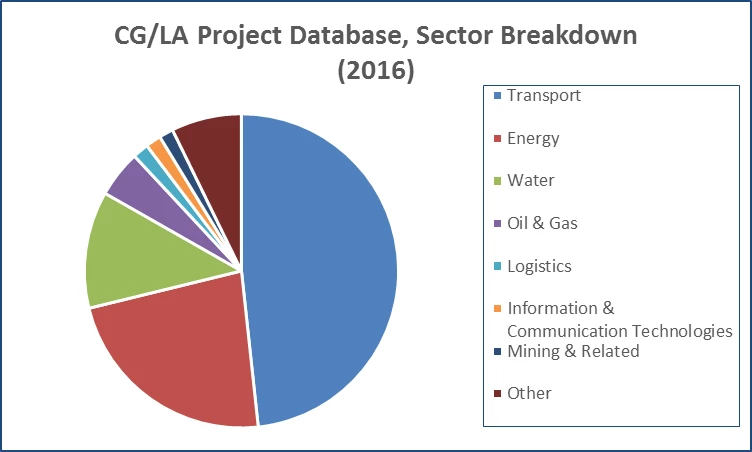

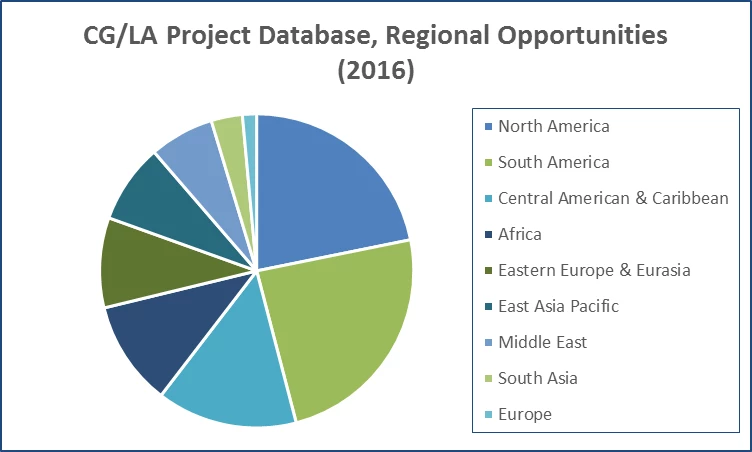

CG/LA, a Washington, DC–based consulting firm, has a database that is smaller but more oriented to emerging markets. Of more than 1,700 projects listed, nearly three-quarters are based outside of North America and Europe – about 40% in South and Central America alone. Half of the projects focus on transport – nearly 36% of which is transit – and an additional quarter on energy. The CG/LA model seems particularly innovative in that it is envisaged as a platform where information can be crowdsourced from infrastructure experts.

The Global Infrastructure Facility (GIF), another vehicle to help share knowledge, is a partnership among governments, multilateral development banks, private sector investors and financiers. It offers a new way to collaborate on preparing, structuring and implementing complex infrastructure projects while also leveraging private capital.

The World Bank Group also works to strengthen the investment environment in our client countries and to raise awareness of infrastructure investment opportunities through public-private partnerships. I am especially pleased by yesterday’s release of the report, Benchmarking PPP Procurement 2017 , the first attempt to provide comparable, actionable data on PPP procurement globally. It assesses the PPP regulatory frameworks across 82 economies, evaluating each against international best practices in preparation, procurement, and contract management, and other areas. It highlights how governments can:

- Improve their fiscal management of PPP projects

- Strengthen project preparation to attract more private sector interest

- Disclose contracts and performance information during PPP implementation to enhance transparency, among many other areas.

These are hot topics that we will discuss with governments and the private sector next week at the WBG-IMF Annual Meetings. We invite you to engage with us during the " Making Infrastructure Rewarding" session, on October 5 at 4 pm EDT. From anywhere in the world, you can participate and share your views using #InvestinInfra on Twitter. I will reflect on these conversations and ideas in subsequent posts. I look forward to hearing your feedback.

2 Taken from www.ijglobal.com . Project data excludes projects that were cancelled or have reached financial closure.

Join the Conversation