Helping communities | © shutterstock.com

Helping communities | © shutterstock.com

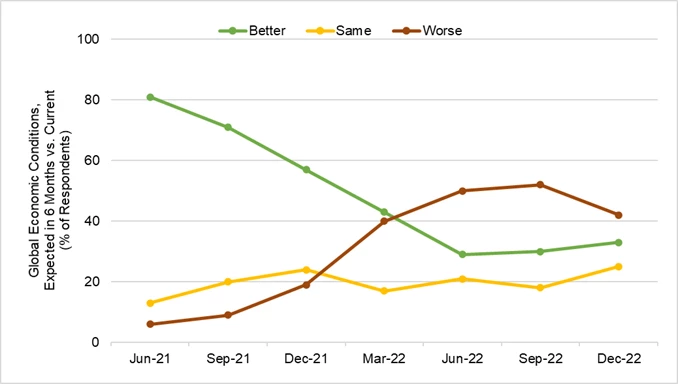

The Global Economic Prospects forecasts that 2023 will see the lowest growth rate in three decades, with the exceptions of 2009 (the global financial crisis) and 2020 (the COVID-19 pandemic). Moreover, the recently released Falling Long-Term Growth Prospects has warned that the slump in the global economy’s long-term growth rate can risk a “lost decade,” limiting countries’ abilities to combat poverty and tackle climate change. The World Bank Group’s sobering forecasts are consistent with the views of business leaders around the world, among whom the share of pessimists has increased in the last few months (see Figure 1). Multiple bank failures over the past few weeks have caused turmoil in the banking sector and rekindled fears of a financial crisis. The high hopes, shared by many, for a strong post-pandemic economic recovery may not now materialize. Bad news about growth is always alarming—low growth implies poverty and vulnerability; these in turn can lead to social unrest, political crises, and crime and violence.

Figure 1. Pessimism towards global economic conditions has grown since mid-2021

Source: McKinsey Global Survey on Economic Conditions.

Note: Between June 2021 and December 2022, the number of respondents in each survey ranged from 785 to 1,247. Respondents were business managers and executives from a range of industries across the globe. Results are weighted by the GDP of respondents’ countries.

PUBLIC DEBT CRISIS, HIGH INFLATION

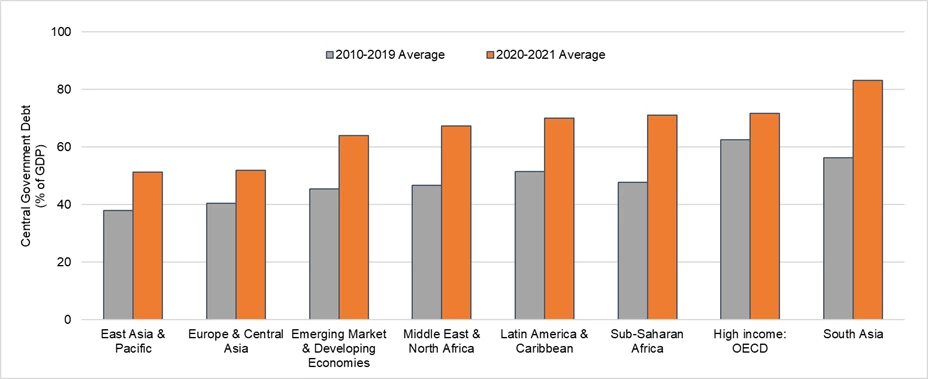

Facing a slump in growth and the possibility of a recession, the traditional macroeconomic response is through fiscal and monetary expansionary policies. For many countries, however, this may not be feasible in the current context. Expansionary fiscal policy is severely limited by public debt crises that affect many developing and advanced countries. Whether driven by low economic activity (and therefore low public revenues) or increased public spending (to support impacted households and businesses), the COVID pandemic spiked public debt around the world (see Figure 2). High debt implies that a large share of public resources is directed toward interest payments, curtailing the capacity to obtain additional debt financing, which may also be too expensive. In these circumstances, the “fiscal space” for governments to fashion a fiscal response may simply not exist.

Figure 2. Central government debt as a proportion of GDP increased in every region during the pandemic

Source: IMF Global Debt Database.

Note: Data refers to 164 economies that the Global Debt Database has information on each year between 2010 and 2021. Central government debt is the total stock of debt liabilities issued by the central government. Regional figures are unweighted averages of economy-level data within each region.

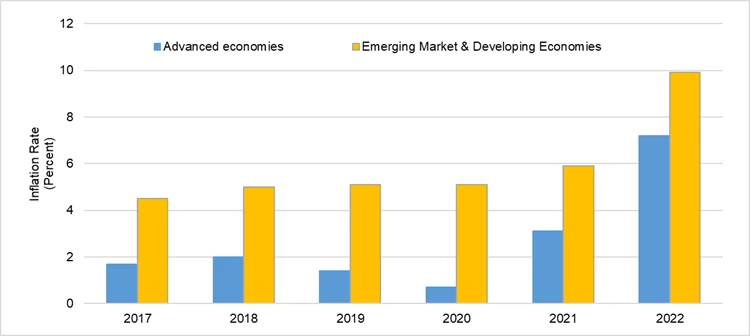

Expansionary monetary policy would counter efforts to bring inflation down in developing and advanced countries. Whether caused by supply factors (for example, disrupted global supply chains) or demand factors (for example, excessive liquidity), inflation has substantially increased and is a major concern for people and policymakers alike (see Figure 3). Again, the “monetary space” for governments to generate a monetary response to growth slowdown may not be currently feasible.

Figure 3. The rise in inflation during 2022 has affected all types of economies

Source: IMF World Economic Outlook, Oct 2022 edition.

Note: The data refers to 196 economies between 2017 and 2022 included in the IMF World Economic Outlook database.

FALTERING PRIVATE INVESTMENT

For most, if not all, countries, the private sector is the engine of economic growth. Whether countries around the world escape the impending slump or not will ultimately depend on how private enterprises and consumers act over the next few months and years.

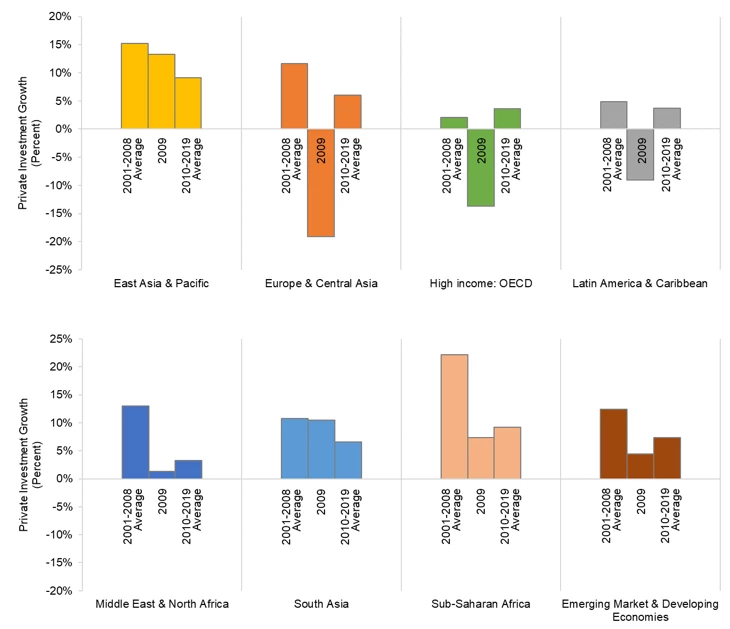

A critical ingredient of private sector activity is private investment. It is one of the main mechanisms through which entrepreneurs bring about innovation, job creation, and linkages with the rest of the economy. While public investment is important, private investment represents, on average, three-quarters of total investment in developing countries. Private investment is driven by expectations of risks and returns at the economy, sector, and firm levels and, to a large extent, these expectations are determined by how propitious the business environment is. Worryingly, private investment as a share of GDP declined in most regions after the 2009 global financial crisis (see Figure 4). Can this trend be reversed?

Figure 4. Private investment growth slowed down during the 2010s

Source: IMF Investment and Capital Stock Dataset (ICSD).

Note: Data refers to 162 economies that ICSD has information on each year between 2000 and 2019. Private investment growth is calculated based on economies’ private investment (gross fixed capital formation) in billions of constant 2017 international dollars as weights.

REFORMS IN TIMES OF CRISES

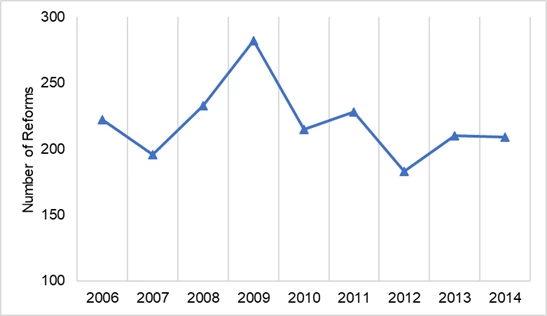

A crisis is an opportunity riding a dangerous wind, says a popular Chinese proverb. Crises can present opportunities by revealing areas of weakness, incentivizing policy action, and unifying minds on the need to reform. If the country withstands the “dangerous wind” of economic shocks, crises can beget reforms. It is well known that, in the aftermath of the 2009 global financial crises, governments introduced stricter financial prudential regulations. It is less well-known that many governments around the world also embarked on major reforms to improve the ease of doing business (see Figures 5 and 6).

Figure 5. Governments implemented a record number of reforms to improve the business environment during the 2009 recession

Source: World Bank Group Doing Business database.

Note: Data refers to reforms in 176 economies and 9 areas of business environment measured under the same methodology in Doing Business 2007-2015 reports. Doing Business 2006 covered fewer economies and Doing Business 2016-2020 expanded the measures in each area, making their numbers not comparable.

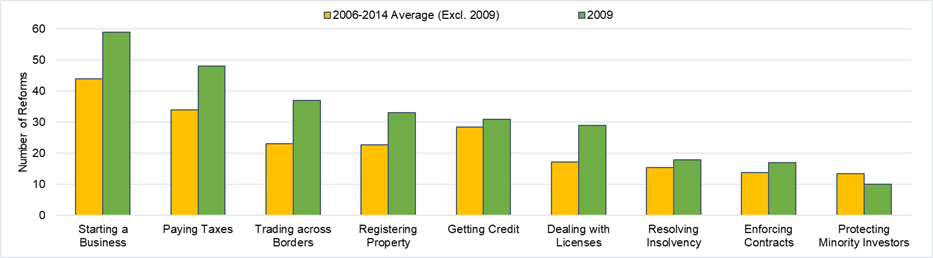

Figure 6. Reforms were implemented across a wide range of business areas during the 2009 recession

Source: World Bank Group Doing Business database.

Note: Data refers to reforms in 176 economies and 9 business environment areas measured under the same methodology in Doing Business 2007-2015 reports.

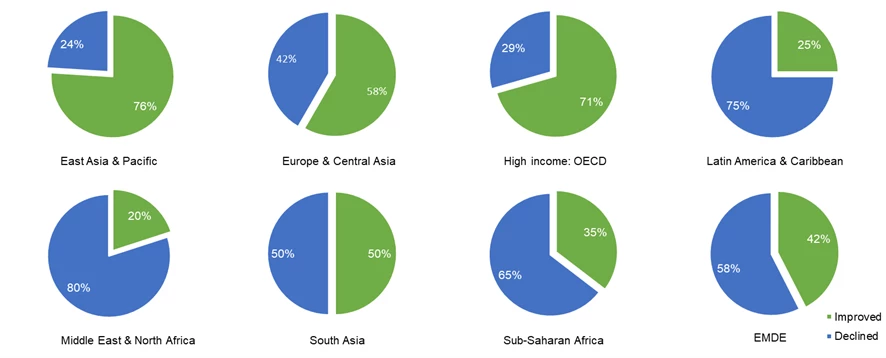

For the private sector to come to the rescue as the world confronts the impacts of the pandemic, a robust set of reforms geared towards improving the business environment is needed in both developing and advanced countries. In this regard, the trends before the pandemic were not particularly promising. Take, for example, business regulatory quality—all developing country regions, except for East Asia and the Pacific and Europe and Central Asia, had more countries worsening than improving in regulatory quality with respect to the global trend (see Figure 7).

Figure 7. The percentage of economies, by region, that improved or worsened their WGI Regulatory Quality score between 2011 and 2019—not a promising trend in most developing countries

Source: World Bank Group World Governance Indicators (WGI).

Note: Data refers to 191 economies in the WGI (Regulatory Quality) Database.

WHAT TO REFORM?

The list of needed reforms is long in almost every country and, in some countries, overwhelmingly so. Yet, the sheer number of required reforms is not necessarily a major obstacle. The lack of insightful international benchmarks for policy reforms, however, is. This is where the World Bank can make a difference. Among the many valuable initiatives that conduct private sector diagnostics, I would like to underscore the new and improved World Bank Group projects that target the business environment.

The forthcoming Business Ready project (both global and sub-national), the expanding Enterprise Surveys program, and the improving Women, Business, and the Law report all attempt to provide not only the orientation of reform but also details of what should be reformed for the private sector to recover in times of crises and grow sustainably at all times.

Join the Conversation