Health Financing

Health Financing

In the months ahead, the world is likely to experience the most rapid economic growth in the aftermath of any recession in the last 80 years. This swift economic turnaround, however, doesn’t hide the fact that a sustained, inclusive global recovery from COVID-19, poses complex challenges that have yet to be resolved.

The return to growth is crucial for the recovery, but so is countries’ ability to fund public investments. In the latest update of our paper, “From Double Shock to Double Recovery,” we look beyond economic growth to highlight large disparities in the capacities of countries to maintain and increase key public investments, including health over 2021 to 2026.

According to the IMF’s latest macro-fiscal projections, 126 countries will increase their per capita general government expenditure (GGE) above pre-COVID levels in the next five years. Yet in 52 countries, per capita GGE is projected to remain below the levels of 2019 before the pandemic hit. We call the first group “GGE-growth countries” and the second “non-GGE-growth countries.”

This distinction has salience for policy choices, as our paper shows. Further forms of diversity within each of the groups is also an important factor. For example, both groups include rich and poor countries. In addition, in both groups, countries show differences in the outlook across a wider range of fiscal parameters. For example, among both GGE-growth and non-GGE-growth countries prospects vary substantially for the length and depth of periods in which governments are expected to cut their spending. Growing debt service requirements will also differentially constrain countries’ ability to invest in the welfare of people.

Many countries are expected to decrease their government health spending

Unaddressed, these disparities in the fiscal outlook will widen rifts in the ability of countries to finance their recovery from the COVID-19 health shock. At one extreme, there are some higher-income countries in the GGE-growth group—whose already-strong health financing capacities are poised to grow further in the years ahead. At the other end are some lower-income countries in the non-GGE-growth group, whose health spending is historically weak and is likely to further diminish.

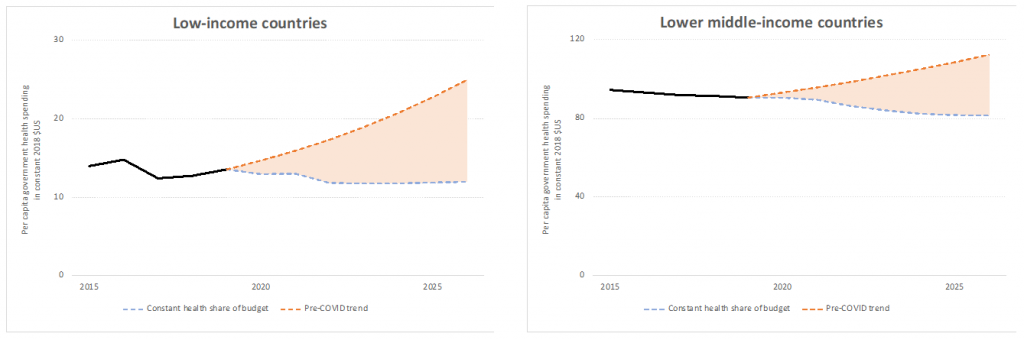

Unless governments raise the priority assigned to health in their budgets, low-income countries (LICs) in the non-GGE-growth group, will see their average per capita government spending on health drop almost 12% between 2019 and 2026 to an average of $12 (Figure 1). This brings their average health spending to levels less than half what would have been expected for 2026 under trends prior to COVID-19 (Figure 1). For the lower-middle-income countries (LMICs) among the 52 non-GGE-growth countries, per capita general government spending on health will fall by nearly 10% between 2019 and 2026 to an average of $82, instead of growing to $114, as would have been expected under pre-COVID trends.

So why don’t these countries direct more resources to health? In the wake of COVID-19, few can doubt the importance of such investments. But many of these countries simply can’t afford to spend adequately on health.

For most countries at the lower end of the health-financing spectrum, a return to past growth trends in per capita government spending on health is an almost impossible task. On average, to keep their health spending growing at pre-pandemic rates, non-GGE-growth LICs, for example, would have to double the share of their government expenditure dedicated to health, from 10% pre-COVID to 20% in 2026; and non-GGE-growth LMICs from 8.1% pre-COVID to 13.5% in 2026.

Shortfalls in financing of COVID-19 vaccines, preparedness and response capabilities

Exceptional health financing commitments are needed in LICs and LMICs to return to pre-pandemic growth trends in per capita government spending on health; yet even these levels would still be insufficient to finance investments necessary to halt the current pandemic and prevent future ones.

An analysis of spending needs and available resources for COVID-19 vaccines makes this clear. In LICs, the projected net growth in health spending during 2021 and 2022 will amount on average to only 45% of the countries’ cost share of a COVID-19 vaccine roll out (including the logistical costs of vaccine distribution but excluding support from COVAX). If LICs do not return to pre-pandemic growth rates in government health spending, this share will be on average only 28 percent with non-GGE-growth countries among them lacking any incremental resources to invest in the COVID-19 vaccine roll-out.

Similarly, the expected net growth in government health spending in LMICs over the same period will cover only 66% of these countries’ cost share for the vaccine rollout. If countries do not return to pre-pandemic growth rates in government health spending, this share will be on average only 43 percent.

With the expected delays or inability to mobilize sufficient funds for a timely and effective rollout of vaccines, countries will be unable to halt the transmission of the coronavirus and the emergence of new variants.

Likewise, countries’ capacity to invest in strengthening preparedness and response for future pandemics will continue to fall short. The projected net growth in government health spending in LICs and LMICs by 2026 will cover only about three-quarters of the necessary annual investment to strengthen and maintain public health preparedness and response capabilities. If LICs and LMICs do not return to pre-pandemic growth rates in health spending, this share will be on average just above 60 percent.

Universal health coverage—a tough job just got tougher

Emerging rifts in health financing capacities are expected to have even more far-reaching destructive effects. This is because they may force cash-strapped countries into difficult either/or choices in health investment. Funding response and preparedness priorities at the cost of other essential health services would pose grave risks for a full, sustained health and economic recovery from COVID-19. The initial COVID-19 health shock weakened non-pandemic health services in many settings, as health-system resources were redirected to the pandemic response. The Global Financing Facility (GFF), which supports the continuity of essential health services as part of COVID-19 response efforts, has been sounding the alarm of this secondary health crisis for vulnerable populations. Regaining losses in progress toward universal health coverage (UHC) is critical for human capital development and a full return to inclusive growth.

The original “Double Shock, Double Recovery” paper laid out the choices that countries have in managing their government funds to meet spending needs for health and economic recovery. The latest data indicate, however, that in many lower-income countries, choices are increasingly constrained, and the financing of a full health recovery from their own resources - increasingly out of reach.

Acting on common interests

Rifts in countries’ capacity to finance health were large before the pandemic—and they are widening further in its wake, creating a fault line that threatens COVID-19 recovery and health security for all. The good news is that, in contrast to geologic rifts, human action can bridge the health financing divide and prevent much of the damage it may bring. Coordinated global action that reverses the recent stagnation in development assistance for health will have positive effects far beyond the lower-income countries that benefit from it first.

It won’t be easy to boost development assistance for health at a time when some wealthy donor countries are also struggling. But high-income countries, too, have a vital interest in reinforcing a global recovery that remains fragile. The World Bank Group, with the IMF, WHO, and WTO have formed a task force to accelerate access to COVID-19 vaccines, therapeutics, and diagnostics by leveraging trade solutions and multilateral finance. Only together, countries can bridge the health financing rifts to build a healthier, more secure, more prosperous future for all.

Join the Conversation